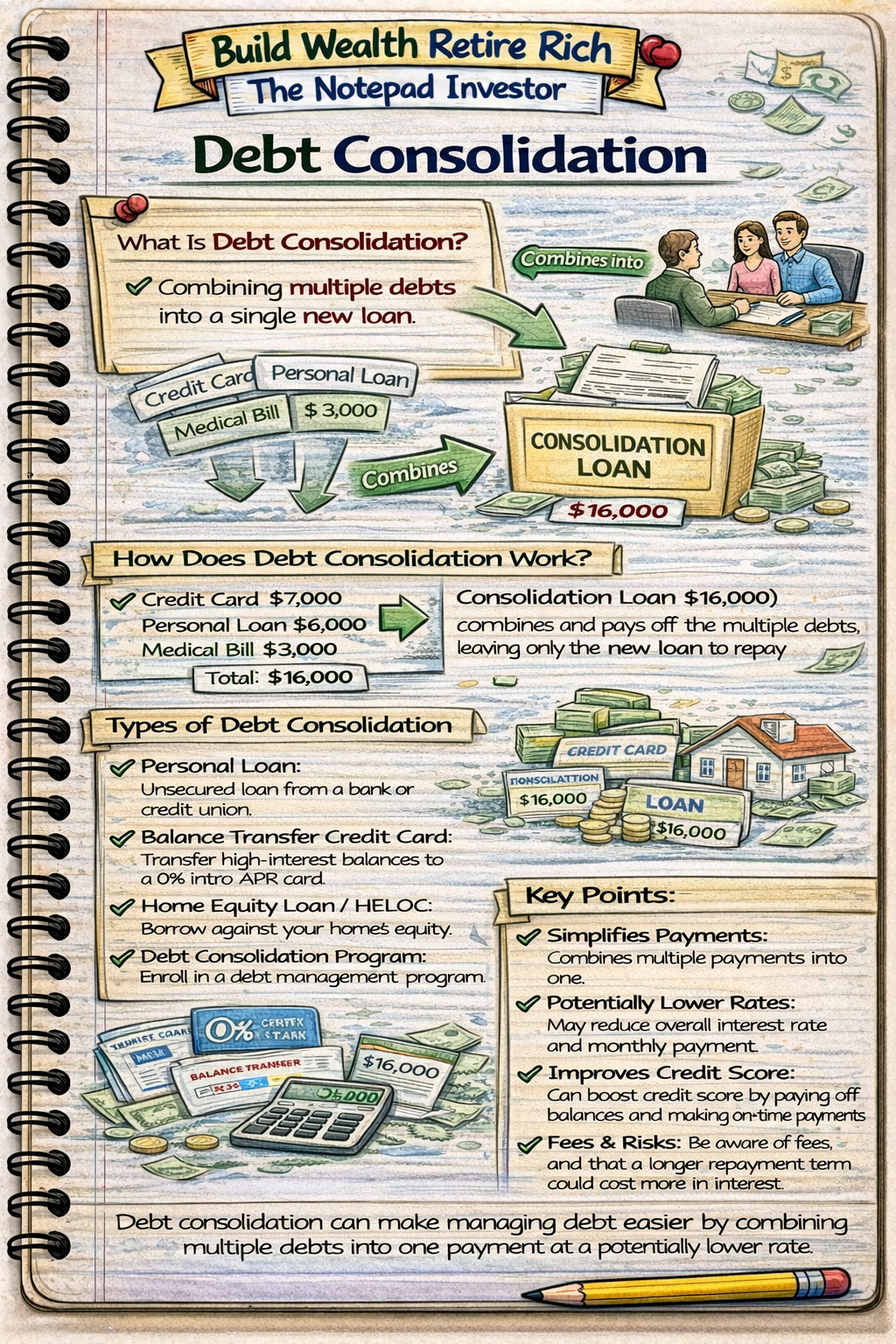

Debt consolidation is debt management strategy combining multiple debts into single loan with unified payment—typically using personal loan, balance transfer credit card, or home equity loan to pay off scattered high-interest obligations, replacing multiple monthly payments and varying interest rates with one streamlined payment at potentially lower rate. While effective when executed strategically saving $3,000-8,000 in interest on typical $15,000-25,000 consolidated debt through rate reduction from 18-24% credit cards to 8-15% consolidation loans, debt consolidation represents solution addressing symptoms not root causes—consolidating without addressing overspending patterns merely creates temporary relief before reaccumulating debt on cleared credit cards creating double burden of consolidation loan plus new credit card balances, making success dependent on behavioral changes preventing future debt cycles not merely mechanical loan replacement. Understanding consolidation mechanics, appropriate use cases, various product types (personal loans, balance transfers, home equity), hidden costs (origination fees, extended terms, restarted interest clocks), and critical success requirements (closing cleared accounts, budget discipline, addressing spending root causes) determines whether consolidation creates pathway to debt freedom saving thousands through simplified repayment or dangerous trap creating larger problems through cleared credit lines tempting renewed spending impossible without comprehensive consolidation literacy recognizing solution limitations alongside legitimate benefits.

