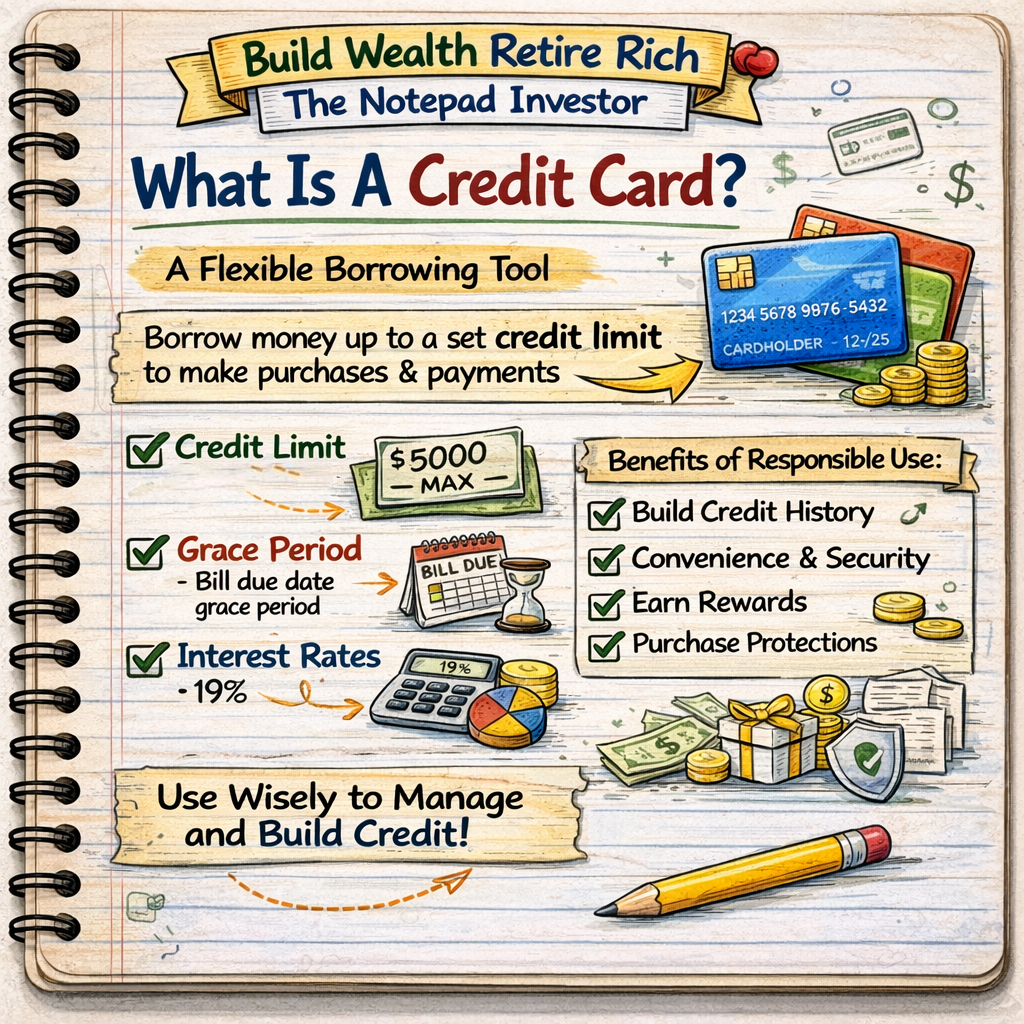

Credit cards are revolving credit instruments issued by financial institutions allowing cardholders to borrow money up to predetermined credit limits for purchases, cash advances, or balance transfers with obligation to repay borrowed amounts plus interest on unpaid balances—functioning as short-term loans renewable monthly through minimum payments enabling ongoing credit access unlike installment loans requiring full repayment before reborrowing. Operating through networks (Visa, Mastercard, American Express, Discover) processing transactions between merchants, cardholders, and issuing banks, credit cards provide payment convenience, fraud protection superior to debit cards or cash, rewards programs offering cash back or travel points, and financial flexibility for emergencies or large purchases when used responsibly through full monthly balance payments avoiding interest charges—but create debt traps through high interest rates (15-25% APR typical) when balances carried monthly compounding into thousands in interest costs over years making credit cards simultaneously powerful financial tools enabling rewards optimization and purchase protection when managed strategically versus destructive debt instruments destroying wealth through interest accumulation when misused carrying balances indefinitely.

