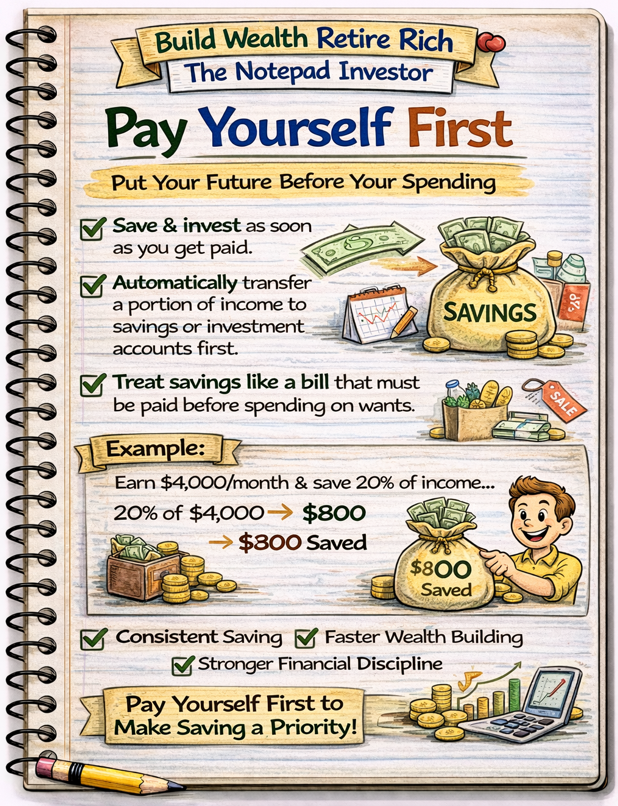

The principle of “pay yourself first” is one of the most effective strategies for building savings. This approach involves setting aside a portion of income for savings immediately when money is received, before paying for other expenses.

Many individuals attempt to save whatever money remains at the end of the month. However, in practice, this often results in little or no savings because most income has already been spent.

By paying yourself first, saving becomes a priority rather than an afterthought. When income is received, a predetermined portion is automatically transferred into a savings or investment account. The remaining income is then used for living expenses.

This strategy works because it establishes saving as a regular financial habit. Over time, individuals adjust their spending patterns to fit within the remaining income.

Automation can make this process even easier. Setting up automatic transfers to savings accounts ensures that the saving habit occurs consistently without requiring ongoing decisions.

The pay-yourself-first strategy transforms saving from something optional into a core part of financial management.