This article is designed for anyone considering debt consolidation, individuals overwhelmed by multiple payments and rates wanting simplification, or those evaluating consolidation loan offers from lenders. You do not need financial expertise to understand consolidation—fundamental concept accessible as combining multiple payments into one, though requires honest assessment determining whether multiple debts result from temporary circumstances versus chronic overspending, realistic evaluation of discipline preventing cleared credit card reuse, and comprehensive cost analysis ensuring consolidation actually improves situation not merely shifts debt while adding fees creating worse outcome than maintaining current payments, making consolidation decision requiring behavioral honesty alongside mathematical calculation impossible when viewing as magical debt elimination versus strategic restructuring requiring sustained commitment preventing future accumulation.

Understanding debt consolidation matters because appropriate consolidation saves $3,000-10,000 interest through rate reduction while simplifying payments reducing missed payment risks, inappropriate consolidation costs $5,000-15,000 additional through origination fees and extended terms while creating double-debt trap from cleared account reuse, and strategic selection among consolidation products (personal loan versus balance transfer versus home equity) determines total costs and foreclosure risks—while consolidation-literate individuals use strategic restructuring as component of comprehensive debt elimination plan combining rate reduction with budget discipline and account closure preventing reuse, versus irresponsible consolidators viewing as debt elimination without behavior change perpetuating cycles through cleared account spending creating $30,000+ debt from original $15,000 through successive consolidation-and-reaccumulation rounds impossible to escape without understanding consolidation limitations requiring root cause resolution alongside mechanical loan replacement.

Educational disclaimer: This article provides general educational information about debt consolidation strategies and products. Individual consolidation suitability, rates, terms, and outcomes vary significantly based on circumstances including credit, income, debt types, and lender. This is not financial advice or recommendation of specific consolidation approaches or products. Consolidation carries risks including origination fees, extended repayment terms, home foreclosure risk (if using home equity), and potential debt reaccumulation if spending patterns unchanged. Some debt types ineligible for consolidation. Tax implications vary by product type. Consult qualified financial professionals or credit counselors for personalized guidance matching individual situations.

Debt Consolidation Fundamentals

What Consolidation Is and Isn’t

What consolidation IS:

- Combining multiple debts into single loan with one payment

- Potentially lowering average interest rate through product selection

- Simplifying payment management reducing missed payment risks

- Creating fixed repayment timeline (versus revolving credit perpetuation)

- Strategic debt restructuring as component of elimination plan

What consolidation IS NOT:

- Debt elimination or forgiveness (still owe full amount plus interest)

- Magical solution fixing overspending root causes

- Automatic guarantee of lower rates or payments

- Risk-free—carries costs, risks, and requires discipline

- Substitute for budget discipline and spending behavior change

How Consolidation Works

Basic consolidation process:

Step 1: Inventory all debts

- List every debt with balance, APR, minimum payment

- Calculate total debt amount

- Determine weighted average current APR

- Example: Credit card A $5,000 at 22%, Credit card B $8,000 at 19%, Credit card C $3,000 at 24% = $16,000 total at 20.6% weighted average

Step 2: Obtain consolidation loan

- Apply for personal loan, balance transfer, or home equity product

- Qualify based on credit, income, debt-to-income ratio

- Receive loan proceeds ($16,000 in example)

Step 3: Pay off original debts

- Use loan proceeds to pay all consolidated debts to $0

- Verify zero balances on all paid accounts

- Obtain written confirmation of payoff

Step 4: Make single consolidated payment

- One monthly payment to consolidation lender

- Fixed rate and term (typically 24-60 months)

- Structured repayment timeline versus revolving minimums

Consolidation Benefits When Used Appropriately

Interest rate reduction:

- Replace 18-24% credit cards with 8-15% loan

- Save $2,000-5,000 interest on $15,000 debt over typical term

- Example: $15,000 at 20% over 48 months = $18,200 total versus same at 12% = $16,800 total, saves $1,400

Payment simplification:

- Replace 5 separate payments with 1 unified payment

- Single due date reducing missed payment risk

- Easier budgeting and tracking

- Reduced mental burden from payment juggling

Fixed repayment timeline:

- Defined payoff date (versus perpetual revolving minimums)

- Cannot add new charges to closed-end loan

- Forced structured elimination

- Example: 48-month loan = debt-free in 4 years guaranteed if payments maintained

Potential payment reduction:

- Lower rate plus extended term can reduce monthly payment

- Frees cash flow for emergency fund or other goals

- Warning: Extended terms increase total interest despite lower payments

Types of Debt Consolidation Products

Personal Consolidation Loans

How personal loans work:

- Unsecured installment loan from bank, credit union, or online lender

- Fixed amount, fixed rate, fixed term (24-84 months typical)

- Proceeds deposited to account, borrower pays off debts

- Single monthly payment to lender until fully repaid

Personal loan rates and terms:

- Excellent credit (740+): 8-12% APR typical

- Good credit (670-739): 12-18% APR

- Fair credit (620-669): 18-24% APR

- Poor credit (below 620): 24-36% or denied

- Loan amounts: $1,000-$50,000 typical

- Terms: 24-60 months most common

Personal loan fees:

- Origination fee: 1-8% of loan amount

- Example: $15,000 loan with 5% fee = $750 deducted from proceeds

- Receive $14,250, repay $15,000 plus interest

- Prepayment penalties: Some lenders charge early payoff fees

- Late payment fees: $25-40 typical

Personal loan consolidation example:

- Current debt: $18,000 across 4 cards at 20% average, $540 minimums

- Consolidation: $18,000 personal loan at 12%, 48 months, 5% origination fee

- Fee: $900 (reducing proceeds to $17,100, need $900 from savings to fully pay debts)