This article is designed for anyone wanting comprehensive credit card understanding, individuals deciding whether to use credit cards or stick to debit/cash, or those seeking to optimize existing card usage avoiding common pitfalls. You do not need financial expertise to understand credit cards—fundamental concepts accessible through clear explanations of card mechanics, costs, benefits, and strategic usage, though requires discipline distinguishing between spending capacity (credit limit) and actual affordability preventing debt accumulation through charging purchases beyond ability to pay in full monthly creating interest-bearing balances growing through compounding impossible to eliminate without aggressive payoff commitment or strategic behavior changes addressing root spending versus income mismatches.

Understanding credit cards matters because appropriate card use builds credit history enabling major purchases (homes, vehicles) impossible without established creditworthiness, strategic usage captures rewards worth hundreds to thousands annually through cash back or travel points, and superior fraud protection prevents unauthorized charge liability versus debit card vulnerabilities affecting actual bank funds—while informed card users maintain zero-interest costs through full monthly payments while earning 2-5% rewards on spending, build excellent credit scores through on-time payments and low utilization, and leverage purchase protections (extended warranties, return protection, dispute rights) creating value impossible to replicate through cash or debit, strategic card management produces superior financial outcomes versus either card avoidance forfeiting benefits or irresponsible usage creating high-interest debt negating rewards through interest costs exceeding cash back earnings.

Educational disclaimer: This article provides general educational information about credit cards. Individual card terms, rates, fees, and features vary significantly by issuer and cardholder qualifications. Credit cards carry debt accumulation risks and potential credit score damage from mismanagement. This is not financial advice or recommendation of specific card usage strategies. Consult qualified financial professionals for personalized guidance. Card benefits, rewards, and terms subject to change. Responsible usage requires discipline paying balances in full monthly avoiding interest charges.

How Credit Cards Work

Basic Credit Card Mechanics

The credit card cycle:

- 1. Credit granted: Issuer approves account with credit limit (example: $5,000)

- 2. Purchases made: Cardholder charges purchases throughout month

- 3. Statement generated: Monthly statement shows charges, balance, minimum payment, due date

- 4. Grace period: 21-25 days from statement closing to payment due date (if paying in full)

- 5. Payment made: Cardholder pays minimum, full balance, or amount in between

- 6. Cycle repeats: Available credit replenishes as payments made

Key terminology:

- Credit limit: Maximum amount borrowable on card

- Available credit: Credit limit minus current balance

- Statement balance: Total charges during billing cycle

- Current balance: Real-time balance including charges after statement closing

- Minimum payment: Smallest payment accepted (typically 1-3% of balance or $25-35 minimum)

- Grace period: Interest-free period between statement closing and payment due date

Payment Options and Consequences

Option 1: Pay full statement balance (optimal)

- Pay entire statement balance by due date

- Zero interest charged

- Grace period maintained for next cycle

- Available credit fully replenished

- Builds credit through payment history without interest costs

Example: Statement balance $2,000, pay $2,000 by due date = $0 interest, grace period continues

Option 2: Pay minimum payment (expensive)

- Pay only minimum required (example: $50 on $2,000 balance)

- Interest charged on remaining balance ($1,950)

- Grace period lost—interest accrues immediately on new purchases

- Balance persists indefinitely with minimum-only payments

- Total cost dramatically higher through compounding interest

Example: $2,000 balance at 18% APR, minimum payments only = 5+ years to pay off, $1,500+ interest paid, total cost $3,500+

Option 3: Pay partial amount

- Pay more than minimum but less than full balance

- Interest charged on remaining balance

- Reduces balance faster than minimum-only

- Still incurs interest costs until fully paid

Example: $2,000 balance, pay $500 monthly = 4-5 months payoff, $150-200 interest depending on APR

Interest Calculation

How credit card interest works:

- APR (Annual Percentage Rate) divided by 365 = daily rate

- Daily rate multiplied by average daily balance = daily interest

- Daily interest compounded (added to balance daily)

- Monthly interest = sum of daily interest for billing cycle

Example calculation:

- Balance: $3,000

- APR: 18%

- Daily rate: 18% ÷ 365 = 0.0493% per day

- Daily interest: $3,000 × 0.000493 = $1.48 per day

- Monthly interest (30 days): $1.48 × 30 = $44.40

Compounding effect:

- Interest added to balance daily

- Next day’s interest calculated on balance + previous interest

- Creates exponential growth if balance not paid down

Types of Credit Cards

Rewards Credit Cards

Cash back cards:

- Earn percentage back on purchases (1-5% typical)

- Flat-rate cards: Same percentage all purchases (1.5-2% common)

- Category bonus cards: Higher rates specific categories (3-5% groceries, gas, dining)

