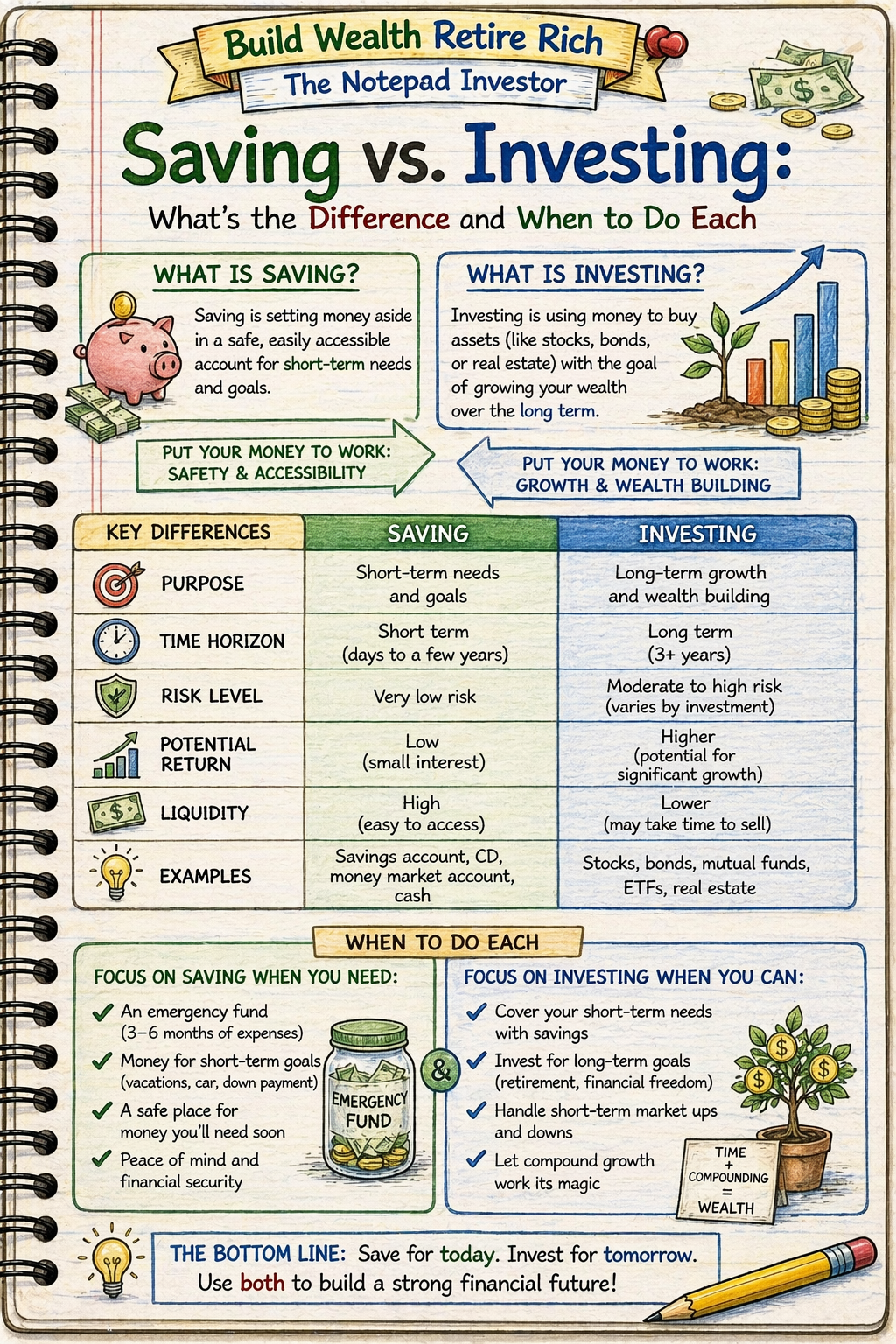

Saving versus investing represents fundamental financial choice determining wealth trajectory over decades—saving preserves money in guaranteed low-return accounts (savings, CDs) earning 0.5-5% annually protecting principal for short-term needs under 5 years, while investing allocates money to growth assets (stocks, bonds, funds) earning 6-12% average accepting volatility and potential temporary losses for long-term goals 5+ years enabling wealth multiplication impossible through savings alone. Representing complementary not competing strategies requiring both for optimal financial health—emergency fund and short-term goal money belongs in savings providing stability and liquidity, while retirement and long-term wealth building requires investing harnessing compound returns outpacing inflation creating prosperity impossible through cash preservation. Understanding appropriate allocation transforms financial outcomes dramatically—$500 monthly over 30 years yields $210,000 in savings at 1% versus $745,000 invested at 8% demonstrating $535,000 wealth differential from strategic choice, proving saving-only approach condemns individuals to inflation-eroded purchasing power and retirement inadequacy while investing-only approach creates emergency vulnerability forcing crisis liquidations destroying long-term wealth, making saving-investing balance essential not optional for financial security requiring honest assessment matching money purpose with appropriate vehicle maximizing both safety and growth impossible when using single strategy exclusively.

This article is designed for anyone confused about saving versus investing distinctions, individuals keeping all money in savings fearing market risk, or investors neglecting emergency funds creating vulnerability. You do not need financial expertise to understand saving-investing differences—fundamental concepts accessible through clear explanations of return expectations, risk profiles, appropriate timelines, and strategic allocation, though requires honest goal assessment determining which money needed short-term (savings) versus long-term (investing), realistic risk tolerance recognizing comfort with volatility versus preference for guarantees, and disciplined execution maintaining both strategies simultaneously not abandoning one for other, making saving-investing literacy requiring both mechanical understanding (returns, vehicles, accounts) and strategic wisdom (appropriate allocation, timeline matching, balanced approach) impossible when viewing as either/or choice versus complementary foundation requiring both for comprehensive financial security.