- New payment: $474 monthly (lower than $540 minimums)

- Total paid: $22,752 + $900 fee = $23,652

- Original path (minimums): Would pay $35,000+ over 12+ years

- Savings: $11,000+ through consolidation assuming no reuse of cards

Personal loan advantages:

- No collateral required (no foreclosure risk)

- Fixed rate and payment (predictable budgeting)

- Defined payoff timeline

- Often lower rates than credit cards

Personal loan disadvantages:

- Origination fees reduce net savings

- Rates depend heavily on credit score

- Some lenders charge prepayment penalties

- Doesn’t address spending behavior

Balance Transfer Credit Cards

How balance transfers work:

- Transfer existing credit card balances to new card with promotional 0% APR

- Promotional period: 12-21 months typical

- Transfer fee: 3-5% of transferred amount

- After promotion: Reverts to regular APR (15-25% typical)

Balance transfer example:

- Current: $12,000 across 3 cards at 21% average

- Transfer: To 0% card for 18 months with 3% fee

- Fee: $360 (3% of $12,000)

- Payment plan: $12,360 ÷ 18 months = $687 monthly required

- Payoff: Completely eliminated in 18 months

- Total cost: $12,360 ($12,000 + $360 fee)

- Original path: $12,000 at 21% paying $687 monthly = $14,820 total (30 months)

- Savings: $2,460 through balance transfer

Balance transfer advantages:

- 0% APR during promotion (all payments attack principal)

- Massive interest savings if paid during promotion

- No origination fee (just 3-5% transfer fee)

- Can keep original cards open (credit utilization benefit)

Balance transfer disadvantages and risks:

- Must pay off before promotion ends (reverts to 18-25% APR)

- Requires good credit for approval (670+ typically)

- New purchases usually no grace period (accrue interest immediately)

- Payments applied to 0% balance first (new purchases accrue interest)

- Late payment can cancel promotion immediately

- Temptation to use old cards creating double debt

Home Equity Loans and HELOCs

Home equity loan (second mortgage):

- Lump sum loan secured by home equity

- Fixed rate and payment (7-11% typical currently)

- Terms: 10-30 years

- Borrow up to 85% of home equity typically

HELOC (Home Equity Line of Credit):

- Revolving credit line secured by home

- Variable rate (7-11% typical)

- Draw period: 10 years typically

- Repayment period: 10-20 years after draw period

Home equity consolidation example:

- Current debt: $25,000 credit cards at 20% average

- Home equity: $100,000 available (home worth $400,000, mortgage $200,000)

- HELOC: Borrow $25,000 at 8.5% variable

- Pay off all credit cards with HELOC proceeds

- New payment: $300 monthly (10-year repayment)

- Total paid: $36,000 versus $50,000+ on credit cards

- Savings: $14,000+

Home equity advantages:

- Lowest rates available (secured by home)

- Largest amounts available (based on home equity)

- Potential tax deductibility of interest (consult tax professional)

- Extended repayment reducing monthly payment

Home equity CRITICAL RISKS:

- FORECLOSURE RISK: Home is collateral, default = lose house

- Transforms unsecured debt into secured debt risking shelter

- Using home equity for consumption debt extremely risky

- If reaccumulate credit cards, face BOTH home payment AND new debt

- Home value decline creates underwater scenario

- Generally NOT recommended for credit card consolidation

Debt Management Plans (Credit Counseling)

How DMPs work:

- Nonprofit credit counseling agency negotiates with creditors

- Reduced interest rates (often 8-12% versus 18-25%)

- Waived fees and penalties

- Single payment to agency, they distribute to creditors

- Typically 3-5 year programs

DMP requirements:

- Close enrolled credit card accounts

- No new credit while in program

- Monthly counseling fee: $25-50 typical

- Setup fee: $0-50

DMP advantages:

- No loan or credit check required

- Reduced rates through creditor agreements

- Professional support and education

- Enforced discipline (automatic payments)

DMP disadvantages:

- Noted on credit report (not as damaging as default but visible)

- Requires account closures

- Monthly fees add cost

- Not all creditors participate

When Consolidation Makes Sense

Good Consolidation Scenarios

Scenario 1: High-rate debt with good credit

- Situation: $20,000 credit cards at 22% average, credit score 720+

- Solution: Personal loan at 10% or balance transfer at 0%

- Result: Save $4,000-6,000 in interest

- Requirements: Income stable, won’t reuse cards, disciplined repayment

Scenario 2: Overwhelming payment juggling

- Situation: 6+ separate debts, different due dates, missing payments occasionally

- Solution: Consolidation creating single payment date

- Result: Simplified management, avoid late fees and score damage

- Even if rate similar, payment simplification valuable

Scenario 3: Temporary hardship recovery

- Situation: Accumulated debt during job loss/medical crisis, now employed

- Solution: Consolidate at lower rate, structured payoff timeline

- Result: Predictable path to debt freedom, fresh start

- Critical: Hardship resolved, won’t reaccumulate

Scenario 4: Variable rate to fixed rate

- Situation: Mostly credit card debt at variable 18-24% APR

- Solution: Fixed-rate personal loan locking rate

- Result: Protection from rate increases, predictable budgeting

Poor Consolidation Scenarios

Red flag scenario 1: Chronic overspending

- Pattern: Spend more than earn monthly, balances growing continuously

- Danger: Consolidation clears cards enabling more spending

- Likely outcome: $15,000 consolidation loan PLUS $15,000 new cards = $30,000 total debt

