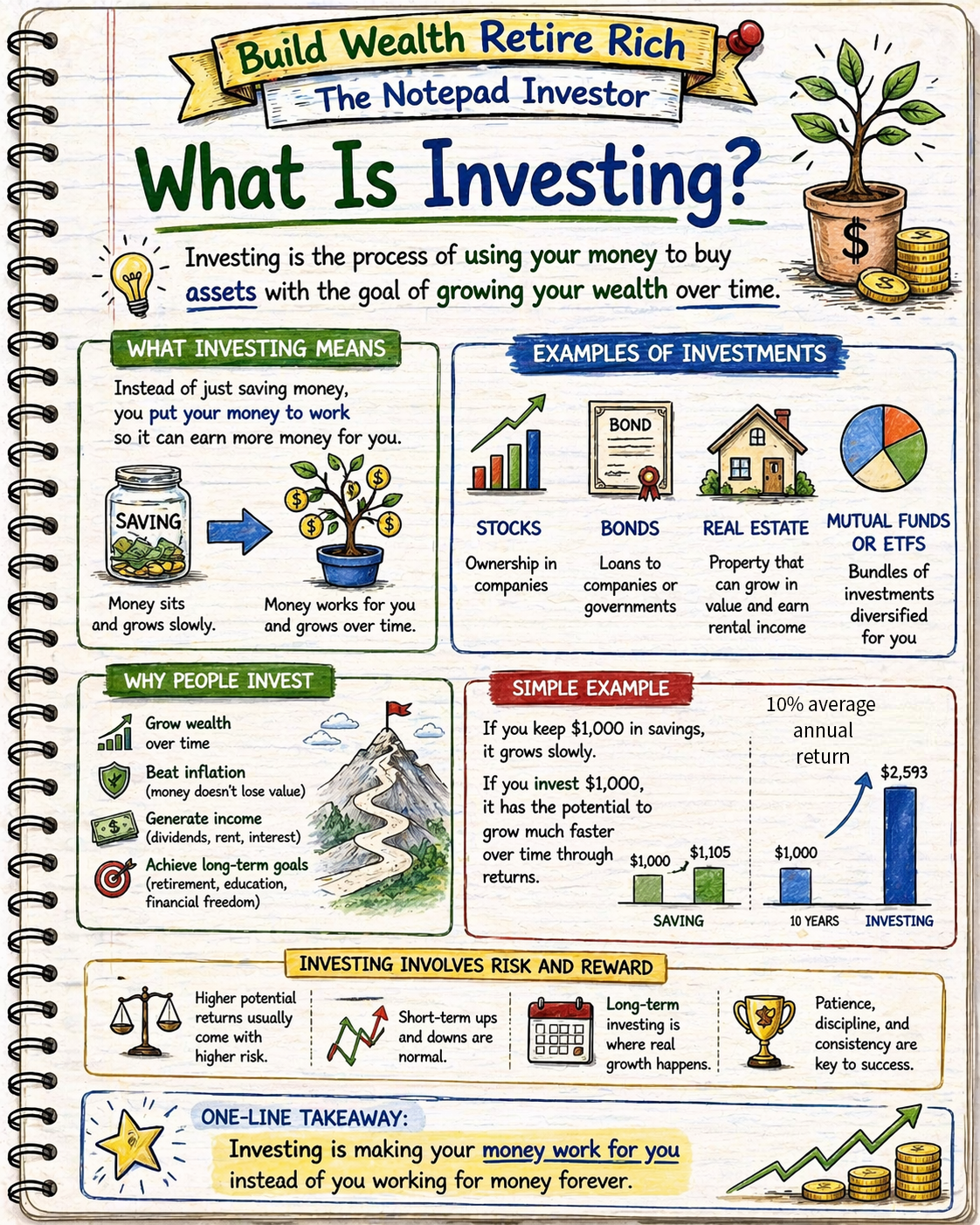

Investing is allocating money to assets expected to generate returns through appreciation, income, or both over time—purchasing stocks, bonds, real estate, mutual funds, or other securities with expectation that initial capital will grow through price increases, dividends, interest payments, or rental income creating wealth accumulation beyond what savings accounts provide. Unlike saving which preserves purchasing power through minimal interest in guaranteed accounts, investing deliberately accepts risk (potential for loss) in exchange for higher expected returns averaging 8-12% annually for stock market investments versus 0.5-5% for savings accounts, though with volatility creating year-to-year fluctuations including potential losses requiring long-term commitment (5-10+ years minimum) allowing recovery from temporary downturns. Representing essential wealth-building tool enabling retirement security, home purchases, education funding, and financial independence impossible through earned income and savings alone—$500 monthly invested at 8% grows to $745,179.72 over 30 years versus same amount saved at 1% yielding ~$210,000 demonstrating $535,179 compound return differential making investing critical for long-term prosperity despite requiring education, discipline, and risk tolerance unavailable through guaranteed savings vehicles prioritizing capital preservation over growth.

This article is designed for investing beginners wanting fundamental understanding, individuals intimidated by stock market complexity seeking accessible explanations, or those questioning whether investing necessary for financial security. You do not need financial expertise to understand investing—basic concepts accessible through clear explanations of returns, risks, asset types, and strategic principles, though requires honest risk assessment recognizing investment values fluctuate creating temporary losses requiring emotional discipline not panicking during downturns, long-term commitment maintaining investments through market cycles despite temptation selling during declines, and realistic expectations understanding 8-10% average annual returns come with volatility including negative years requiring patience impossible when expecting guaranteed steady gains or attempting market timing through frequent trading destroying compound returns through transaction costs and poor timing decisions.