- Rotating category cards: 5% on quarterly rotating categories

- Redemption: Statement credit, direct deposit, or gift cards

Travel rewards cards:

- Earn points or miles for travel redemptions

- Airline-specific cards: Miles with specific carrier

- Hotel-specific cards: Points with hotel chain

- General travel cards: Flexible points for any travel

- Perks: Airport lounge access, travel insurance, no foreign transaction fees

Premium rewards cards:

- High annual fees ($250-$695)

- Enhanced rewards (2-3% or higher)

- Premium benefits: Lounge access, travel credits, concierge service

- Requires high spending to justify annual fee

Balance Transfer Cards

Features:

- 0% APR promotional period (12-21 months typical)

- Transfer balances from high-interest cards

- Balance transfer fee (3-5% of transferred amount typically)

- Debt payoff tool when used strategically

Strategic usage:

- Transfer $5,000 from 18% card to 0% card (18 months)

- Pay $278/month = fully paid before 0% expires

- Saves $700+ in interest versus keeping on original card

- Requires discipline avoiding new charges during payoff

Secured Credit Cards

For building or rebuilding credit:

- Requires security deposit ($200-$500 typical)

- Deposit amount becomes credit limit

- Reports to credit bureaus like regular cards

- Graduation to unsecured card after 6-12 months responsible use

- Deposit returned upon graduation or account closure

Common secured cards:

- Discover it Secured: Cash back rewards, no annual fee

- Capital One Platinum Secured: Low deposit options

- Secured Mastercard from Capital One: Flexible deposits

Student Credit Cards

Designed for college students:

- Easier approval with limited credit history

- Lower credit limits ($500-$1,500 typical)

- Basic rewards programs

- No annual fees usually

- Requires student status verification

Business Credit Cards

For business expenses:

- Separate business and personal spending

- Business expense tracking and reporting

- Higher credit limits

- Business rewards categories (office supplies, advertising)

- Employee card options

Credit Card Costs and Fees

Interest Rates (APR)

Typical APR ranges:

- Excellent credit (750+): 13-18% APR

- Good credit (670-749): 17-22% APR

- Fair credit (580-669): 21-25% APR

- Poor credit (below 580): 25-29.99% APR or denied

Variable vs fixed APR:

- Variable APR: Changes with prime rate (most cards), can increase/decrease over time

- Fixed APR: Rare on modern cards, can still change with 45-day notice

Multiple APRs on single card:

- Purchase APR: Standard rate for purchases

- Cash advance APR: Higher rate (typically 25-30%), no grace period

- Balance transfer APR: Often promotional 0% then higher rate

- Penalty APR: Applied after late payments (up to 29.99%)

Annual Fees

Fee structures:

- No annual fee cards: $0 (most basic cards, many cash back cards)

- Low annual fee: $25-$95 (some rewards cards)

- Premium cards: $95-$250 (enhanced rewards, benefits)

- Luxury cards: $450-$695 (premium travel cards, exclusive benefits)

Fee justification calculation:

- Card annual fee: $95

- Annual rewards earned: $300 (3% on $10,000 spending)

- Net benefit: $300 – $95 = $205 positive

- Justified if rewards and benefits exceed fee

Other Common Fees

Transaction fees:

- Late payment fee: $25-$40 (first offense $25, subsequent $40)

- Over-limit fee: $25-$35 (rare now, must opt in)

- Foreign transaction fee: 1-3% of purchase amount (many cards waive)

- Balance transfer fee: 3-5% of transferred amount

- Cash advance fee: 3-5% of advance amount (minimum $10 typically)

- Returned payment fee: $25-$40

Credit Card Benefits

Fraud Protection

Superior liability protection:

- Credit card liability: $50 maximum by law (most issuers waive entirely)

- Zero liability policies: Most major issuers offer $0 liability for unauthorized charges

- Dispute process: Temporary credit while investigating, 60-90 days to dispute

- Your money safe: Fraudulent charges affect credit line not bank account

Debit card comparison:

- Report within 2 days: $50 maximum liability

- Report within 60 days: $500 maximum liability

- Report after 60 days: Unlimited liability (total loss possible)

- Your money withdrawn: Bank account affected, bills may bounce

- Investigation time: 2-4 weeks without funds access

Example fraud scenario:

- $3,000 fraudulent charges

- Credit card: Report fraud, temporary credit issued, continue using card, resolved in 7-10 days, $0 liability

- Debit card: $3,000 withdrawn from checking, overdrafts possible, 2-4 weeks investigation, potential liability up to $500

Purchase Protections

Extended warranty protection:

- Adds 1-2 years to manufacturer warranty

- Automatic coverage on most cards

- Covers repairs or replacement if item fails

- Example: $800 laptop with 1-year warranty, card extends to 2-3 years free

Purchase protection (damage/theft):

- Covers damaged or stolen items 90-120 days from purchase

- Typical coverage: $500-$10,000 per claim

- Example: Buy $600 camera, stolen within 90 days, card reimburses

Return protection:

- Refund if merchant won’t accept return

- Typically 90 days from purchase

- Coverage limits apply

Price protection:

- Refund price difference if item goes on sale within 60-90 days

- Example: Buy TV for $800, drops to $650 in 60 days, card refunds $150 difference

- Note: Many issuers phasing out this benefit

Rewards and Cash Back

Value calculation:

- $30,000 annual spending on 2% cash back card = $600 annually

- Over 30 years: $18,000 total rewards

- Requires: Paying balance in full monthly (zero interest)

- Cash/debit alternative: $0 rewards on same spending

Category optimization:

- Grocery card: 3% on groceries ($6,000 annual = $180)

- Gas card: 3% on gas ($3,000 annual = $90)

- Dining card: 4% on restaurants ($4,000 annual = $160)

- General card: 1.5% everything else ($17,000 annual = $255)

- Total rewards: $685 annually from strategic category matching

Travel Benefits

Premium card perks:

- Airport lounge access (Priority Pass, airline lounges)

- Travel insurance (trip cancellation, delay, lost luggage)

- Rental car insurance (primary or secondary coverage)

- No foreign transaction fees

- Travel credits ($200-$300 annually)

- Global Entry/TSA PreCheck credit ($100 every 4-5 years)

Building Credit

Credit score benefits:

- Establishes credit history (15% of FICO score)

- Creates payment history (35% of score) when paid on time

- Adds to credit mix (10% of score)

- Provides credit utilization denominator (30% of score)

Timeline:

- 6 months: First credit score appears

- 12 months: Establish good score (680-720) with responsible use

- 24+ months: Achieve excellent score (740+) possible

Strategic Credit Card Usage

Golden Rules of Credit Cards

Rule 1: Pay full balance monthly

- Zero interest charges

- Maintain grace period

- Maximize rewards without costs

- Build credit without paying for privilege

Rule 2: Keep utilization under 30%, ideally under 10%

- Credit utilization = current balance ÷ credit limit

- Affects 30% of credit score

- Example: $5,000 limit, keep balance under $500 (10%)

- Pay before statement closing date for lower reported utilization

Rule 3: Pay on time every month

- Payment history is 35% of credit score

- Single 30-day late payment drops score 60-110 points

- Set up automatic minimum payment as backup

- Calendar reminders 5 days before due date

Rule 4: Only charge what you can afford to pay in full

- Credit limit is not spending target

- Use credit as payment method not loan vehicle

- If can’t pay cash, probably shouldn’t charge

- Exceptions: Planned large purchases with payoff strategy

Optimizing Rewards

Multi-card strategy:

- Match spending categories to highest-earning cards

- 2-4 cards optimal for most people (more creates complexity)

- Track which card for which spending

Example optimized wallet:

- Card 1: 3% groceries and gas

- Card 2: 4% dining and entertainment

- Card 3: 2% everything else

- Total spending $30,000: Earns $750 annually optimized vs $450 on single 1.5% card

What NOT to Do

Avoid cash advances:

- High fees (3-5% plus $10 minimum)

- High APR (25-30% typical)

- No grace period (interest starts immediately)

- Example: $500 cash advance = $25 fee + $12.50 interest first month = $537.50 total

Avoid minimum-only payments:

- Compounds debt indefinitely

- Pays mostly interest not principal

- Example: $5,000 balance, 18% APR, minimum payments = 15+ years, $6,000+ interest

Avoid unnecessary cards:

- Store cards often have high APR (25-30%)

- Limited usefulness (single retailer only)

- Hard inquiry on credit report

- Exception: Significant one-time discount with payoff plan

Avoid closing old cards:

- Reduces total credit limits (increases utilization)

- Eventually lowers average account age

- Damages credit score 20-40 points typically

- Keep old cards open even if unused (small annual charge prevents closure)

Credit Cards vs Debit Cards vs Cash

Comparison Overview

Credit cards:

- Pros: Rewards, fraud protection, builds credit, grace period, purchase protections

- Cons: Debt risk, interest if balances carried, requires discipline

- Best for: Disciplined users paying in full monthly

Debit cards:

- Pros: Spends own money (no debt), widely accepted, convenient

- Cons: No rewards, weaker fraud protection, no credit building, no purchase protections