- Solution needed: Budget correction first, then maybe consolidation

Red flag scenario 2: Previous consolidation failures

- Pattern: Consolidated before, reaccumulated debt, considering again

- Danger: Behavioral pattern unchanged, will repeat cycle

- Likely outcome: Third consolidation creating $40,000+ from original $10,000

- Solution needed: Professional counseling, root cause resolution

Red flag scenario 3: Using home equity for unsecured debt

- Pattern: $15,000 credit cards, considering HELOC consolidation

- Danger: Transform dischargeable unsecured debt into foreclosure risk

- Likely outcome: Lose home if unable to maintain payments or reaccumulate

- Solution: Personal loan or balance transfer instead, preserve home safety

Red flag scenario 4: High fees negating savings

- Pattern: $8,000 debt at 19%, considering loan at 17% with 8% origination

- Danger: $640 fee plus minimal rate reduction = no real savings

- Calculation: 2% rate improvement offset by 8% upfront cost = worse outcome

- Solution: Aggressive payment on current debt or better consolidation option

Consolidation Decision Framework

Ask these critical questions:

1. Why do I have this debt?

- One-time emergency/hardship: Consolidation may help

- Chronic overspending: Fix behavior first

2. Have I addressed the root cause?

- Budget balanced, spending under income: Proceed

- Still spending more than earning: Don’t consolidate yet

3. Will consolidation actually save money?

- Calculate: Total cost with consolidation versus without

- Include ALL fees, extended term costs, potential reaccumulation

- If saves $2,000+: Worth considering

- If saves under $500: Probably not worth risk/effort

4. Can I avoid reusing cleared accounts?

- Honest assessment: Will close or freeze cards?

- If uncertain: Consolidation premature

5. Do I qualify for beneficial rates?

- Credit 670+: Likely qualify for worthwhile rates

- Credit under 620: Rates may not improve situation

Consolidation Success Requirements

Requirement 1: Close or Freeze Paid-Off Accounts

Critical action after consolidation:

- Close paid-off credit cards OR freeze preventing use

- Remove from wallet and delete saved payment info online

- Only exception: Keep 1-2 oldest cards for credit history (frozen/unused)

Why this matters:

- Prevents double-debt trap (consolidation loan PLUS new card balances)

- Removes temptation during weak moments

- Forces lifestyle adjustment to actual income

Account management strategy:

- Close: Store cards, newest cards, high-fee cards

- Keep frozen: 1-2 oldest cards for credit history length

- Freeze method: Cut up cards, call requesting account freeze, remove from all online merchants

Requirement 2: Budget Discipline and Behavior Change

Essential budget work:

- Track spending revealing where money actually goes

- Identify and eliminate discretionary overspending

- Align monthly spending with monthly income

- Build $1,000 emergency buffer preventing reactive charging

Behavioral changes required:

- Cash/debit only for discretionary spending

- Envelope budgeting for problem categories

- Delay major purchases (30-day rule preventing impulse buying)

- Address emotional spending triggers

Requirement 3: Aggressive Repayment Mindset

Don’t just make minimums on consolidation loan:

- Consolidation creates opportunity, not finish line

- Pay extra when possible accelerating elimination

- Apply windfalls (tax refunds, bonuses) to principal

- Maintain urgency preventing complacency

Repayment acceleration example:

- Consolidation: $18,000 at 12%, 60 months, $400 monthly

- Standard payoff: 60 months, $24,000 total

- Aggressive $600 monthly: 36 months, $21,600 total

- Saves: $2,400 and 24 months through extra payments

Requirement 4: Emergency Fund Priority

Build buffer preventing re-accumulation:

- Save $1,000 starter emergency fund while paying debt

- Prevents reactive charging for car repairs, medical, etc.

- After debt-free, expand to 3-6 months expenses

Emergency fund prevents this scenario:

- Consolidated debt, closed cards, making progress

- $800 car repair needed, no emergency fund

- Forced to reopen credit card or take high-interest loan

- Cycle restarts through lack of buffer

Consolidation Costs and Pitfalls

Hidden Costs to Calculate

Origination fees:

- Personal loans: 1-8% of loan amount

- $20,000 loan with 5% fee = $1,000 cost upfront

- Deducted from proceeds or added to balance

- Reduces net interest savings significantly

Balance transfer fees:

- 3-5% of transferred amount

- $15,000 transfer with 3% fee = $450

- Must be paid off during 0% period to maximize savings

Extended term costs:

- Lower monthly payment through 60-84 month terms

- Dramatically increases total interest despite lower rate

- Example: $18,000 at 12%—36 months = $21,340 total, 72 months = $24,560 total

- Extended term costs $3,220 more despite “affordable” payment

Prepayment penalties:

- Some lenders charge fee for early payoff

- 2-5% of remaining balance typical

- Prevents acceleration, locks borrower into full term

- Avoid lenders with prepayment penalties when possible

The Double-Debt Trap

Most common consolidation failure pattern:

Step 1: Initial consolidation

- Have $15,000 across 4 credit cards

- Take $15,000 personal loan at 12%, pay off all cards

- New payment: $334 monthly for 60 months

Step 2: Cleared cards tempt spending

- Cards show $0 balances, limits restored

- “Can afford small charges” thinking

- Gradual reaccumulation over 12-18 months

Step 3: Double debt crisis

- Still owe $12,000 on consolidation loan (36 months remaining)