Understanding saving versus investing matters because appropriate allocation creates $300,000-700,000 additional lifetime wealth through investing long-term money versus leaving in savings losing purchasing power to inflation, while simultaneous emergency fund maintenance prevents crisis liquidations during market downturns protecting compound growth from forced selling at losses, and strategic balance enables both stability (3-6 months expenses readily accessible) and prosperity (retirement wealth through decades of compound returns)—while financially-literate individuals maintain $15,000-30,000 emergency savings PLUS $500,000-2,000,000 retirement investments creating comprehensive security impossible for savings-only individuals accumulating $200,000-400,000 over lifetime eroded by inflation, or investing-only individuals facing forced liquidations during emergencies destroying years of discipline through single crisis, demonstrating saving-investing balance as essential wealth-building foundation not simplistic choice requiring nuanced strategic allocation impossible without understanding fundamental differences enabling informed purposeful money placement.

Educational disclaimer: This article provides general educational information about saving and investing strategies. Individual appropriate allocations, timelines, and strategies vary significantly based on circumstances including age, income, goals, risk tolerance, and financial obligations. This is not financial advice or specific recommendation of savings/investment ratios. Investment returns represent historical averages with significant volatility—actual results vary. Emergency fund recommendations represent general guidelines not personalized assessments. Consult qualified financial advisors for guidance matching individual situations.

Fundamental Differences

Saving Characteristics

Purpose and timeline:

- Emergency fund (3-6 months living expenses)

- Short-term goals under 3 years (vacation, car down payment, wedding)

- Irregular expense reserves (property taxes, insurance, home maintenance)

- Money needed with certainty within 5 years

Common savings vehicles:

- High-yield savings accounts: 0.5-5% APY depending on Fed rates

- Money market accounts: 0.5-5% APY, check-writing capability

- Certificates of Deposit (CDs): 2-5% APY, fixed terms 3 months-5 years

- All FDIC insured up to $250,000 per account

Savings advantages:

- Principal guaranteed (FDIC insurance prevents loss)

- Immediate liquidity (access within 0-3 days typical)

- Zero volatility (balance never decreases)

- Predictable returns (stated interest rate known upfront)

- No market knowledge required

- Peace of mind from stability

Savings limitations:

- Low returns barely outpacing or trailing inflation

- Purchasing power erosion over decades

- Insufficient for retirement wealth building

- Opportunity cost of foregone investment gains

Investing Characteristics

Purpose and timeline:

- Retirement (20-40 years away)

- Long-term goals 5+ years (home down payment, education)

- Wealth building beyond inflation

- Financial independence and passive income

Common investment vehicles:

- Stock index funds: 8-12% average annual returns historically

- Bond funds: 3-6% average returns, lower volatility

- Target-date retirement funds: Age-appropriate stock/bond mix

- Real estate: 8-10% average returns through appreciation and rents

Investing advantages:

- High long-term returns outpacing inflation substantially

- Compound growth multiplying wealth over decades

- Passive income potential (dividends, interest)

- Retirement security through wealth accumulation

- Purchasing power protection and growth

Investing limitations:

- Volatility creating temporary losses (20-50% declines possible)

- No principal guarantee (can lose money)

- Requires long timeline for recovery from downturns

- Liquidity varies (stocks liquid, real estate illiquid)

- Emotional discipline needed during market crashes

Side-by-Side Comparison

Return expectations:

- Savings: 0.5-5% annually (currently ~4-5% high-yield savings)

- Investing: 6-12% annually average (stocks ~10%, bonds ~4-6%, balanced ~7-8%)

Risk profile:

- Savings: Zero principal loss risk, inflation purchasing power loss

- Investing: Temporary market loss 20-50%, long-term gain high probability

Timeline appropriateness:

- Savings: Under 5 years ideal, essential under 3 years

- Investing: 5+ years minimum, 10+ years ideal

Liquidity:

- Savings: Immediate to 3-day access typical

- Investing: Varies (stocks 2-3 days, real estate months, retirement accounts penalties before 59½)

Tax treatment:

- Savings: Interest taxed as ordinary income annually

- Investing: Capital gains preferential rates 0-20%, tax-deferred growth in retirement accounts

The Wealth Impact Over Time

30-Year Wealth Comparison

Scenario: $500 monthly for 30 years

SAVINGS APPROACH (1% interest):

- Monthly contribution: $500

- Total contributed: $180,000

- Interest earned: $30,000

- Final value: $210,000

- Purchasing power adjustment: -25% from 2.5% average inflation = $157,500 in today’s dollars

INVESTING APPROACH (8% returns):

- Monthly contribution: $500

- Total contributed: $180,000

- Investment gains: $553,000

- Final value: $733,000

- Purchasing power: $550,000 in today’s dollars (8% nominal minus 2.5% inflation = 5.5% real)

WEALTH DIFFERENTIAL: $535,180 from investing versus saving

Inflation Impact on Savings

The purchasing power problem:

- Inflation averages 2-3% annually long-term

- Savings rates fluctuate but often trail inflation

- Real return = Nominal return – Inflation

Example erosion:

- $100,000 saved at 1% interest

- Year 10: $110,500 nominal value

- Inflation at 2.5%: Need $128,000 to maintain purchasing power

- Real loss: $17,500 purchasing power (13.7% decline)

Investment protection:

- $100,000 invested at 8%

- Year 10: $216,000 nominal value

- After 2.5% inflation adjustment: $170,814 real value

- Real gain: $45,186 purchasing power increase

The Opportunity Cost

Foregone wealth from savings-only approach:

Example: Age 30-65 (35 years)

- Savings-only: $400 monthly at 1% = ~$201,053

- Investing: $400 monthly at 8% = ~$917,553

- Opportunity cost: $716,000 lifetime wealth foregone

- Retirement income impact: $3,058 monthly (4% withdrawal from $917K) versus $700 monthly ($201K)

The compound difference:

- First 10 years: Investing ahead $21,000 (modest difference)

- Years 11-20: Gap widening, investing ahead $175,000

- Years 21-30: Massive divergence, investing ahead $523,000

- Final 5 years: Gap explodes to $716,000,000 through compound acceleration

Appropriate Allocation Strategy

The Balanced Approach

Step 1: Build emergency fund in savings (3-6 months expenses)

- Calculate monthly essential expenses (housing, food, utilities, insurance, minimum debt payments)

- Multiply by 3-6 months based on job security and family situation

- Single income household: 6 months

- Dual income household: 3-4 months

- Self-employed/commission: 6-12 months

Example emergency fund calculation:

- Monthly essentials: $3,500

- Dual income household target: 4 months

- Emergency fund goal: $14,000 in high-yield savings

Step 2: Save for short-term goals (under 3 years)

- Vacation next year: $3,000

- Car down payment 2 years: $5,000

- Wedding 18 months: $8,000

- Total short-term savings: $16,000

Step 3: Invest everything else for long-term goals

- Retirement (20-40 years away)

- Home down payment (5+ years)

- Children’s education (10+ years)

- Financial independence

Complete Allocation Example

Household: $5,000 monthly income, $3,500 expenses

Available for savings/investing: $1,500 monthly

Phase 1: Emergency fund building (6-12 months)

- Emergency fund needed: $14,000 (4 months expenses)

- Current emergency fund: $2,000

- Gap: $12,000

- Allocation: $1,200 monthly to savings, $300 to investing (capture employer 401k match)

- Timeline: 10 months to complete emergency fund

Phase 2: Balanced savings/investing (ongoing)

- Emergency fund: Complete at $14,000 (maintain, don’t increase)

- Short-term goal savings: $300 monthly for upcoming vacation/car

- Long-term investing: $1,200 monthly to retirement accounts

- Ratio: 20% savings, 80% investing

Phase 3: Retirement approaching (age 50+)

- Emergency fund: Increase to $18,000 (6 months as job loss harder at older age)

- Short-term reserves: $20,000 for home maintenance, travel

- Retirement investing: Maximum contributions $2,000+ monthly

- Gradual shift toward bonds reducing volatility

Age-Based Allocation Guidelines

Ages 20-30 (wealth building foundation):

- Emergency fund: $5,000-15,000 (3-6 months expenses typical at this age)

- Short-term savings: $2,000-5,000 for immediate goals

- Investing: 80-90% of available monthly surplus

- Investment allocation: 100% stocks (aggressive growth, long timeline)

Ages 30-45 (peak accumulation):

- Emergency fund: $15,000-30,000 (higher expenses, family obligations)

- Short-term savings: $5,000-15,000 (kids activities, home repairs)

- Investing: 70-80% of surplus to retirement and education

- Investment allocation: 90-100% stocks

Ages 45-60 (final push):

- Emergency fund: $20,000-40,000 (job loss harder, healthcare costs)

- Short-term savings: $10,000-25,000 (major expenses, aging parents)

- Investing: Maximum 70-85% to catch up on retirement

- Investment allocation: 70-80% stocks, 20-30% bonds (stability increase)

Ages 60+ (preservation focus):

- Emergency fund: $25,000-50,000 (fixed income protection)

- Short-term reserves: $30,000-60,000 (2-5 years living expenses in cash)

- Investing: Remainder in balanced portfolio

- Investment allocation: 40-60% stocks, 40-60% bonds

Common Mistakes and How to Avoid

Mistake 1: Keeping Everything in Savings

The savings-only trap:

- Pattern: $100,000+ in savings earning 1-4%, $0 invested

- Motivation: Fear of market volatility, “safety” preference

- Cost: $50,000-200,000+ in foregone returns over 20-30 years

Example scenario:

- Age 35: $50,000 in savings, adds $500 monthly for 30 years

- All in savings at 2%: Age 65 = $278,000

- If invested at 8%: Age 65 = $783,000

- Cost of fear: $505,000 lifetime opportunity cost

Solution:

- Maintain 3-6 months expenses in savings ($15,000-30,000 typical)

- Invest everything beyond emergency fund

- Accept short-term volatility for long-term wealth

- Remember: 30-year timeline allows multiple market crash recoveries

Mistake 2: Investing Without Emergency Fund

The emergency vulnerability:

- Pattern: $0 savings, 100% income to investing

- Motivation: Maximize returns, “I’ll just use credit cards for emergencies”

- Cost: Forced investment liquidation during crisis, debt accumulation, destroyed compound growth

Example disaster scenario:

- No emergency fund, $30,000 invested in market

- Lose job during market crash (portfolio down 30% to $21,000)

- Need $15,000 for 3 months expenses

- Forced to sell $15,000 worth (71% of remaining portfolio)

- Left with $6,000 invested, missed entire market recovery

- 5 years later: $6,000 would have grown to $21,000 if held

- Plus reaccumulated $10,000 credit card debt at 18% from emergency expenses

Solution:

- Build $1,000 starter emergency fund before aggressive investing

- Expand to 3-6 months expenses before maximizing investments

- Accept temporarily lower investment contributions for stability

- Prevents forced selling and debt creation

Mistake 3: Using Wrong Vehicle for Timeline

Common mismatches:

Mismatch A: Short-term money in stocks

- Scenario: Need $20,000 for home down payment in 18 months

- Mistake: Invest in stock market hoping for 10% returns

- Risk: Market crashes 30% month before purchase, only have $14,000

- Consequence: Lose dream home or forced to delay years

- Correction: Keep in high-yield savings guaranteeing $20,000+ availability

Mismatch B: Long-term retirement money in savings

- Scenario: Age 30, saving for retirement age 65 (35 years)

- Mistake: Keep retirement savings in 2% savings account

- Cost: $400 monthly 35 years = $222,000 saved versus $930,000 invested

- Consequence: Inadequate retirement forcing continued work or lifestyle reduction

- Correction: Invest retirement money in stock index funds accepting volatility

Timeline decision framework:

- Under 2 years: Savings only (100% safety priority)

- 2-5 years: Mostly savings, consider conservative investing if can delay goal

- 5-10 years: Balanced or aggressive investing acceptable

- 10+ years: Aggressive stock investing optimal

Mistake 4: Abandoning Savings After Building Emergency Fund

The ongoing savings need:

- Pattern: Build $15,000 emergency fund, redirect 100% future savings to investing

- Problem: Irregular expenses drain emergency fund repeatedly

- Examples: Annual insurance $2,500, property taxes $3,000, car maintenance $1,500, holiday gifts $1,000

- Total: $8,000 annually in irregular but predictable expenses

- Result: Emergency fund constantly depleted, never stable

Solution: Sinking funds

- Identify annual irregular expenses: $8,000

- Divide by 12: $667 monthly sinking fund contribution

- Separate from emergency fund in dedicated savings

- Prevents emergency fund depletion from predictable expenses

Complete savings allocation:

- Emergency fund: $15,000 maintained (use only for genuine emergencies)

- Sinking funds: $667 monthly for irregular expenses

- Short-term goals: Additional as needed (vacation, car replacement)

- Investing: Remainder after all savings needs covered

Decision Framework

Quick Decision Tree

Question 1: When do I need this money?

- Under 3 years → SAVINGS (high-yield savings or short-term CDs)

- 3-5 years → Mostly SAVINGS, conservative investing if flexible

- 5-10 years → INVESTING (balanced portfolio 60/40 stocks/bonds)

- 10+ years → INVESTING (aggressive 80-100% stocks)

Question 2: Can I afford to lose 20-30% temporarily?

- No, need guaranteed access → SAVINGS

- Yes, have time to recover → INVESTING

Question 3: What’s the money’s purpose?

- Emergency buffer/safety net → SAVINGS

- Specific purchase soon → SAVINGS

- Retirement wealth building → INVESTING

- Long-term goals → INVESTING

Question 4: Do I already have adequate emergency fund?

- No → Priority SAVINGS until 3-6 months expenses secured

- Yes → Shift focus to INVESTING for long-term wealth

Specific Scenario Guidance

Scenario: “I have $10,000 windfall, where should it go?”

Decision process:

- Step 1: Emergency fund adequate? If under $5,000 → Add to savings

- Step 2: High-interest debt? If credit cards over 10% → Pay off debt

- Step 3: Emergency fund complete? Short-term goals funded?

- Step 4: Everything else → Invest in retirement accounts

Example allocation:

- Emergency fund current: $3,000, need $15,000 = $12,000 gap

- Credit card debt: $0

- Short-term goals: Funded

- Windfall allocation: $10,000 to emergency fund (now $13,000), $2,000 remaining gap to fill from monthly income, future windfalls 100% to investing

Scenario: “Should I pause investing to build bigger emergency fund?”

Pause investing when:

- Emergency fund under $1,000 (extreme vulnerability)

- Job instability or layoff risk (build 6-12 months buffer)

- Major life change (baby, moving, career change)

- Income irregular or commission-based needing larger buffer

Maintain balanced approach when:

- Emergency fund $3,000+ covering most emergencies

- Stable employment

- Dual income household

- Can split surplus 70/30 investing/savings building both simultaneously

Scenario: “I’m 50 with $500,000 invested but only $5,000 saved, what now?”

Action plan:

- Immediate: Build emergency fund to $25,000 (6 months expenses at this age/income level)

- Pause retirement contributions temporarily if needed OR

- Balanced: Continue retirement investing but divert 50% of new contributions to emergency fund building

- Timeline: 10-12 months to adequate emergency fund

- Do NOT liquidate investments to build emergency fund (avoid triggering taxes and missing growth)

- Resume full retirement contributions once emergency fund adequate

Why Understanding Saving vs Investing Matters

Without understanding saving versus investing differences, individuals either keep all money in savings losing $300,000-700,000 lifetime wealth to inflation and opportunity costs versus investing long-term funds, or invest everything including emergency money forcing crisis liquidations during market downturns destroying years of compound growth through forced selling at losses, missing strategic balance enabling both stability (accessible emergency reserves) and prosperity (retirement wealth through decades of compound returns)—while financially-literate individuals maintain appropriate allocation with $15,000-30,000 emergency savings providing crisis buffer PLUS $500,000-2,000,000 retirement investments creating comprehensive security impossible for extreme-approach users either accumulating inadequate inflation-eroded savings or facing emergency vulnerability requiring debt or liquidations, demonstrating saving-investing balance as essential wealth-building foundation requiring honest assessment matching money purpose with appropriate vehicle maximizing both safety and growth impossible when using single strategy exclusively creating either poverty through excessive caution or crisis through excessive risk.