- Best for: Those lacking card discipline or building spending awareness

Cash:

- Pros: No debt possible, tangible spending awareness, universally accepted

- Cons: No rewards, no fraud protection, no credit building, inconvenient, theft risk

- Best for: Small transactions, budget envelope system

30-Year Value Comparison

Scenario: $30,000 annual spending, 30 years

Credit card (paid in full monthly):

- Rewards: $600 annually × 30 years = $18,000

- Interest paid: $0

- Credit score: Excellent (enables low mortgage rates saving $50,000+)

- Fraud protection: Superior

- Net benefit: $68,000+ (rewards + mortgage savings)

Debit card:

- Rewards: $0

- Interest paid: $0

- Credit score: No credit history built (mortgage denied or higher rates)

- Fraud protection: Weaker

- Net benefit: $0, potential mortgage cost increase

Credit card (carrying balances):

- Rewards: $600 annually × 30 = $18,000

- Interest paid: $3,000 average balance × 18% APR × 30 years = $16,200

- Credit score: Damaged by high utilization

- Net benefit: $1,800 (rewards minus interest), credit damage

Key insight: Credit cards superior IF paid in full, destructive if balances carried

Why Understanding Credit Cards Matters

Without understanding credit cards, individuals either avoid cards entirely forfeiting rewards worth thousands and credit-building opportunities necessary for major purchases or misuse cards carrying balances paying hundreds to thousands annually in unnecessary interest negating rewards value—while card-literate users capture 2-5% rewards on all spending through strategic card matching, build excellent credit scores through on-time payments and low utilization enabling lowest mortgage rates, and leverage superior fraud protection and purchase benefits creating value impossible through cash or debit, making credit card knowledge essential for optimizing modern payment infrastructure when combined with discipline ensuring balances paid in full monthly avoiding interest costs that destroy wealth through compounding over years.

Understanding credit cards enables individuals to:

- Earn hundreds to thousands annually in rewards through strategic card usage

- Build credit history necessary for mortgages and major purchases

- Protect against fraud through superior liability limits and dispute rights

- Avoid interest costs through understanding grace periods and payment timing

- Optimize credit scores through utilization management and payment discipline

- Leverage purchase protections (extended warranties, return protection) adding value

- Make informed decisions about card types, features, and costs versus benefits

Credit card knowledge transforms cards from feared debt instruments or ignored payment methods into strategically optimized financial tools producing measurable value through rewards, protections, and credit building when managed responsibly versus either avoidance forfeiting benefits or misuse creating destructive debt.

Common Misunderstandings

Many people assume carrying credit card balances helps credit scores by “showing activity.” In reality, credit scores improve through on-time payments and low utilization regardless of whether balances paid in full or carried—carrying balances costs substantial interest ($1,000 annually on $5,000 balance at 20% APR) with zero score benefit, proving pay-in-full strategy superior producing identical credit building without interest waste based on misunderstanding of score factors rewarding payment history and utilization percentage not interest payment to issuers.

Another common misconception is credit cards inherently dangerous requiring avoidance for financial safety. In practice, credit cards are neutral tools—strategic disciplined usage paying in full monthly produces superior outcomes through rewards, fraud protection, and credit building versus cash or debit alternatives, while irresponsible usage carrying balances creates destructive debt, proving cards themselves not problematic but rather user behavior determining outcomes making discipline and knowledge differentiating factors not card existence.

Some believe closing unused credit cards improves credit scores by reducing “available debt.” However, closing cards immediately increases credit utilization (lower total credit limits) and eventually reduces average account age both damaging scores 20-40 points typically, proving keeping old cards open even if unused superior strategy maintaining high total credit limits (lower utilization) and long account ages versus closing based on false belief that unused credit represents risk when algorithms reward high available credit relative to balances not absolute credit limit amounts.

How Credit Card Understanding Fits Into Financial Success

Credit card understanding enables optimization of modern payment infrastructure capturing thousands in lifetime rewards, builds credit history necessary for major purchases at optimal rates, and provides fraud and purchase protections impossible through cash or debit—making card literacy essential component of comprehensive financial success when combined with discipline ensuring responsible usage through full monthly payments, strategic reward optimization through category matching, and credit score management through low utilization and perfect payment timing, transforming cards from potential debt traps into value-generating tools producing measurable benefits impossible without understanding card mechanics, costs, benefits, and strategic usage principles.