- Reaccumulated $8,000 across credit cards

- Total debt: $20,000 (versus original $15,000)

- Payments: $334 loan + $240 card minimums = $574 monthly

- Worse position than before consolidation

Step 4: Desperate second consolidation

- Try consolidating again: $20,000 new loan

- Higher rate (credit damaged): 16% versus original 12%

- Cycle continues if behavior unchanged

Prevention:

- Close or freeze ALL paid-off accounts immediately

- Address spending behavior before consolidating

- Maintain emergency fund preventing reactive charging

Consolidation vs Aggressive Payoff Comparison

Scenario: $18,000 debt at 20% average

Option A: Consolidate to 12% loan, maintain similar payment

- Loan: $18,000 at 12%, 60 months, $400 monthly

- Total paid: $24,000

- Timeline: 60 months

- Risk: Card reuse creating double debt

Option B: Keep current debt, aggressive payments

- Current: $18,000 at 20%, pay $800 monthly (versus $540 minimums)

- Total paid: $21,600

- Timeline: 30 months

- Benefit: Half the time, $2,400 less, no consolidation fees, no reuse risk

Option C: Consolidate AND aggressive payments (best outcome)

- Consolidate to 12%, pay $800 monthly

- Total paid: $19,800

- Timeline: 26 months

- Best: Lowest cost, fastest timeline, rate benefit PLUS aggressive payoff

Key insight: Consolidation alone not optimal—must combine with aggressive payments

Why Understanding Debt Consolidation Matters

Without understanding debt consolidation, individuals either miss legitimate savings opportunities ($3,000-8,000 potential through appropriate rate reduction and strategic selection) or fall into double-debt traps creating $30,000+ from original $15,000 through cleared account reuse, lack framework evaluating when consolidation beneficial versus when aggressive payment on current debt superior avoiding fees and risks, and either avoid beneficial consolidation fearing complexity or pursue inappropriate consolidation without addressing root overspending creating worse outcomes—while consolidation-literate individuals use strategic restructuring as component of comprehensive elimination plan saving thousands through rate optimization while implementing behavioral changes preventing reaccumulation, versus irresponsible consolidators viewing as magical debt elimination perpetuating cycles through cleared card spending creating impossible situations impossible to escape without understanding consolidation represents mechanical restructuring not behavioral solution requiring discipline and root cause resolution alongside loan replacement.

Understanding debt consolidation enables individuals to:

- Calculate true costs including origination fees and extended term impacts

- Evaluate appropriate timing ensuring overspending addressed before consolidating

- Select optimal consolidation product (personal loan vs balance transfer vs DMP)

- Recognize when aggressive current debt payment superior to consolidation

- Implement critical success requirements (account closure, budget discipline, emergency fund)

- Avoid double-debt trap through cleared account management

- Combine consolidation with aggressive repayment maximizing benefits

Debt consolidation knowledge transforms debt management from reactive loan-seeking into strategic informed evaluation weighing benefits against risks, recognizing consolidation as tool not solution requiring behavioral foundation, and preventing common pitfalls creating worse situations through cleared account temptation impossible without comprehensive understanding enabling appropriate strategic use when genuinely beneficial versus recognition when premature or unnecessary.

Common Misunderstandings

Many people view debt consolidation as debt elimination believing consolidated debt somehow disappears or becomes less serious. In reality, consolidation merely restructures existing debt into different format—still owe full original amount plus interest (often more interest through extended terms despite lower rates), making consolidation mechanical reorganization not magical elimination proving debt remains requiring full repayment through sustained discipline regardless of consolidation status not shortcut avoiding payment obligations through loan replacement.

Another common misconception is consolidation always reduces monthly payments and total costs. In practice, consolidation often increases total paid through extended terms and origination fees—$18,000 at 20% paying $540 minimums = $35,000+ total over 12+ years, consolidate to 12% over 72 months = $27,600 total (saves $7,400) BUT aggressive $800 monthly on original debt = $21,600 total in 30 months (saves $5,800 versus consolidation), proving consolidation without aggressive payment creates mediocre outcomes versus optimal combination of rate reduction PLUS payment acceleration or aggressive original debt payment without consolidation fees.

Some believe closing paid-off credit cards after consolidation damages credit scores making account closure inadvisable. However, keeping open zero-balance accounts creates reaccumulation temptation destroying consolidation benefits—credit score temporary 20-30 point dip from closures far preferable to $15,000 reaccumulated debt from open accounts creating $30,000 total burden, proving account closure essential success requirement despite modest score impact making reuse prevention priority over credit score optimization when consolidating demonstrating behavioral protection more valuable than maintaining perfect scores enabling renewed spending.

How Consolidation Understanding Fits Into Financial Success

Debt consolidation understanding enables strategic use of restructuring tools saving $3,000-10,000 interest through appropriate rate reduction when behavioral foundation established, prevents double-debt traps costing $15,000-30,000 through cleared account reuse by recognizing consolidation as component not complete solution, and provides framework distinguishing scenarios where consolidation beneficial versus where aggressive current debt payment superior avoiding unnecessary fees and risks—making consolidation literacy essential component of debt elimination requiring honest behavioral assessment ensuring overspending addressed before consolidating, comprehensive cost calculation including all fees and extended term impacts, and disciplined post-consolidation management through account closure and emergency fund preventing reaccumulation, transforming consolidation from feared complexity or false salvation into understood strategic tool appropriately deployed when genuinely beneficial impossible without recognizing both legitimate optimization opportunities and critical success requirements preventing common failure patterns.