Understanding what investing is matters because compound returns create wealth impossible through saving or earning alone enabling retirement security and financial goals, early investing start dramatically amplifies results through decades of compounding—$200 monthly at 8% from age 25 grows to $698,201.57 by 65 versus same amount starting age 35 yielding $298,071.89 demonstrating $400,129.68 advantage from 10-year head start, and strategic asset allocation balancing growth and safety determines outcomes separating comfortable retirements from financial struggle—while investment-literate individuals harness compound returns building $500,000-2,000,000 retirement wealth through disciplined long-term investing, versus non-investors relying solely on savings and Social Security facing retirement income inadequacy requiring lifestyle reduction or continued employment impossible to avoid without investment knowledge enabling informed participation in wealth-building markets creating measurable prosperity differences through strategic capital allocation impossible for cash-only savers regardless of income level when inflation erodes purchasing power faster than savings account interest accumulates.

Educational disclaimer: This article provides general educational information about investing concepts and principles. Individual investment decisions, appropriate strategies, and outcomes vary significantly based on circumstances including age, income, risk tolerance, goals, and time horizon. This is not financial advice, investment recommendation, or guarantee of returns. All investments carry risk including potential loss of principal. Past performance does not guarantee future results. Stock market returns average 8-10% historically but include negative years and significant volatility. Consult qualified financial advisors or investment professionals for personalized guidance matching individual situations and goals.

Investing Fundamentals

Investing Versus Saving

Saving characteristics:

- Purpose: Short-term needs and emergency reserves (under 5 years)

- Vehicles: Savings accounts, money market accounts, CDs

- Returns: 0.5-5% annually depending on account type and rates

- Risk: Virtually none (FDIC insured up to $250,000)

- Liquidity: Immediate or near-immediate access

- Volatility: Stable, no value fluctuation

Investing characteristics:

- Purpose: Long-term wealth building and goals (5+ years, preferably 10+)

- Vehicles: Stocks, bonds, mutual funds, ETFs, real estate

- Returns: 6-12% average annually (stocks historically 10%)

- Risk: Principal can decrease, potential temporary or permanent losses

- Liquidity: Varies (stocks liquid, real estate illiquid)

- Volatility: Significant year-to-year fluctuation including negative years

Appropriate use cases:

Use SAVING for:

- Emergency fund (3-6 months expenses)

- Short-term goals under 3 years (vacation, car down payment)

- Funds needed with certainty within 5 years

- Capital preservation priority over growth

Use INVESTING for:

- Retirement (decades away)

- Long-term goals 5+ years (home down payment, education)

- Wealth building beyond inflation

- Growth priority accepting volatility

How Investing Creates Wealth

The compound return principle:

- Year 1: Invest $10,000, earn 10% = $11,000

- Year 2: $11,000 earns 10% = $12,100 (earning returns on previous returns)

- Year 3: $12,100 earns 10% = $13,310

- Year 10: $25,937 (without adding any money beyond initial $10,000)

- Year 20: $67,275

- Year 30: $174,494

Regular contributions amplify compounding:

- Monthly investment: $500

- Return: 8% annually

- 10 years: $91,473 contributed $60,000, gains $31,473

- 20 years: $294,510 contributed $120,000, gains $174,510

- 30 years: $745,180 contributed $180,000, gains $565,180

Comparison: Investing versus saving same amounts:

$500 monthly invested at 8% (30 years):

- Total contributed: $180,000

- Final value: $745,180

- Returns gained: $565,180 (307% of contributions)

$500 monthly saved at 1% (30 years):

- Total contributed: $180,000

- Final value: $210,000

- Returns gained: $30,000 (17% of contributions)

Wealth difference: $535,180 from investing versus saving

The Risk-Return Relationship

Fundamental investment principle: Higher potential returns require accepting higher risk

Risk-return spectrum:

- Savings accounts: 0.5-1% return, virtually zero risk

- CDs and bonds: 3-5% return, minimal to low risk

- Balanced funds: 6-7% return, moderate risk

- Stock market index: 8-10% return, moderate-high risk

- Individual stocks: -100% to +500%+ return, high risk

- Speculative investments: Unlimited upside/downside, very high risk

Understanding risk means:

- Volatility: Value fluctuates daily, monthly, annually

- Temporary losses: Portfolio may decrease 20-50% during downturns

- Recovery requirement: Needing years to regain previous values

- No guarantees: Past performance doesn’t ensure future results

Historical stock market volatility example:

- 2008 financial crisis: -37% year

- 2009 recovery: +26% year

- Average bull market: +114% over 4-5 years

- Average bear market: -36% over 1-2 years

- Long-term average despite volatility: 10% annually

Types of Investments

Stocks (Equities)

What stocks are:

- Ownership shares in companies

- Buy Apple stock = own tiny portion of Apple

- Value rises/falls with company performance and market sentiment

- Profits through: Price appreciation (buy $100, sell $150) and dividends (quarterly payments)

Stock return potential:

- Historical average: 10% annually (S&P 500 index)

- Individual stocks: -100% (bankruptcy) to +1,000%+ (exceptional growth)

- Dividends: 1-4% annually typical for dividend-paying stocks

Stock risks:

- High volatility (daily price swings 1-5% common)

- Company-specific risk (poor management, competition, disruption)

- Market risk (entire market declines affecting all stocks)

- No principal guarantee (can lose entire investment)

Bonds (Fixed Income)

What bonds are:

- Loans to governments or corporations

- Buy bond = lend $1,000 to issuer for set period

- Receive regular interest payments (coupon)

- Principal returned at maturity date

Bond return characteristics:

- Government bonds: 3-5% annually typical (low risk)

- Corporate bonds: 4-7% annually (moderate risk)

- Returns through: Regular interest payments plus principal return

- Less volatile than stocks but lower returns

Bond advantages:

- Predictable income stream

- Lower volatility than stocks

- Portfolio balance during stock declines

- Principal preservation focus

Mutual Funds and ETFs

How pooled investments work:

- Mutual funds/ETFs: Baskets containing dozens to thousands of stocks/bonds

- Professional management or index tracking

- Instant diversification (one purchase = hundreds of holdings)

- Accessible to small investors ($100-1,000 minimums)

Index funds (most recommended for beginners):

- Track market indexes (S&P 500, Total Market)

- Low fees (0.03-0.20% annually typical)

- Automatic diversification (500-3,000+ stocks)

- Passive management (no stock picking)

- Historical returns match market (10% annually long-term)

Example index fund:

- Vanguard Total Stock Market Index (VTSAX)

- Contains 3,500+ U.S. stocks

- Fee: 0.04% annually ($4 per $10,000 invested)

- Returns: Matches total U.S. stock market performance

- Diversification: Instant exposure to entire market

Real Estate

Real estate investment approaches:

- Rental properties: Direct ownership generating rental income

- REITs (Real Estate Investment Trusts): Stock-like ownership of property portfolios

- Real estate crowdfunding: Pooled investments in properties

Real estate advantages:

- Tangible asset providing shelter utility

- Leverage potential (mortgages amplifying returns)

- Income generation through rents

- Tax benefits (depreciation, deductions)

Real estate challenges:

- High capital requirements ($20,000-100,000+ down payments)

- Illiquidity (months to sell, transaction costs 6-10%)

- Active management (tenants, maintenance, repairs)

- Geographic concentration risk

Why People Invest

Retirement Security

The retirement challenge:

- Life expectancy: 20-30 years in retirement

- Social Security: $1,500-2,500 monthly typical (insufficient alone)

- Living expenses: $3,000-5,000+ monthly retirement needs typical

- Gap: $18,000-30,000 annually requiring personal savings/investments

Investment necessity for retirement:

- $1 million retirement goal common for comfortable retirement

- Achieving through saving alone: Requires $2,800 monthly for 30 years (impossible for most)

- Achieving through investing: Requires $700 monthly for 30 years at 8% (achievable)

- Investment returns provide 73% of final value ($700K+ from $252K contributions)

Beating Inflation

Inflation impact on cash/savings:

- Inflation average: 2-3% annually

- Savings account: 0.5-1% interest

- Real return: -1.5% annually (losing purchasing power)

- $100,000 in savings loses 18% purchasing power over 10 years at 2% inflation

Investment returns outpace inflation:

- Stock returns: 10% nominal, 7-8% after inflation

- Bond returns: 4-5% nominal, 2-3% after inflation

- Maintains and grows purchasing power over time

Wealth Building Beyond Earned Income

Income limitations:

- Salary cap: Maximum earnings limited by hours, position, market

- Time for money: Income stops when stop working

- Linear growth: Modest raises 2-5% annually typical

Investment compound acceleration:

- Works 24/7 regardless of employment status

- Exponential growth through compounding

- Passive income potential (dividends, interest, rents)

- Eventual financial independence when investments generate sufficient income

Comparison 30-year wealth building:

Earned income only ($60,000 salary):

- 3% annual raises over 30 years

- Final salary: $145,000

- Total earnings: $2.7 million

- Net worth if saved 10%: $450,000

Earned income + investing:

- Same salary progression

- Invest 15% income ($750 monthly initially, increasing with raises)

- Total invested: $540,000 over 30 years

- Final investment value at 8%: $1,650,000

- Net worth: $1,650,000 (3.7x higher through investing)

Investment Vehicles and Accounts

Retirement Accounts (Tax-Advantaged)

401(k) (employer-sponsored):

- Contribution limit: For 2026, the IRS announced that the 401(k) contribution limit for employees increases to $24,500 (up from $23,500 in 2025). Individuals aged 50 and older can make additional catch-up contributions of $8,000, bringing their total potential contribution to $32,500. A special, higher catch-up limit of $11,250 applies for those aged 60 to 63/li>

- Tax benefit: Pre-tax contributions (reduce current taxable income)

- Employer match: Free money (50-100% of contributions up to 3-6% salary typical)

- Investment options: Limited selection chosen by employer (typically 10-30 mutual funds)

- Withdrawal: Penalty-free after 59½, taxed as ordinary income

IRA (Individual Retirement Account):

- Contribution limit: For 2026, the IRA contribution limit increases to $7,500 ($8,600 for age 50 or older). This applies to the combined total of traditional and Roth IRA contributions. Taxpayers must have earned income to contribute, and higher income levels may phase out eligibility to make direct Roth contributions

- Types: Traditional (pre-tax contributions) or Roth (after-tax contributions)

- Tax benefit: Traditional reduces current taxes, Roth provides tax-free retirement withdrawals

- Investment options: Unlimited (any stocks, bonds, funds available)

- Flexibility: Open at any brokerage, full investment control

Roth IRA advantages:

- Tax-free growth and withdrawals in retirement

- No required distributions at any age

- Contributions (not earnings) withdrawable anytime penalty-free

- Ideal for young investors in low tax brackets

Taxable Brokerage Accounts

Characteristics:

- No contribution limits (invest unlimited amounts)

- No withdrawal restrictions (access anytime without penalties)

- Capital gains taxes on profits when sold

- Dividend and interest income taxed annually

- Use for: Goals before retirement, additional savings beyond retirement limits

Tax implications:

- Long-term capital gains (held 1+ years): 0-20% tax depending on income

- Short-term capital gains (held under 1 year): Taxed as ordinary income

- Dividends: 0-20% qualified dividend rate

Common Investment Platforms

Traditional brokerages:

- Vanguard: Low-cost index funds, excellent for passive investors

- Fidelity: Comprehensive options, good tools and research

- Charles Schwab: Full-service, broad investment selection

Modern platforms:

- Robinhood: Simple interface, fractional shares, commission-free

- M1 Finance: Automated portfolio management, fractional shares

- Betterment/Wealthfront: Robo-advisors with automated management

Platform selection considerations:

- Fees: Prefer $0 commission platforms, low expense ratio funds (under 0.20%)

- Investment options: Ensure access to low-cost index funds

- Account types: Verify IRA, Roth IRA, taxable account availability

- User experience: Choose interface matching comfort level

Getting Started with Investing

Prerequisites Before Investing

Financial foundation requirements:

- High-interest debt eliminated (credit cards over 8-10% APR)

- Emergency fund established ($1,000 minimum, 3-6 months ideal)

- Budget sustainable (spending less than earning consistently)

- Employer 401(k) match captured (if available)

Why foundation matters:

- Credit card at 18% APR costs more than stock market gains (paying 18% versus earning 10% = -8% net)

- No emergency fund forces selling investments at loss during crisis

- Budget deficit prevents consistent investing (requires surplus)

Beginner Investment Strategy

Recommended starting approach:

Step 1: Maximize 401(k) match (free money)

- Contribute minimum required for full employer match

- Example: Employer matches 50% up to 6% salary = contribute 6% minimum

- Instant 50-100% return through match

Step 2: Open Roth IRA and invest in index funds

- Choose platform: Vanguard, Fidelity, or Schwab

- Open Roth IRA online (15-30 minutes)

- Select total market index fund (VTSAX, FSKAX, SWTSX)

- Set up automatic monthly contributions ($100-500+ depending on budget)

Step 3: Increase contributions toward 15% total income

- Combine 401(k) and IRA contributions

- Goal: 15% gross income to retirement investing

- Example: $60,000 income = $9,000 annually = $750 monthly

Beginner portfolio allocation:

- Ages 20-35: 100% stock index fund (maximize growth, long timeline)

- Ages 35-50: 90% stocks, 10% bonds (slight stability addition)

- Ages 50-60: 70-80% stocks, 20-30% bonds (increased stability approaching retirement)

- Ages 60+: 50-60% stocks, 40-50% bonds (preservation focus)

Common Beginner Mistakes to Avoid

Mistake 1: Waiting for “perfect time” to invest

- Problem: Delaying while trying to time market bottoms

- Reality: Time in market beats timing market

- Solution: Start immediately with available funds, invest regularly regardless of market conditions

Mistake 2: Panic selling during downturns

- Problem: Selling when portfolio down 20-30% locking in losses

- Reality: Market recovers over time, selling prevents recovery gains

- Solution: Maintain long-term perspective, continue investing during declines (buying discounted shares)

Mistake 3: Chasing hot stocks or trends

- Problem: Buying individual stocks or sectors after dramatic rises

- Reality: 80% of active stock pickers underperform index funds long-term

- Solution: Stick with diversified index funds avoiding speculation

Mistake 4: Excessive trading and monitoring

- Problem: Daily checking, frequent buying/selling

- Reality: Transaction costs and poor timing reduce returns

- Solution: Set-and-forget approach, check quarterly or annually

Mistake 5: Investing before emergency fund

- Problem: All savings in market, forced selling during emergencies

- Reality: Emergencies occur, selling at loss destroys compound growth

- Solution: $1,000-3,000 minimum cash buffer before aggressive investing

Why Understanding Investing Matters

Without understanding what investing is, individuals miss compound return benefits accumulating $500,000-2,000,000 additional lifetime wealth through decades of market participation versus cash-only saving yielding $200,000-400,000 same contributions, lack retirement security relying solely on insufficient Social Security ($1,500-2,500 monthly) versus investment income supplementation ($3,000-5,000 monthly) enabling comfortable lifestyle, and lose purchasing power to inflation eroding savings real value 20-30% over decades—while investment-literate individuals harness 8-10% stock returns building substantial wealth through patient long-term commitment, diversified index fund allocation avoiding individual stock speculation, and disciplined contribution consistency regardless of market volatility, creating retirement security and financial independence impossible for non-investors regardless of income level when earned income alone and cash savings insufficient generating prosperity requiring compound return participation impossible to achieve through labor or guaranteed accounts prioritizing capital preservation over growth necessary for long-term wealth accumulation.

Understanding what investing is enables individuals to:

- Distinguish investing from saving recognizing appropriate use cases and return expectations

- Harness compound returns through long-term market participation creating wealth multiplication

- Select appropriate investment vehicles (index funds, 401k, IRAs) matching goals and timelines

- Accept calculated risks understanding volatility temporary requiring patience not panic

- Start early maximizing compound time advantage creating $100,000-300,000 additional wealth from 10-year head start

- Avoid common mistakes (timing market, panic selling, excessive trading) destroying returns

- Build retirement security through systematic investing impossible via earned income alone

Investment knowledge transforms wealth building from income-dependent impossibility into systematic achievable process through market participation, enabling prosperity and retirement security regardless of salary level when compound returns provide 60-70% of final retirement wealth from contributions representing 30-40% demonstrating investment understanding as essential wealth-building prerequisite impossible for cash-only savers when inflation erodes value faster than savings interest accumulates.

Common Misunderstandings

Many people view investing as gambling or speculation requiring luck and market timing. In reality, disciplined long-term index fund investing produces predictable wealth through historical 8-10% average returns over decades despite year-to-year volatility, with time in market and consistent contributions creating reliable compounding—$500 monthly invested over 30 years yields $650,000-850,000 with 95%+ probability based on historical data versus gambling’s negative expected returns and pure chance outcomes, proving systematic investing wealth-building strategy not speculation when diversified across entire markets through index funds avoiding individual stock picking requiring skill or luck.