For example, two friends age 25 both earning $50,000 with identical $30,000 annual spending. Friend A avoids credit cards believing “debt is dangerous” using debit card exclusively. Never builds credit history, denied mortgage age 30 despite $40,000 saved (no credit = no mortgage approval), forced to continue renting $1,800 monthly. Zero rewards earned on $30,000 annual spending over 30 years = $0. Age 55: Paid $648,000 in rent over 30 years, $200,000 saved (disciplined saver) but no home equity, never qualified for mortgage due to absent credit history. Friend B understands credit cards as tools requiring discipline, opens 2% cash back card age 25 paying full balance monthly never carrying interest-bearing balance. Uses card for all spending: $30,000 annually × 2% = $600 rewards yearly. Age 30: Excellent 760+ credit score from 5 years perfect payment history, low utilization. Approved for mortgage with $40,000 down (identical savings as Friend A). Buys $300,000 home, 6% rate enabled by excellent credit, $1,799 monthly payment. Over 30 years: $18,000 rewards earned ($600 × 30 years), built $150,000 home equity through ownership versus rent, excellent credit enabled optimal mortgage rate saving $50,000 versus fair credit rates. Age 55: Home worth $600,000 with $300,000 equity, total rewards $18,000, optimal rates on all borrowing saving $75,000+ lifetime. Difference from identical starting points and identical spending: Friend A’s card avoidance cost $400,000+ ($648,000 rent vs $216,000 mortgage principal paid building equity minus $18,000 rewards minus $75,000 borrowing cost savings = $441,000 disadvantage) despite equal spending discipline and savings rates—entire difference from credit card understanding enabling credit building, rewards capture, and strategic usage versus avoidance based on misconception that cards inherently dangerous versus recognizing discipline as differentiating factor.

Credit card understanding separates strategic optimizers capturing rewards and building credit enabling wealth accumulation from either avoiders forfeiting benefits creating opportunity costs or misusers carrying balances paying thousands in interest negating rewards through lack of discipline or knowledge.

Recent Updates and Trends

In recent years, credit card rewards competition has intensified with cards offering 2-5% cash back or valuable travel points becoming standard versus historical 1% rewards creating enhanced value proposition for strategic users though tempting overspending through rewards psychology potentially negating benefits when balances carried paying interest exceeding cash back earnings.

Contactless payment technology has expanded through tap-to-pay cards and mobile wallets (Apple Pay, Google Pay) improving transaction speed and security versus magnetic stripe cards though creating potential for easier impulse spending through reduced payment friction making discipline more critical as payment convenience increases.

Buy-now-pay-later services have proliferated offering point-of-sale financing as credit card alternative splitting purchases into installment payments, appealing to younger consumers wary of traditional credit cards but creating similar debt risks plus credit building limitations versus strategic credit card use building credit scores through reporting to bureaus.

Annual fee cards have increased in prevalence with premium cards offering enhanced benefits justifying $250-$695 fees for high spenders capturing value through multiplied rewards and perks, though requiring careful cost-benefit analysis ensuring rewards and benefits exceed fees versus assuming premium cards always superior when benefits may not justify costs for moderate spending levels.

Fundamental credit card principles remain timeless: paying balances in full monthly avoids interest while capturing rewards, low utilization and perfect payments build excellent credit scores, superior fraud protection provides security advantage, and strategic usage produces measurable benefits impossible through cash or debit—regardless of rewards intensification, payment technology evolution, alternative financing proliferation, or premium card expansion, understanding card mechanics, maintaining discipline paying in full, and optimizing rewards strategically produces superior financial outcomes through responsible leverage of payment infrastructure benefits versus either avoidance forfeiting advantages or misuse creating destructive debt through lack of knowledge or discipline.

3 Things You Can Do Today

Ready to optimize credit card usage? Here are three simple steps you can take right now:

1. Calculate your current annual rewards and potential rewards with optimized card strategy – Review last 12 months spending by category: Groceries (example: $6,000), gas ($3,000), dining ($4,000), travel ($2,000), everything else ($15,000), total $30,000 annually. Calculate current rewards: If using 1.5% cash back card on everything = $30,000 × 0.015 = $450 annually. Research category-specific cards: Groceries card 3% ($6,000 × 0.03 = $180), gas card 3% ($3,000 × 0.03 = $90), dining card 4% ($4,000 × 0.04 = $160), travel card 2% ($2,000 × 0.02 = $40), everything else 1.5% ($15,000 × 0.015 = $225). Optimized total: $695 annually versus $450 current = $245 additional annually, $7,350 over 30 years from strategic card matching. Check annual fees: Ensure rewards exceed fees (example: $695 rewards minus $95 combined fees = $600 net benefit). Create simple reference: “Groceries → Card A, Dining → Card B, Everything else → Card C” preventing decision fatigue. Critical requirement: Only effective if paying balances in full monthly—carrying balances at 18% APR negates rewards ($5,000 average balance = $900 interest annually exceeding $695 rewards). Takes 30 minutes calculating opportunity creating $245 annual value increase through strategic card optimization.