For example, two individuals both age 38 with $22,000 credit card debt at 21% average across 5 cards. Person A hears about consolidation, applies for $22,000 personal loan receiving approval at 14% over 60 months with 6% origination fee ($1,320), pays off all cards with loan proceeds. Month 1-6: Makes $518 monthly loan payment, feels relief from simplified single payment versus 5 previous payments, credit cards show zero balances. Month 7-18: Gradually reuses cards for “emergencies” and conveniences without tracking, accumulates $8,000 across 3 reopened cards. Month 19: Realizes problem, now has $18,500 consolidation loan remaining PLUS $8,000 credit cards = $26,500 total (versus $22,000 original). Payments $518 loan + $240 card minimums = $758 monthly creating financial strain. Age 43 (5 years later): Attempted second consolidation but denied due to debt-to-income ratio, still carrying $15,000 across loan and cards, paid $46,000 total over 5 years ($518 × 60 = $31,080 loan plus $15,000 card payments) yet $15,000 debt remains from perpetual reaccumulation cycle. Person B understands consolidation requirements, first addresses root overspending identifying $400 monthly discretionary cuts, builds $1,000 emergency fund over 3 months, then consolidates $22,000 to balance transfer card 0% for 18 months with 3% fee ($660). Immediately closes 3 newest cards, freezes 2 oldest preventing use. Calculates required payment: $22,660 ÷ 18 = $1,259 monthly required for complete elimination during 0% period. Implements aggressive plan: $400 discretionary cuts + $600 side gig (DoorDash 15 hours weekly) + $300 from previous minimums = $1,300 monthly payment. Month 18: Completely debt-free, paid $23,400 total ($22,000 + $660 fee + $740 remaining interest). Continues $1,300 monthly into investments building wealth. Age 43 (5 years later): Invested $1,300 monthly for 4.5 years (54 months) at 8% return = $93,000 accumulated. Difference: Person A’s consolidation without behavioral change created $15,000 remaining debt plus $46,000 paid with zero wealth = $61,000 hole, Person B’s strategic consolidation with behavior change and aggressive repayment created $93,000 wealth demonstrating $154,000 outcome difference from understanding consolidation as restructuring tool requiring behavioral foundation not magical solution creating superior outcomes through account closure, spending discipline, and aggressive payment impossible without comprehensive consolidation literacy recognizing critical success requirements preventing double-debt trap.

Debt consolidation understanding separates strategic restructurers optimizing rates while maintaining discipline from failed consolidators creating worse situations through behavioral neglect, requiring both mechanical comprehension and honest self-assessment determining readiness creating dramatically different outcomes impossible without consolidation literacy.

Recent Updates and Trends

In recent years, online personal loan marketplaces have proliferated simplifying consolidation product comparison and application, though fundamental evaluation requirements unchanged with borrowers still needing comprehensive cost analysis including origination fees and extended term impacts regardless of application convenience making technology enhancing access not changing strategic decision-making framework determining appropriate consolidation use.

Balance transfer promotional periods have shortened from 18-21 months typical to 12-18 months more common requiring more aggressive monthly payments for complete elimination during 0% window, though strategic value unchanged with borrowers able to capture substantial savings through disciplined payoff before promotion expires making compressed timelines requiring payment discipline not eliminating consolidation benefit when executed properly.

Debt consolidation marketing has intensified with lenders aggressively targeting indebted consumers through digital advertising creating awareness but also potential for inappropriate consolidation by borrowers lacking behavioral readiness, though fundamental consolidation principles unchanged requiring honest overspending assessment before pursuing regardless of marketing convenience or lender encouragement making strategic evaluation essential despite increased product accessibility.

Credit counseling agencies and debt management plans have gained legitimacy through nonprofit certification standards (NFCC, FCAA) improving consumer protection, though DMP enrollment still appears on credit reports creating visibility concerns for some borrowers making alternative consolidation products potentially preferable when qualifying based on credit and income despite DMP legitimate benefits for appropriate candidates.

Fundamental consolidation principles remain timeless: combine multiple debts into single payment potentially reducing rates and simplifying management, requires behavioral changes preventing cleared account reuse, must include comprehensive cost analysis evaluating all fees and extended term impacts, and works best when combined with aggressive repayment not merely minimum payments—regardless of marketplace proliferation, promotional period changes, marketing intensity, or counseling improvements, understanding consolidation as restructuring tool requiring behavioral foundation alongside mechanical loan replacement produces optimal outcomes through strategic appropriate use preventing common pitfalls impossible without comprehensive literacy recognizing both benefits and critical success requirements.