Understanding saving versus investing enables individuals to:

- Match money purpose with appropriate vehicle (short-term savings, long-term investing)

- Build emergency fund preventing crisis liquidations protecting compound growth

- Harness investment returns for long-term wealth impossible through savings alone

- Accept calculated risks understanding volatility temporary with adequate timeline

- Allocate strategically based on age, goals, and timeline requirements

- Avoid common mistakes (all savings or all investing extremes)

- Create balanced financial foundation enabling both stability and prosperity

Saving-investing knowledge transforms financial strategy from simplistic single-approach into nuanced balanced allocation, enabling both emergency resilience through accessible reserves and retirement security through compound returns, creating comprehensive financial health impossible when viewing as either/or choice versus complementary strategies requiring both for optimal outcomes.

Common Misunderstandings

Many people view saving as universally “safe” and investing as universally “risky” making savings always preferable for risk-averse individuals. In reality, long-term savings face certain purchasing power loss through inflation erosion creating guaranteed real loss, while long-term investing faces temporary volatility but provides inflation protection and wealth growth with 95%+ positive return probability over 20+ year periods making investing actually “safer” for long-term money despite short-term volatility—$100,000 saved 30 years loses 25% purchasing power guaranteed through 2.5% inflation versus invested $100,000 growing to $1 million through 8% returns despite temporary 20-50% declines during journey, proving “risk” definition depends on timeline not absolute volatility making savings risky for retirement and investing risky for emergencies requiring timeline-appropriate matching not universal risk rankings.

Another common misconception is building large emergency fund ($50,000-100,000+) provides superior security justifying keeping substantial money in low-return savings. However, emergency fund over 6-12 months expenses creates massive opportunity cost through foregone investment returns—$50,000 excess emergency fund earning 2% over 20 years = $74,000 versus invested at 8% = $233,000 representing $159,000 opportunity cost for marginally increased security, proving beyond reasonable 3-6 month buffer creates wealth destruction not protection making $15,000-30,000 emergency fund optimal with remainder invested generating actual long-term security through wealth accumulation versus false security from excessive low-return cash holdings preventing prosperity.

Some believe market timing allows avoiding investing risks through perfect entry and exit timing making volatility avoidable through skillful trading. However, market timing attempts consistently fail with studies showing 80-90% of active timers underperform simple buy-and-hold approaches, missing best 10 market days over 20 years reduces returns 50% yet impossible predicting which days creating missed-recovery risk, and transaction costs plus poor timing decisions destroy wealth faster than volatility acceptance—proving volatility management through long-term holding and continuing contributions during declines produces superior outcomes versus timing attempts creating worse results through missed gains and poor decisions making acceptance not avoidance optimal volatility strategy for long-term investors.

How Saving-Investing Understanding Fits Into Financial Success

Saving-investing understanding enables comprehensive financial security through balanced allocation maintaining emergency accessibility PLUS retirement wealth growth, prevents extreme approaches creating either inadequate savings forcing crisis debt or excessive savings creating opportunity cost poverty, and provides strategic framework matching timeline with vehicle optimizing both stability and prosperity—making saving-investing literacy essential requiring 3-6 months emergency savings protecting against crisis liquidations, investing all long-term money harnessing compound returns creating $500,000-2,000,000 retirement wealth impossible through savings alone, and honest assessment determining appropriate allocation based on timeline not fear or greed, transforming financial strategy from simplistic single-approach into nuanced balanced foundation enabling both emergency resilience and long-term prosperity impossible when viewing as either/or choice versus complementary strategies requiring both for optimal comprehensive security.

Saving-investing understanding separates financially-secure balanced individuals from extreme-approach strugglers, requiring honest timeline assessment, calculated risk acceptance for long-term money, and disciplined emergency fund maintenance creating measurable prosperity differences impossible without strategic allocation literacy.

Recent Updates and Trends

In recent years, high-yield savings rates have fluctuated dramatically with Federal Reserve policy changes creating 0.5% rates in 2021 rising to 4-5% by 2023 then declining to 3-4% by 2026, though fundamental saving-investing distinction unchanged with temporary rate increases not altering long-term wealth-building necessity for investing when savings still trail inflation over decades regardless of current attractive short-term rates making strategic allocation unchanged despite rate environment variations.

Inflation spike 2021-2023 averaging 5-7% annually demonstrated purchasing power erosion vividly when savings accounts earning 0.5-2% created negative 3-5% real returns, though reinforcing investing necessity through inflation protection when stock returns continued outpacing inflation over full period proving investment value during inflationary periods not just low-inflation stability making lessons amplifying fundamental principles not changing strategic approach.

Online high-yield savings proliferation through Ally, Marcus, CIT offering 4-5% rates created savings opportunity improving emergency fund returns, though not justifying larger emergency funds or long-term savings allocations when even 5% trails historical 8-10% stock returns making savings rate improvements enhancing appropriate emergency fund strategy not changing investing primacy for long-term wealth building regardless of improved savings availability.

Market volatility 2020-2026 through COVID crash, recovery, and subsequent corrections tested investor discipline with 30-40% drawdowns occurring multiple times, though reinforcing volatility acceptance importance when patient holders recovered and prospered while panic sellers locked in losses proving fundamental principles through real-world test validating long-term approach not changing strategy despite increased short-term turbulence.