Another common misconception is investing requires large amounts making participation impossible for average earners. In practice, modern fractional share investing and low account minimums enable starting with $50-100 monthly building substantial wealth—$100 monthly from age 25-65 grows to ~$349,100 at 8% returns demonstrating accessibility at any income level, with consistency and time more important than contribution size making $100 monthly for 40 years creating more wealth than $1,000 monthly for 10 years ($349K versus $183K) proving early modest start superior to delayed large contributions making investing accessible not exclusive regardless of current income when small consistent amounts compound dramatically over decades.

Some believe market crashes destroy investment wealth requiring avoidance or selling to prevent losses. However, market recoveries historically occur within 1-5 years with portfolios reaching new highs—2008 crash dropped markets 50% but recovered by 2012 and tripled by 2020, proving patient investors recovered and prospered while panic sellers locked in permanent losses missing recovery gains, demonstrating crashes temporary setbacks not permanent destruction when maintaining long-term investment horizon and continuing contributions buying discounted shares during declines creating superior outcomes versus attempting market timing through selling low and missing recovery buying high making volatility acceptance essential not reason avoiding investing altogether.

How Investment Understanding Fits Into Financial Success

Investment understanding enables wealth multiplication through compound returns creating $500,000-2,000,000 retirement security from $200,000-400,000 lifetime contributions, provides purchasing power protection through 7-8% real returns exceeding 2-3% inflation preventing cash erosion, and creates financial independence potential when investment income eventually replaces earned income enabling career flexibility—making investment literacy essential wealth-building component requiring early start maximizing compound time benefits, consistent contributions through market cycles regardless of volatility, and diversified index fund allocation avoiding speculation, transforming retirement from Social Security dependence and continued employment into comfortable security through systematic market participation impossible for cash-only savers when earned income alone insufficient and inflation erodes purchasing power faster than savings interest accumulates creating wealth-building necessity not optional enhancement for comfortable prosperous retirement regardless of income level.

For example, two individuals both age 25 earning $50,000 annually. Person A lacks investment understanding, fears stock market volatility and complexity, keeps all savings in bank accounts earning 1% interest. Saves diligently $400 monthly for 40 years demonstrating discipline. Age 65: Contributed $192,000 total, final savings value ~$236,000 including $45,000 interest (inflation averaged 2.5% annually meaning purchasing power actually declined in real terms). Social Security provides $2,200 monthly, savings withdrawal $787 monthly ($236,000 ÷ 300 months estimated retirement), total retirement income $2,987 monthly requiring budget reduction from working years, cannot help children or grandchildren financially, outlives savings age 90 forcing sole Social Security reliance final years. Person B understands investing fundamentals, overcomes initial fear through education recognizing long-term market reliability despite volatility. Age 25: Opens Roth IRA at Vanguard, invests $400 monthly in total stock market index fund (VTSAX). Age 26-65: Continues $400 monthly regardless of market ups and downs, Experiences 2008-style crashes and recoveries, maintains discipline never selling during downturns. Age 65: Contributed $192,000 total, final investment value $1,396,403 at 8% average returns despite volatility. Social Security provides $2,200 monthly, investment withdrawal $4,654 monthly (4% safe withdrawal rate from $1,396,403), total retirement income $6,854 monthly enabling comfortable lifestyle, helps grandchildren education $50,000 without impacting retirement security, leaves $800,000 inheritance to family demonstrating generational wealth transfer. Difference: Person A’s cash-only saving created $236,000 with inflation-eroded purchasing power and retirement income inadequacy requiring lifestyle reduction, Person B’s investment understanding created $1,396,403 (5.8x higher) from similar contribution discipline demonstrating $1,160,403 wealth differential plus $3,867 monthly additional retirement income ($6,854 versus $2,987) from understanding compound returns, accepting calculated volatility risk, and maintaining long-term discipline impossible without investment literacy enabling market participation creating prosperity impossible through earned income and cash savings alone when inflation and insufficient returns prevent wealth accumulation regardless of savings discipline.

Investment understanding separates wealthy comfortable retirees from financially-struggling continued workers, requiring education overcoming fear and complexity, disciplined long-term commitment through volatility, and systematic index fund approach avoiding speculation creating measurable generational wealth differences impossible without investment literacy.

Recent Updates and Trends

In recent years, commission-free trading has become universal through platforms like Robinhood, Fidelity, and Schwab eliminating transaction costs that previously deterred small investors, though fundamental long-term index investing strategy unchanged with fee elimination enhancing accessibility not altering core wealth-building principles requiring patient multi-decade commitment versus frequent trading enabled by zero commissions creating false perception of day-trading viability destroying wealth through poor timing and speculation.

Fractional share investing has expanded enabling $1 investments in expensive stocks previously requiring $100-1,000+ per share, though benefit primarily psychological accessibility rather than strategic advantage when diversified index funds already provided fractional ownership of thousands of companies making single-stock fractional shares marginal improvement versus critical diversification achieved through funds regardless of fractional capability.

Market volatility has intensified with technology-driven rapid information flow creating sharper faster price movements, though long-term returns unchanged with 8-10% average persisting despite increased short-term fluctuation making volatility acceptance even more critical while fundamental patient investing approach produces identical wealth-building outcomes regardless of intra-year volatility magnitude when maintaining multi-decade holding periods.

Cryptocurrency and alternative investments have gained mainstream attention creating speculation temptation, though traditional stock/bond portfolios remain optimal wealth-building foundation with 90-95% allocation recommended before considering alternatives representing 5-10% portfolio maximum given volatility and unproven long-term track records making core index fund investing unchanged despite alternative proliferation.