3 Things You Can Do Today

Ready to evaluate debt consolidation strategically? Here are three simple steps you can take right now:

1. Calculate total consolidation costs versus aggressive current debt payment determining if consolidation actually beneficial – List all debts: Balances, APRs, current minimum payments (example: Card A $6,000 at 22%, Card B $8,500 at 19%, Card C $4,200 at 24%, total $18,700 averaging 21.3%). Current path calculation: Use debt calculator entering all debts with total available monthly payment determining timeline and total paid (example: $700 monthly on current debts = 36 months, $25,200 total paid). Consolidation option research: Get actual rates from 2-3 lenders based on credit score, note origination fees, calculate total cost (example: $18,700 loan at 12% over 48 months with 5% fee = $935 fee + $22,100 paid = $23,035 total including fees). Aggressive current payment alternative: Calculate total if simply increase payments on current debt without consolidating (example: $1,000 monthly on current debts = 22 months, $22,000 total, no fees). Compare three scenarios: Current minimums $25,200 over 36 months, Consolidation $23,035 over 48 months (saves $2,165 but 12 months longer), Aggressive current $22,000 over 22 months (best: saves $3,200 versus consolidation, 26 months faster). Consolidation + aggressive option: Calculate consolidation with aggressive payment (example: $18,700 at 12%, pay $1,000 monthly = 20 months, $19,700 total, best outcome if can sustain). Decision framework: If consolidation saves $2,000+ versus current path AND can prevent card reuse through closures = worth considering. If aggressive current payment achieves similar or better outcome = skip consolidation avoiding fees and risks. If cannot sustain aggressive payments making consolidation enabling lower monthly payment while still providing progress = acceptable trade-off. Write comparison: “Current path: $X over Y months. Consolidation: $A over B months (saves/costs $C). Aggressive current: $D over E months (best outcome). Decision: [Consolidate/Aggressive current/Status quo] based on analysis.” Takes 30 minutes creating data-driven decision preventing emotion-based consolidation when inappropriate or missing opportunity when genuinely beneficial.

2. Complete honest behavioral assessment determining if overspending addressed before consolidating preventing double-debt trap – Answer critical questions truthfully: (1) Why do I have this debt? One-time emergency/hardship now resolved OR chronic spending exceeding income ongoing? (2) Review last 6 months spending: Is monthly spending less than monthly income creating surplus OR still spending more than earning each month? (3) Have I created and followed budget for minimum 3 months demonstrating discipline OR still ad-hoc spending without tracking? (4) Can I commit to closing/freezing ALL paid-off credit cards permanently OR need to keep them “just in case” indicating behavioral unreadiness? (5) Have I built $1,000 starter emergency fund preventing reactive charging OR no buffer creating vulnerability to forced card use? (6) Have I previously consolidated debt and reaccumulated OR first consolidation attempt? Score assessment: Answer favorably to 5-6 questions (hardship resolved, budget established, spending under income, willing to close cards, emergency fund built, no previous failures) = READY for consolidation with high success probability, proceed with confidence. Answer favorably to 3-4 questions = MARGINAL readiness, address remaining issues before consolidating or risk moderate reaccumulation probability. Answer favorably to 0-2 questions = NOT READY, consolidation premature creating high reaccumulation risk resulting in double-debt trap, address overspending and build behavioral foundation 6-12 months before reconsidering. Behavioral foundation building if not ready: Create zero-based budget allocating every dollar, track spending 90 days revealing patterns, cut discretionary spending $300-500 monthly, save $1,000 emergency fund, practice 30-day purchase delay rule. Reassess readiness: After 6 months behavioral work, retake assessment determining if consolidation timing improved. Write assessment: “Behavioral readiness: [Ready/Marginal/Not ready]. Issues remaining: [List]. Timeline: [Proceed now/Address issues 3 months/Build foundation 6-12 months].” Takes 20 minutes creating honest evaluation preventing premature consolidation when behavioral foundation absent creating failure probability versus recognizing readiness enabling successful consolidation when foundation established.

3. If consolidating, create account closure and reuse prevention plan executing immediately after payoff – List all accounts being paid off through consolidation: Note which newest (close these), which oldest (potentially keep frozen for credit history). Account closure decisions: Close completely—Store cards, newest cards (under 2 years old), any cards with annual fees not justified by benefits, cards with highest previous balances indicating problem spending. Keep frozen—Maximum 1-2 oldest cards (5+ years old) for credit history length maintenance, must freeze preventing use. Closure execution plan: Day consolidation funds disburse paying cards to zero, call each card being closed requesting permanent account closure, obtain written confirmation of closure within 30 days, verify closures on credit report within 60 days. Freeze execution plan: For cards kept for history, call requesting account freeze or spending block, physically destroy cards cutting into pieces, delete saved card information from all online retailers and subscription services, notify spouse/family members card unavailable preventing authorized user charges. Physical prevention: Remove all credit cards from wallet including frozen ones (keep at home in safe or frozen in ice block creating access friction), delete card details from phone payment apps, unsubscribe from credit card marketing emails preventing reapplication temptation. Alternative payment method: Switch to debit card or cash for all discretionary spending, keep single debit card in wallet, use cash envelope system for problem categories (dining, entertainment, shopping), commit to 90-day credit-free period proving discipline. Emergency backup: If genuinely concerned about emergency access despite building $1,000 fund, keep one frozen card locked in safe with written rule “Use only for expenses over $500 that emergency fund cannot cover, must repay within 30 days” creating accountability. Accountability: Inform spouse/partner/trusted friend of consolidation and closure plan creating external accountability, schedule 30-day check-in reviewing spending and card closure compliance, join debt-free community for ongoing support. Write plan: “Closing: [List cards]. Keeping frozen: [List cards]. Execution date: [When consolidation funds]. Alternative payment: [Debit/Cash/Envelopes]. Emergency protocol: [Plan]. Accountability partner: [Name].” Takes 30 minutes creating systematic reuse prevention impossible without explicit plan executing immediately preventing gradual drift toward card reactivation destroying consolidation benefits.