Fundamental saving-investing principles remain timeless: emergency fund 3-6 months in savings provides stability buffer, short-term money under 3 years requires savings protection, long-term money 5+ years demands investing for wealth growth, balanced allocation essential not extreme single-approach, and timeline determines appropriate vehicle not fear or greed—regardless of savings rate fluctuations, inflation spikes, online savings proliferation, or market volatility changes, understanding purpose-based allocation matching timeline with vehicle produces comprehensive security impossible through extreme approaches creating either inadequate wealth from excessive savings or crisis vulnerability from inadequate reserves.

3 Things You Can Do Today

Ready to optimize saving-investing balance? Here are three simple steps you can take right now:

1. Calculate emergency fund target and current gap determining immediate savings priority – Calculate monthly essential expenses: Housing (rent/mortgage, utilities, property taxes, insurance) + Food (groceries only not dining out) + Transportation (car payment, gas, insurance, maintenance minimum) + Insurance (health, life, disability) + Minimum debt payments = total essentials (example: $2,200 housing + $400 food + $450 transport + $300 insurance + $350 debt = $3,700 monthly essentials). Determine target months: Single income household 6 months, dual income 3-4 months, self-employed 6-12 months (example: dual income = 4 months appropriate). Calculate target emergency fund: Essentials × months (example: $3,700 × 4 = $14,800 target). Assess current emergency fund: Current savings readily accessible within 3 days (example: $4,200). Determine gap: Target minus current (example: $14,800 – $4,200 = $10,600 gap). Priority assessment: If gap over $5,000 consider temporarily reducing investment contributions building emergency fund, if gap under $3,000 maintain balanced approach adding $200-400 monthly until complete, if emergency fund adequate (within $1,000 of target) shift focus to investing maximization. Write commitment: “Monthly essentials: $3,700. Emergency fund target: $14,800 (4 months). Current: $4,200. Gap: $10,600. Priority: Build emergency fund $600 monthly plus invest $400 monthly (60/40 split) completing fund in 18 months then shift to 90% investing.” Takes 15 minutes creating concrete emergency fund understanding and action plan impossible when vaguely “should save more” without quantified target and gap assessment.

2. Audit current money allocation identifying savings-investing mismatches requiring rebalancing – List all current money locations with amounts and purposes: Category 1 Checking account: $2,500 (monthly expenses buffer). Category 2 Savings account: $18,500 (purpose assessment needed). Category 3 Investments: $85,000 in 401k + $12,000 in Roth IRA = $97,000 total. Assess each dollar purpose and timeline: Checking $2,500: Appropriate for monthly flow. Savings $18,500: Break down—$14,000 emergency fund (appropriate), $2,500 vacation next year (appropriate short-term), $2,000 “just in case” excess (opportunity cost – should invest). Investments $97,000: All retirement 25+ years away (appropriate long-term). Identify mismatches: Mismatch 1—Excess savings $2,000 beyond emergency fund and defined short-term goals earning 4% should invest at 8% creating $50,000+ opportunity cost over 20 years. Mismatch 2—Retirement money in savings (none identified, good). Mismatch 3—Short-term goal money invested (none identified, good). Create rebalancing plan: Action 1—Transfer excess $2,000 savings to Roth IRA investing in index fund immediately. Action 2—Adjust future allocation: $14,000 emergency fund maintained, short-term goals funded separately as needed, all remaining surplus to investing. Action 3—Set up automatic monthly allocation preventing future drift: $800 investing automatic, $200 flexible for short-term goals as arise. Expected outcome: Eliminate $2,000 excess low-return savings, optimize 80% monthly surplus to investing with 20% flexibility for goals. Write plan: “Current allocation: $18,500 savings (appropriate $16,500, excess $2,000), $97,000 invested (appropriate). Action: Transfer $2,000 to Roth IRA. Future: $800 automatic investing, $200 flexible, maintain $14,000 emergency fund.” Takes 30 minutes identifying money mismatches creating immediate $2,000 optimization plus ongoing balanced allocation impossible when never auditing current status against purpose-based framework.

3. Set up optimal allocation automation matching timeline with vehicle permanently – Create accounts structure: Account 1—Emergency fund high-yield savings (Ally, Marcus, CIT) separate from checking preventing casual spending, name “Emergency ONLY – Do Not Touch.” Account 2—Short-term goals savings (same bank or separate), name “Vacation/Car/Goals 2026-2028.” Account 3—Retirement investing Roth IRA at Vanguard/Fidelity/Schwab in total stock market index fund. Account 4—Taxable brokerage for additional investing beyond retirement limits. Set up automatic monthly allocation from paycheck or checking: Emergency fund: $0 once target reached OR $200-500 monthly if building gap. Short-term goals: $100-300 monthly for defined upcoming needs (vacation, car replacement, wedding, etc.). Retirement investing: $500-1,200 monthly to Roth IRA and/or 401k. Taxable investing: Any remaining surplus after above allocations. Example balanced automation age 35: Income $5,000 monthly minus expenses $3,200 = $1,800 surplus. Allocation: $400 emergency fund (building from $3,000 to $14,000 target over 28 months), $200 short-term goals (annual vacation, car maintenance reserve), $1,200 retirement investing (Roth IRA $583 monthly reaching $7,000 annual limit, 401k $617 monthly), $0 taxable (utilizing all surplus through categories above). Review triggers: Quarterly check emergency fund status adjusting allocation when target reached, annual review short-term goals updating amounts for upcoming year needs, automatic investing continues regardless of market conditions without intervention. Protection mechanisms: Emergency fund in separate bank requiring manual transfer preventing accidental spending, investments in retirement accounts with early withdrawal penalties creating barrier against emotional liquidation, all automations “set and forget” removing decision fatigue and temptation deviation. Write automation summary: “Emergency fund: $400/month Ally savings until $14,800 complete. Short-term: $200/month goals savings. Investing: $1,200/month split $583 Roth IRA + $617 401k. Review: Quarterly emergency fund status, annual goals adjustment. Total automated: $1,800/month (100% surplus optimally allocated).” Takes 60-90 minutes initial setup creating permanent strategic allocation preventing drift through automation impossible when manually deciding each month creating inconsistency and poor timing decisions destroying optimal balanced approach.