Fundamental investing principles remain timeless: compound returns create wealth impossible through saving alone, early start dramatically amplifies outcomes through decades of compounding, diversified index funds provide optimal risk-adjusted returns, patient long-term commitment through volatility essential, and systematic contributions regardless of market conditions produce superior results—regardless of commission elimination, fractional share availability, volatility changes, or alternative investment marketing, understanding basic investing mechanics enabling disciplined index fund commitment produces retirement security impossible for non-investors when earned income and cash savings insufficient regardless of technological conveniences or product proliferation not changing fundamental wealth-building requirements.

3 Things You Can Do Today

Ready to start investing? Here are three simple steps you can take right now:

1. Calculate your retirement gap determining investment necessity and contribution target – Estimate retirement expenses: Current monthly spending typically 70-80% of working years (example: spend $4,500 monthly working, need $3,500 retirement). Calculate Social Security estimate: Use SSA.gov calculator entering work history (typical $1,800-2,500 monthly). Determine gap: Monthly retirement need minus Social Security (example: $3,500 – $2,000 = $1,500 monthly gap = $18,000 annually). Calculate required retirement savings: Annual gap × 25 (4% withdrawal rule, example: $18,000 × 25 = $450,000 needed). Determine current age timeline: Years until retirement 65 (example: age 35 = 30 years). Use investment calculator: Enter 0 current savings, goal amount $450,000, years 30, return rate 8%, calculate required monthly contribution (example result: $301 monthly needed). Compare saving versus investing requirement: Same goal through 1% savings requires $1,072 monthly (impossible for most) versus $301 monthly investing (achievable) demonstrating investment necessity. Write commitment: “Retirement gap: $1,500 monthly ($18,000 annual). Savings needed: $450,000. Timeline: 30 years. Required investment: $301 monthly at 8%. Savings-only requirement: $1,072 monthly (unachievable). Conclusion: Investing essential for retirement security.” Takes 20 minutes revealing specific retirement need and monthly investment target creating concrete actionable goal impossible when vaguely “should invest someday” without quantified necessity understanding.

2. Open Roth IRA at low-cost brokerage and invest first $100-500 in total stock market index fund TODAY – Select brokerage: Choose Vanguard, Fidelity, or Schwab (all excellent low-cost options). Visit website: Navigate to “Open Account” or “Get Started” section. Account type: Select “Roth IRA” (after-tax contributions, tax-free growth). Complete application: Provide SSN, employment, income information (15 minutes online). Fund account: Link checking account, transfer initial $100-500 (or minimum required). Select investment: Search “total stock market index fund” choosing broker’s option (Vanguard VTSAX/VTI, Fidelity FSKAX/ITOT, Schwab SWTSX/VTI). Purchase shares: Enter dollar amount, confirm purchase completing first investment. Set up automatic contributions: Schedule monthly automatic transfer $100-500 (or affordable amount) buying shares automatically. Contribution target: Work toward 15% gross income over time (example: $60,000 salary = $750 monthly goal, start with $200 increasing annually). Investment selection rationale: Total stock market index provides instant diversification across 3,500+ U.S. companies, 0.03-0.04% ultra-low fees maximizing returns, proven long-term 10% historical average, eliminates individual stock selection risk through automatic broad market ownership. Avoid temptation: Do NOT research individual stocks, crypto, or complex strategies initially—total market index optimal for 95% of investors providing superior risk-adjusted returns versus stock picking or sector betting. Write confirmation: “Opened Roth IRA at [Brokerage]. Invested $[amount] in [Fund]. Automatic $[monthly] contributions scheduled. Current allocation: 100% stocks appropriate for age [X]. Next review: [Date one year from now].” Takes 30-60 minutes transforming from investment procrastinator to active investor with actual money working in market impossible when perpetually “planning to invest” without execution creating years of lost compound returns from analysis paralysis.

3. Commit to long-term hold discipline writing down volatility acceptance pledge reviewed during downturns – Write volatility acknowledgment: “I understand stock market declines 20-50% periodically (every 3-10 years typical). This is NORMAL and TEMPORARY, not crisis requiring selling. Historical crashes (2008, 2020, others) always recovered within 1-5 years reaching new highs. Selling during decline locks in losses preventing recovery gains destroying long-term wealth. My timeline: [X] years until retirement providing abundant recovery time from temporary downturns.” Create commitment pledge: “I commit to: (1) Never selling during market decline regardless of portfolio decrease, (2) Maintaining automatic monthly contributions especially during downturns buying discounted shares, (3) Not checking portfolio more than quarterly preventing panic from daily volatility, (4) Trusting decades of market history showing 10% average returns despite volatility, (5) Reviewing this pledge before any emotional selling decision.” Add perspective reminder: “Example: $100,000 invested drops to $70,000 during crash (painful but temporary). Patient holding recovers to $100,000 in 3 years then $150,000 in 6 years = $50,000 gain. Panic selling at $70,000 locks in $30,000 permanent loss missing recovery creating $80,000 total wealth difference ($50,000 gain versus $30,000 loss) from emotional decision destroying decade of discipline.” Store pledge prominently: Save in phone notes, email to self, print and keep with financial documents, set annual calendar reminder reviewing commitment. Share with accountability partner: Tell spouse/friend/family about investment journey and volatility commitment creating external accountability preventing isolated panic selling. Behavioral preparation: Expect feeling uncomfortable during first market decline, recognize discomfort as normal not actionable crisis, refer to written pledge before any selling decision. Historical perspective building: Review 2008 crash and recovery timeline, 2020 COVID crash (34% drop, full recovery 5 months, tripled by 2021), 2000 dot-com crash (50% drop, recovery 5 years, tripled by 2013) demonstrating recovery certainty when patient making current volatility predictable not unprecedented. Write final commitment: “Investing timeline: [X] years. Strategy: Total stock market index. Commitment: Hold through volatility, never sell during decline, maintain automatic contributions, trust historical recovery pattern. Reviewed: [Date]. Next review: [Annual].” Takes 15 minutes creating psychological foundation preventing emotional destruction of long-term wealth impossible when experiencing first 20-30% decline without pre-commitment and perspective preparation creating panic selling locking in losses destroying years of disciplined accumulation through single emotional decision.