2. Set up automatic full payment from checking account ensuring zero interest costs while capturing rewards – Log into credit card account online, navigate to automatic payment settings. Configure automatic FULL STATEMENT BALANCE payment from checking account (not minimum payment). Verify sufficient checking buffer: Maintain $500-1,000 extra in checking preventing overdrafts when automatic payment processes. Set payment date: 2-3 days before due date ensuring processing time. Enable low balance alerts: Both checking (warns if buffer insufficient) and credit card (confirms payment processed). This guarantees: Zero interest charges ever (grace period maintained), zero late payment fees, perfect payment history (35% of credit score), maximum rewards capture without costs. Monitor first 2-3 months: Ensure payments processing correctly, checking balance sufficient, no issues. Backup reminder: Calendar alert 5 days before payment date verifying checking balance adequate. Takes 15 minutes one-time setup creating permanent zero-interest operation capturing full rewards value impossible when carrying balances or making manual payments risking late fees and interest from forgotten payments. Critical: Budget ensuring spending not exceeding income creating situation where automatic payment cannot be covered—credit cards are payment method not income supplement requiring spending discipline.

3. If currently carrying credit card debt, create aggressive payoff plan calculating total interest cost of minimum payments versus payoff timeline – List all credit card balances: Card A $3,000 at 18% APR, Card B $2,000 at 22% APR, total $5,000 debt. Calculate minimum payment costs: Use online credit card payoff calculator entering balances and APRs. Minimum payments only: $5,000 debt takes 15-20 years, total interest $6,000-8,000, total paid $11,000-13,000. Create aggressive plan: How much can you pay monthly? Example: $500 monthly total. Debt avalanche method (optimal): Pay minimums on all cards, apply extra to highest APR card first (Card B 22%), once eliminated attack next highest. Timeline: $500 monthly pays off $5,000 in 11-12 months, total interest ~$500 versus $6,000+ minimum-only. Debt snowball alternative (psychological): Pay smallest balance first regardless of APR creating quick wins, slightly more interest but better motivation for some people. During payoff: Stop all new charges (use debit card temporarily), redirect any extra income to debt (tax refunds, bonuses), track progress monthly. After payoff: Maintain $500 monthly “payment” redirecting to savings preventing lifestyle inflation and building emergency fund. Takes 20 minutes creating concrete payoff plan with specific timeline and total cost versus indefinite minimum payments, typically saving $5,000+ in interest and achieving freedom in 12 months versus 15+ years making aggressive planning essential for anyone carrying balances.

These actions create credit card optimization within 90 minutes—calculated rewards opportunity through strategic card matching ($245+ annually), implemented automatic full payments ensuring zero interest forever, and created aggressive debt payoff plan if carrying balances (saving $5,000+ interest)—transforming credit cards from potential debt traps or underutilized payment methods into optimized value-generating tools through strategic usage, payment discipline, and debt elimination when applicable.

Quick FAQ

Does carrying a credit card balance help my credit score?

No—complete myth wasting money. Credit scores improve through: (1) On-time payments (happens whether balance paid in full or carried monthly), (2) Low credit utilization under 30% ideally under 10% (actually better at lower percentages not higher), (3) Length of credit history, (4) Credit mix. Carrying balance costs interest with ZERO additional score benefit versus paying in full. Example: $2,000 average balance at 18% APR = $360 annual interest wasted for no credit advantage. Correct approach: Use cards actively generating payment history, pay FULL balance monthly avoiding all interest, maintain low utilization (easily achieved paying in full), keep accounts open long-term building history length. This maximizes credit score while minimizing costs versus “carry small balance” myth enriching card issuers through unnecessary interest payments providing zero scoring benefit based on misunderstanding of FICO calculation factors.

Should I close credit cards I’m not using?

Usually no—closing typically damages credit scores. Negative impacts: (1) Reduces total credit limits increasing utilization percentage (example: $10,000 limits with $2,000 balance = 20% utilization, close $5,000 limit card = now 40% utilization on remaining $5,000 limits damaging scores), (2) Eventually reduces average account age when closed account falls off report after 10 years (FICO) or immediately (VantageScore), (3) Reduces number of accounts and credit mix slightly. Score impact: 20-40 points typical from closing old established card. Exceptions where closing acceptable: High annual fee card ($450+) not providing value justifying cost, multiple similar cards creating management complexity when have several no-fee alternatives, identity theft cleanup. Better strategy: Keep old no-fee cards open, make small purchase annually ($5-10) preventing issuer closure from inactivity, set up automatic payment and forget about card. Costs zero, maintains credit limits lowering utilization, preserves account age, protects credit score.