These actions create optimal saving-investing foundation within 2-3 hours—calculated specific emergency fund target and gap creating concrete savings priority ($10,600 gap requiring 18 months example), audited current allocation identifying $2,000 excess savings opportunity cost requiring immediate rebalancing, and established automated allocation permanently matching timeline with vehicle preventing future mismatches—transforming from vague “should save and invest” into systematic optimized approach with every dollar purposefully placed impossible when attempting ad-hoc allocation without framework, targets, and automation creating drift toward extreme approaches or inconsistent execution destroying balanced strategy benefits.

Quick FAQ

How much should I keep in savings versus investing?

Keep 3-6 months essential expenses in savings (emergency fund) plus short-term goals under 3 years, invest everything else for long-term wealth building: Emergency fund calculation—Monthly essential expenses (housing, food, transport, insurance, minimum debts) × 3-6 months = emergency fund target. Example: $3,500 essentials × 4 months = $14,000 emergency savings. Short-term goals addition—Specific upcoming needs within 3 years (vacation $3,000, car down payment $5,000, wedding $8,000) = additional $16,000 savings. Total savings target: $30,000 ($14,000 emergency + $16,000 short-term goals). Investment allocation—Everything beyond savings target goes to long-term investing (retirement, education 5+ years away, wealth building). Example complete allocation: $30,000 in savings accounts, $100,000+ in investment accounts, future $1,000 monthly surplus = $200 maintaining/replenishing savings, $800 investing. Age considerations—Ages 20-30: $5,000-15,000 savings typical, ages 30-45: $15,000-30,000 savings, ages 45-60: $20,000-40,000 savings, ages 60+: $25,000-60,000 savings (increased buffer, lower risk tolerance). Common mistake: Keeping $50,000-100,000+ “just in case” in savings creating massive opportunity cost ($50,000 excess over 20 years = $159,000 foregone wealth at 8% versus 2%). Key principle: Adequate emergency fund essential preventing crisis, but beyond reasonable buffer every dollar in savings represents lost investment growth making excess savings expensive false security destroying long-term prosperity.

Should I invest if I don’t have an emergency fund?

Build minimum $1,000 emergency fund before aggressive investing, expand to 3-6 months expenses before maximizing investments, though capture employer 401k match even while building emergency fund: Minimum emergency fund—$1,000 starter fund prevents 70-80% of emergency credit card usage (car repairs, medical, minor home issues), achievable in 1-2 months through intense saving making brief delay acceptable before investment focus. Employer match exception—Always contribute minimum for full 401k match even while building emergency fund (50-100% instant return too valuable to sacrifice), example: employer matches 50% up to 6% salary, contribute 6% for match while building emergency fund with remaining surplus. Balanced approach during building phase—Split surplus 60/40 emergency fund/investing example: $1,000 monthly surplus = $600 emergency fund + $400 investing (401k match), complete $14,000 emergency fund in 24 months while simultaneously accumulating $9,600 invested creating both stability and growth versus extreme all-savings or all-investing. Danger of no emergency fund—Without buffer, $800 car repair forces either high-interest debt or investment liquidation during potential market downturn, example: forced to sell $1,000 investments during 30% crash captures only $700, miss recovery to $1,400 in 3 years = $700 permanent loss from forced timing. Full investment acceleration—After emergency fund complete, redirect entire previous emergency fund contribution to investing dramatically increasing accumulation rate, example: $600 emergency fund contribution becomes $1,000 total investing ($400 existing + $600 freed) doubling investment rate. Timeline: Most complete adequate emergency fund in 6-18 months depending on income and expenses making temporary investment reduction worthwhile preventing crisis liquidation risk.

Can I invest short-term money if I’m comfortable with risk?

Generally NO for true short-term needs under 3 years regardless of risk comfort due to sequence risk creating potential unavailability exactly when needed: Sequence risk problem—Market crashes unpredictable and can occur exactly before planned use, example: invest $20,000 for home down payment needed in 2 years, market crashes 35% month before purchase leaving only $13,000 forcing either abandoning home purchase, significant delay waiting recovery (unknown timeline), or accepting smaller/different home. “Comfortable with risk” misconception—Risk comfort means accepting temporary losses during long investment timeline allowing recovery, NOT accepting failure achieving specific time-bound goal, example: comfortable with portfolio dropping 30% in retirement account age 30 (35 years to recover), NOT comfortable missing home purchase because down payment insufficient. Exceptions for flexibility—If goal truly flexible with 2-5 year window and can delay if market poor, conservative investing acceptable (60/40 or 70/30 stock/bond allocation), example: “want to buy home sometime 2027-2030, whenever market allows” enables investing versus “must buy August 2027 for job relocation” requires savings. Graduated approach—Money needed 4-5 years can use conservative balanced portfolio (50-60% stocks, 40-50% bonds) reducing volatility, shifting to 100% savings final 12-18 months eliminating sequence risk, example: $30,000 home down payment goal 5 years, invest first 3.5 years, shift to savings final 18 months locking in gains. Key principle: Short-term money in stocks creates binary risk (either have full amount or don’t exactly when needed), while long-term investing creates continuous timeline (poor returns one year compensated by good returns other years over decades) making timeline flexibility essential for any investing not emergency-fund money.