These actions create investing foundation within 90 minutes—calculated specific retirement need demonstrating investment necessity ($301 monthly required versus $1,072 savings-only alternative), opened actual Roth IRA with real money invested in total stock market index fund beginning compound return journey, and created volatility commitment pledge preventing panic selling during inevitable future downturns—transforming from non-investor to active market participant with systematic approach impossible when perpetually delaying through analysis paralysis or fear preventing wealth accumulation through decades of lost compound returns.

Quick FAQ

What’s the difference between investing and saving?

Saving preserves money in guaranteed accounts (savings, CDs) earning 0.5-5% for short-term needs under 5 years with no principal risk, while investing allocates money to growth assets (stocks, bonds, funds) earning 6-12% average for long-term goals 5+ years accepting volatility and potential temporary losses: Saving purpose—Emergency fund (3-6 months expenses), short-term goals (vacation, car down payment within 3 years), funds needed with certainty soon. Investing purpose—Retirement decades away, long-term goals 5+ years (home down payment, education), wealth building outpacing inflation. Return comparison—$500 monthly over 30 years: Saving at 1% = $209,000 total, Investing at 8% = ~$745,180 total, difference $536,180 demonstrating investment necessity for substantial wealth building. Risk difference—Saving guarantees principal preservation but loses purchasing power to inflation, investing risks temporary declines but historically recovers creating superior long-term outcomes when patient. Liquidity difference—Savings immediately accessible, some investments liquid (stocks sold same day) while others illiquid (real estate requiring months). Appropriate allocation—Maintain 3-6 months expenses in savings (safety), invest remainder for long-term goals (growth). Key insight: Saving and investing complementary not competing, optimal strategy uses both appropriately (savings for safety/short-term, investing for growth/long-term) creating balanced financial foundation impossible when using only one exclusively.

How much money do I need to start investing?

Can start investing with $100-500 initially through low-minimum brokerages and fractional shares, though consistency more important than starting amount with $50-200 monthly systematic contributions building substantial wealth over decades: Minimum requirements today—Many brokerages $0 account minimum (Fidelity, Schwab, Robinhood), index fund minimums $1-3,000 initially (Vanguard VTSAX $3,000) BUT ETF versions available for single share price $100-400 (VTI, ITOT), fractional shares enable investing any amount $1+ at some brokerages. Realistic starting approach—If have $500-1,000 available: Open Roth IRA, invest lump sum, add $100-300 monthly automatic contributions. If have under $500: Start with $100-200, add $50-100 monthly, building to larger amounts over time. Contribution target progression—Start: Whatever affordable $50-200 monthly, Goal: 15% gross income over time (example $60,000 = $750 monthly = 15%), increase contributions 1% salary annually approaching goal gradually versus attempting unsustainable large initial amount. Example wealth building—$100 monthly age 25-65 = $349,100 at 8%, demonstrating modest consistent contributions create substantial wealth versus requiring large lump sum. Employer 401(k) consideration—If available, even $50-100 monthly captures partial match providing instant 50-100% return making minimal contributions worthwhile. Key: Start TODAY with available amount (even $50-100) rather than waiting years to save “enough” losing compound time worth far more than initial dollar amount given decades of growth potential.

What if the stock market crashes right after I invest?

Continue holding and investing through decline buying discounted shares creating superior long-term wealth versus selling or stopping, as historical crashes always recover within 1-5 years reaching new highs benefiting patient disciplined investors: Crash reality—Market declines 20-50% occur every 3-10 years throughout investing lifetime, inevitable not avoidable, temporary not permanent when maintaining long-term timeline. Historical pattern—2020 COVID: 34% drop March, full recovery August (5 months), +100% by 2021. 2008 financial crisis: 50% drop, full recovery 2012 (4 years), +200% by 2020. 2000 dot-com: 50% drop, recovery 2006 (6 years), +200% by 2019. Every crash followed by recovery proving pattern reliability. Optimal response—Continue automatic monthly contributions buying shares at 30-50% discount (dollar cost averaging), never sell locking in losses, maintain long-term perspective (20-40 year retirement timeline provides abundant recovery time), review volatility commitment pledge reinforcing discipline. Worst case timing—Invest $10,000 at market peak before 50% crash dropping to $5,000, feel terrible seeing loss. Options: (A) Panic sell at $5,000 locking in $5,000 permanent loss never participating in recovery, (B) Hold patiently, recover to $10,000 in 4 years, grow to $20,000 in 10 years, $43,000 in 20 years demonstrating $38,000 wealth difference from discipline ($43,000 versus $5,000) making holding essential. Additional contribution advantage—If continue $500 monthly during crash and recovery: Original $10,000 becomes $43,000, PLUS additional $120,000 contributed over 20 years becomes $280,000 (buying many shares during crash discount) = $323,000 total demonstrating crash as opportunity not crisis for disciplined systematic investors. Protection: Maintain emergency fund ensuring never forced selling investments during decline due to job loss or expense requiring cash, preventing worst-case forced liquidation at bottom. Key: Market timing impossible (cannot predict crashes or recoveries), patient holding through volatility produces superior outcomes versus attempting avoidance missing years of gains waiting for “perfect entry” or panicking during inevitable declines destroying wealth through emotional decisions.

