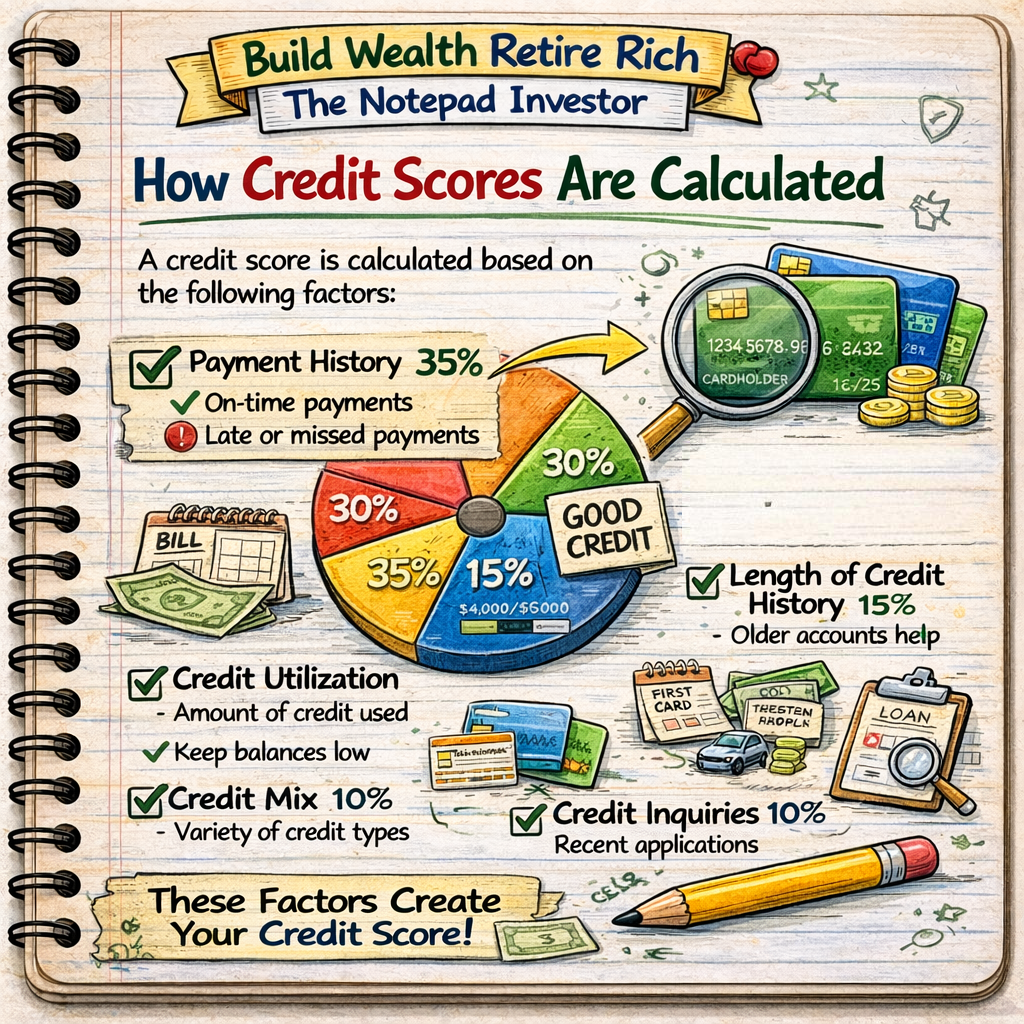

Credit scores are calculated using several factors that reflect how individuals manage their credit. While exact formulas may vary between scoring models, most systems consider similar components.

Payment history is usually the most important factor. This reflects whether individuals pay their bills on time. Consistently making payments by the due date demonstrates reliability and has a positive impact on credit scores.

Credit utilization is another important factor. This measures how much credit a person is using compared to the total credit available. High utilization levels can indicate financial stress and may reduce credit scores.

The length of credit history also plays a role. Lenders generally prefer borrowers with longer credit histories because they provide more information about financial behavior over time.

Credit mix refers to the variety of credit accounts a person holds, such as credit cards, installment loans, and mortgages. A diverse mix of credit types may positively influence a credit score.

Finally, recent credit inquiries are considered. Applying for multiple credit accounts in a short period may signal increased financial risk and can temporarily lower a credit score.

Understanding these factors helps individuals make decisions that improve and maintain strong credit profiles.