What if my emergency fund earns less than inflation?

Accept emergency fund purchasing power erosion as insurance premium for financial stability preventing worse outcomes (debt, investment liquidation) during crisis: Purpose reframe—Emergency fund NOT investment or wealth-building tool, instead insurance creating financial buffer preventing catastrophic decisions during job loss or unexpected expense, modest inflation erosion acceptable cost for protection provided. Real-world benefit—$15,000 emergency fund losing 2% annually to inflation ($300/year purchasing power loss) infinitely preferable to alternatives: (A) No fund forcing $5,000 emergency onto credit card at 18% APR costing $900 annual interest plus stress, (B) Liquidating investments during market crash capturing 30% loss = $1,500 permanent loss plus missed recovery gains worth $3,000+ over subsequent years. Rate optimization within safety—Use high-yield savings (currently 3-5% APY) minimizing inflation gap while maintaining FDIC insurance and liquidity, example: 4% savings versus 2.5% inflation = +1.5% real return current environment (not always available but capture when possible). Appropriate fund size limitation—Keeping exactly 3-6 months expenses not $50,000+ excess minimizes inflation exposure while maintaining adequate protection, example: $18,000 appropriate emergency fund loses $360 annually to 2% real loss versus $50,000 excess losing $1,000 annually making right-sizing critical. Inflation protection portfolio—Long-term invested money at 8% nominal minus 2.5% inflation = 5.5% real return providing purchasing power growth offsetting emergency fund erosion across total portfolio, example: $15,000 emergency fund losing $300 annually acceptable when $200,000 investments gaining $11,000 real annual creating net positive position. Key: Emergency fund sacrifice small guaranteed inflation loss to prevent large uncertain crisis losses making modest erosion acceptable trade-off for essential financial stability buffer enabling investment confidence (knowing won’t need forced liquidation) creating overall superior outcomes despite emergency fund drag.

Should I stop investing during a recession to build more savings?

Generally NO—maintain investing especially during recession buying discounted shares while ensuring emergency fund adequate before recession hits: Counter-intuitive optimal strategy—Recessions create best long-term buying opportunities when stock prices 20-40% discounted making continued investing during downturn critical for superior returns, example: $500 monthly invested during 2008-2009 recession bought shares 40-50% cheaper creating 2-3x returns over subsequent decade versus stopping and missing discounted accumulation. Preparation before recession—Build adequate emergency fund during good times (currently) enabling investment confidence during recession without fear of forced liquidation, example: maintain $18,000 emergency fund through 2026-2027 strong economy, when recession hits 2028 have buffer allowing continued $500 monthly investing despite economic uncertainty and potential job risk. Recession investing benefit—Dollar cost averaging through downturn captures declining prices creating lower average cost basis, example: invest $500 monthly during 18-month recession buying shares at $100 → $80 → $60 → $70 → $90 creating $75 average cost versus $100 pre-recession, when recovery to $120 = 60% gain versus 20% if stopped investing. Emergency fund sufficiency during recession—If fund inadequate (under 3 months), acceptable reducing investment contributions temporarily building 6 months buffer given elevated job loss risk, but resume immediately when adequate never stopping completely. Job security consideration—Stable government or essential industry employment can maintain investing, uncertain industries facing layoffs might pause increasing buffer to 6-12 months during recession then resume. Historical pattern—Every recession (2008, 2020, previous cycles) followed by strong recovery punishing those who stopped investing and rewarding those who continued capturing discounted shares proving recession investing optimal despite discomfort. Key: Recession moment of maximum fear exactly when should invest most aggressively not least, making emergency fund pre-preparation essential enabling recession investing confidence creating superior long-term wealth through temporary discomfort discipline.

Explore More in Investing Basics

Disclosure

This article provides general educational information about saving and investing strategies and allocation approaches. Individual appropriate allocations, emergency fund sizes, investment strategies, and outcomes vary significantly based on personal circumstances including age, income, expenses, family situation, job security, risk tolerance, financial goals, and time horizons. This is not financial advice or personalized recommendation of specific savings/investment ratios, account types, or allocation strategies. Investment return examples represent historical averages with significant year-to-year volatility—actual results vary substantially and past performance does not guarantee future results. Savings account rates fluctuate with Federal Reserve policy and economic conditions—current rates may differ from examples. Emergency fund recommendations represent general guidelines not personalized assessments—appropriate amounts vary based on individual risk factors, family size, job stability, industry, and personal comfort levels. Inflation projections and purchasing power calculations use historical averages—actual inflation varies significantly over time affecting real returns. Timeline-based allocation suggestions (savings for under 3 years, investing for 5+ years) represent general frameworks not absolute rules—individual circumstances may warrant different approaches. Tax implications of savings interest and investment gains vary by individual tax situations and account types. FDIC insurance limits and rules subject to change. Employer 401(k) match percentages and vesting schedules vary by company. Some investment strategies and products not suitable for all investors based on risk tolerance and circumstances. Sinking fund recommendations represent general guidance—specific irregular expense amounts vary widely by individual circumstances and geographic location. Market crash recovery timelines based on historical patterns—future market behavior may differ. Sequence risk (investing short-term money) can result in significant losses affecting ability to achieve time-bound goals. Opportunity cost calculations assume specific return rates—actual investment returns vary. Consult qualified financial advisors, certified financial planners, or investment professionals for personalized guidance matching individual circumstances, risk tolerance, and financial goals before making allocation decisions. Financial success requires sustained discipline, appropriate risk management, and regular strategy review beyond basic knowledge. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.