Should I invest in individual stocks or index funds?

Index funds strongly recommended for 95% of investors providing superior risk-adjusted returns through diversification, minimal fees, and proven long-term performance versus individual stocks requiring research, accepting concentration risk, and statistically underperforming indexes: Index fund advantages—Instant diversification (own 500-3,500+ companies single purchase), ultra-low fees (0.03-0.20% annually versus 1-2% actively managed funds), match market returns historically 10% average, eliminate stock-picking skill requirement, reduce company-specific bankruptcy risk. Individual stock disadvantages—Concentration risk (company bankruptcy = 100% loss), research requirement (financial statement analysis, industry trends, competitive analysis), emotional attachment creating poor decisions, 80% of professional stock pickers underperform index long-term (if experts fail, individuals face worse odds), time intensive monitoring and decision-making. Performance comparison—$10,000 invested 20 years: S&P 500 index = $67,000 average, active stock pickers = $45,000 average (underperformance from fees and poor picks), lucky individual stock (Amazon, Apple, etc.) = $200,000+ BUT risk of losers (Enron, Lehman = $0) making survivorship bias misleading. Appropriate individual stock use—After building substantial index fund portfolio ($100,000+), can allocate 5-10% to individual stock speculation for learning/entertainment accepting risk, never making individual stocks primary strategy. Recommended approach—Ages 20-60: 100% index funds (total stock market or S&P 500), adding bond index approaching retirement, avoiding individual stock temptation entirely. Exception: Employer stock in 401k creating overconcentration, should diversify rather than hold employer stock beyond 5-10% preventing Enron-style disasters (employees lost retirement when company bankrupt). Key: Index fund “boring” strategy produces superior outcomes through consistency and low costs versus exciting individual stock picking destroying wealth through fees, poor timing, and concentration risk, making simplicity and discipline more valuable than complexity and stock selection attempts.

When should I start investing?

Start TODAY (or as soon as high-interest debt eliminated and $1,000 emergency fund established) as every year delayed costs $20,000-100,000+ in lost compound returns making early start dramatically more valuable than contribution amount: Time advantage demonstration—$200 monthly age 25-35 (only 10 years contributing $24,000 total) then stop = $368,185 age 65 at 8%. Same $200 monthly age 35-65 (30 years contributing $72,000 total) = $298,072 age 65. Early starter accumulated $70,113 MORE despite contributing $48,000 LESS proving 10-year head start worth more than tripled contribution period through compound time advantage. Delay cost—Each year delayed age 25-35 costs approximately $50,000-80,000 final retirement wealth, making “starting next year” extremely expensive procrastination. Exception: High-interest debt—If carrying credit cards over 8-10% APR, pay off aggressively first (attacking 18% debt = guaranteed 18% return superior to stock market 10% expected), then start investing avoiding paying 18% while earning 10% creating -8% net result. Minimum foundation—$1,000 emergency fund preventing forced investment liquidation during car repair or medical expense, eliminating high-interest consumer debt, sustainable budget spending less than earning enabling consistent contributions. Starting small perfectly acceptable—$50-100 monthly starting immediately beats $500 monthly starting 5 years later due to compound time advantage, increase contributions annually as income grows versus waiting for “enough money” losing critical early years. Common delay excuses—”Don’t know enough” (total stock market index requires zero stock knowledge), “Markets too high” (impossible to predict, time in market beats timing market), “Will start after [life event]” (life always has events, start today regardless). Real-world 40-year comparison—Start $300 monthly age 25 = $1,047,302 age 65. Delay starting to age 35 same $300 monthly = $447,107 age 65. Delay cost: $600,195 from 10-year procrastination proving immediate start essential regardless of economic conditions or personal circumstances when compound time advantage worth hundreds of thousands creating urgency impossible to recover through higher contributions later.

Explore More in Investing Basics

Disclosure

This article provides general educational information about investing concepts, principles, and strategies. Individual investment decisions, appropriate strategies, asset allocations, and outcomes vary significantly based on personal circumstances including age, income, risk tolerance, financial goals, time horizon, and tax situation. This is not financial advice, investment recommendation, endorsement of specific products or platforms, or guarantee of investment returns or outcomes. All investments carry risk including potential loss of principal invested. Past performance does not guarantee future results and should not be sole basis for investment decisions. Stock market historical returns averaging 8-10% annually include significant year-to-year volatility with negative years occurring regularly—individual experiences may differ substantially. Investment examples and scenarios represent typical situations with assumptions about returns, contribution amounts, and timelines—actual results will vary based on market performance, individual behavior, and economic conditions. Tax implications of different account types vary by individual circumstances—contribution limits, deductibility, and withdrawal rules subject to change. Employer 401(k) match percentages and vesting schedules vary by company. Platform and brokerage comparisons based on current offerings as of article date—features, fees, and available investments change over time. Investment account minimums and fractional share availability vary by platform. Retirement planning calculations require assumptions about Social Security benefits, life expectancy, expenses, and inflation—actual needs differ. 4% safe withdrawal rate represents general guideline not guarantee of sustainable retirement income. Emergency fund recommendations represent general guidance—appropriate amounts vary by individual risk factors and circumstances. Debt elimination timing before investing represents general framework—individual situations may warrant different approaches. Age-based asset allocation suggestions represent common guidelines not personalized recommendations. Cryptocurrency and alternative investments carry additional risks beyond traditional securities. Some investment strategies and products not suitable for all investors. Consult qualified financial advisors, investment professionals, certified financial planners, or tax professionals for personalized guidance matching individual circumstances, goals, and risk tolerance before making investment decisions. Investment success requires sustained discipline, appropriate risk management, and long-term commitment beyond basic knowledge. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.