How many credit cards should I have?

Depends on spending patterns and management ability but 2-4 cards optimal for most people balancing rewards optimization and simplicity. One card: Simplest management but limited rewards optimization (single 1.5-2% rate on everything). Two cards: Good balance, example: One 2% everything card plus one category bonus card (3-5% groceries/gas). Three cards: Better optimization, example: Groceries card, dining card, everything else card capturing category bonuses. Four+ cards: Maximum optimization for high spenders willing to track categories, can become complex managing multiple payments and tracking. Credit score perspective: Multiple cards beneficial showing credit management capability, total credit limits higher (lower utilization), mix of account ages. Warning: Only if disciplined paying all in full monthly—more cards = more complexity = higher risk of missed payment if not systematic. Start conservative: Begin with 1-2 cards, add strategically after proving payment discipline, prioritize management simplicity over marginal rewards unless high spender justifying complexity through substantial additional rewards.

What’s the difference between statement balance and current balance?

Critical distinction affecting interest charges: Statement balance = total charges during billing cycle from statement closing date, shown on monthly statement, amount due to avoid interest. Current balance = real-time balance including charges made AFTER statement closing date, reflects all pending transactions. Payment strategy: Pay STATEMENT BALANCE in full by due date to avoid interest and maintain grace period (current balance may be higher due to post-statement charges but those appear on next statement). Example timeline: Statement closes January 15 showing $1,000 balance (due February 10), you charge $500 more January 16-February 9, current balance shows $1,500 but only $1,000 statement balance due. Pay $1,000 by February 10: Zero interest charged, grace period maintained, $500 appears on February statement due March 10. Mistake: Confusing current balance for statement balance paying wrong amount (paying only current balance when higher charges made after statement closing overpays current cycle, paying only current balance when lower than statement underpays owing interest). Always reference STATEMENT BALANCE from monthly statement for payment amount needed to avoid interest not current balance from online account which fluctuates daily.

Is it better to use credit cards or debit cards?

Credit cards superior IF disciplined paying in full monthly, debit cards safer if lacking spending discipline. Credit card advantages: 2-5% rewards (hundreds annually), superior fraud protection ($50 max liability vs $500 debit), builds credit history necessary for mortgages, grace period (21-25 days interest-free), purchase protections (extended warranties, return protection). Debit card advantages: Spends own money preventing debt accumulation, easier spending awareness (immediate balance reduction), no interest risk. The critical factor: DISCIPLINE paying full balance monthly. Disciplined user: Credit cards clearly superior—same spending, earn rewards, build credit, better protection, no interest if paid in full. Undisciplined user: Credit cards dangerous—easy overspending beyond means, interest accumulation, debt spiral, rewards negated by interest ($500 rewards meaningless when paying $2,000 interest). Recommendation: Use credit cards for all spending IF (1) budget maintained ensuring spending not exceeding income, (2) commitment to full monthly payment absolute, (3) automatic payments configured preventing late fees, (4) emergency fund exists covering unexpected expenses without card reliance. If struggling with spending control: Stick to debit temporarily while building discipline then transition to credit cards once demonstrated budget adherence preventing debt accumulation through overspending.

Explore More in Money Basics

Disclosure

This article provides general educational information about credit cards. Individual card terms, rates, fees, rewards, benefits, and features vary significantly by issuer, card type, and cardholder qualifications. Credit cards carry risks including debt accumulation and credit score damage from mismanagement. APR ranges, fee amounts, and reward rates represent typical market ranges as of publication—actual offers vary. This is not financial advice, product recommendation, or guarantee of approval or specific terms. Card benefits including purchase protections, extended warranties, and travel insurance have specific terms, limitations, and exclusions—review cardholder agreements for complete details. Rewards optimization calculations assume disciplined usage paying balances in full monthly—carrying balances negates rewards through interest costs. Some card benefits mentioned (price protection, return protection) being phased out by issuers—check current benefits before applying. Credit score impact examples represent typical scenarios—individual results vary based on complete credit profiles. Consult qualified financial professionals for personalized guidance. Focus on responsible usage maintaining zero interest-bearing balances rather than rewards optimization if lacking spending discipline. Card approval depends on creditworthiness, income, and issuer criteria. Annual fees, interest rates, and benefits subject to change by issuers. Comparison between credit cards, debit cards, and cash represents generalized scenarios—individual circumstances vary. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.