These actions create strategic consolidation evaluation and success foundation within 90 minutes—calculated comprehensive costs comparing consolidation versus alternatives determining if genuinely beneficial ($2,165 savings example) or if aggressive current payment superior ($3,200 savings alternative), completed honest behavioral readiness assessment preventing premature consolidation when overspending unaddressed (Ready/Marginal/Not ready determination), and created explicit account closure and reuse prevention plan executing immediately protecting consolidation benefits—transforming consolidation from vague debt solution into informed strategic decision with systematic success infrastructure preventing double-debt trap impossible without comprehensive cost analysis, honest self-assessment, and disciplined post-consolidation management.

Quick FAQ

Does debt consolidation hurt my credit score?

Temporary modest impact (10-30 points typical) from hard inquiry and potential account closures, but long-term neutral or positive if managed well: Short-term impacts—Hard inquiry from loan application drops score 5-10 points (recovers within 6 months), closing paid-off accounts reduces available credit increasing utilization potentially dropping score 10-20 points, new loan reduces average account age slightly. Long-term benefits IF managed properly—On-time consolidated loan payments build positive history improving score over time, reduced utilization if keeping some cards open with zero balances helps scores, successful elimination improving debt-to-income ratio benefits future credit applications. Long-term damage IF mismanaged—Missed payments on consolidation loan drop scores 60-110 points, reaccumulating debt on cleared cards dramatically increases utilization destroying scores, defaulting on consolidation loan creates 100-150 point drop plus collections. Net impact example: Start 680 score, consolidate dropping to 660-665 initially (inquiry + closures), after 12 months on-time payments recover to 670-680, after 24 months successful payoff potentially 690-710 from reduced debt and positive history. Comparison: Consolidation score impact minimal versus continuing to struggle with multiple debts missing payments occasionally (each 30-day late = 60-110 point drop), making consolidation score-neutral or beneficial when executed properly versus destructive when mismanaged through missed payments or reaccumulation. Key: Score dip temporary and modest, focus should be debt elimination not score perfection during process, successful consolidation completion produces better long-term scores than perpetual minimum payment struggle.

Should I use a home equity loan to consolidate credit cards?

Generally NO except rare circumstances—transforms dischargeable unsecured debt into foreclosure risk not worth savings: Home equity risks—Lose home if cannot maintain payments (job loss, income reduction, unexpected expenses), reaccumulating credit cards creates BOTH home payment AND new debt potentially forcing foreclosure, underwater home value decline traps borrowers, transforms temporary financial stress into shelter loss. When MAYBE acceptable—Massive debt ($40,000+) where personal loan insufficient, extremely disciplined borrower with proven track record, permanent behavior change demonstrated through 12+ months zero credit card use, substantial home equity buffer ($200,000+) protecting against value decline, stable dual income reducing unemployment risk. Better alternatives—Personal consolidation loan (unsecured, no foreclosure risk), balance transfer credit cards (0% interest if disciplined), debt management plan through credit counseling (negotiated rates without home risk), aggressive payment on current debts avoiding consolidation entirely. Example risk scenario: Consolidate $18,000 cards using HELOC, feel relief from $250 monthly payment versus $540 card minimums, gradually reaccumulate $12,000 on cleared cards over 2 years, now owe $15,000 HELOC (home secured) plus $12,000 cards = $27,000 total, lose job unable to maintain both payments, face foreclosure losing $150,000 home equity over debt problem that started at $18,000. Key principle: Never convert unsecured debt (credit cards dischargeable in bankruptcy as last resort) into secured debt risking primary shelter, modest interest savings ($2,000-4,000 typical) not worth catastrophic foreclosure risk making home equity consolidation inappropriate for consumer debt except extremely rare perfect circumstances with massive debt loads and bulletproof discipline.

How do I avoid reaccumulating debt after consolidation?

Close or freeze ALL paid-off accounts, build emergency fund, address overspending root causes through budget discipline, and maintain aggressive consolidated loan repayment: Account management—Close completely: newest cards, store cards, any high-fee cards, cards associated with problem spending. Freeze preventing use: maximum 1-2 oldest cards kept for credit history (cut up cards physically, call requesting account freeze, delete from online merchants). Remove temptation: eliminate cards from wallet, delete saved payment information everywhere, unsubscribe from credit marketing emails. Emergency fund building—Save $1,000 starter fund ASAP preventing reactive charging for car repairs, medical, appliances, while paying consolidated debt, expand to 3-6 months expenses after debt-free creating comprehensive protection. Budget discipline implementation—Track every dollar spent for 90 days revealing patterns, create zero-based budget allocating all income, cut discretionary spending to necessities only temporarily, use cash envelopes for problem categories (dining, shopping, entertainment), practice 30-day purchase delay rule preventing impulse buying. Overspending root cause resolution—Identify triggers: emotional spending, lifestyle inflation, keeping up with others, lack of financial goals, address through counseling if needed, create meaningful financial goals (debt freedom, home purchase, retirement) providing motivation resisting temptation. Payment momentum maintenance—Pay extra on consolidation loan when possible accelerating elimination, apply windfalls (tax refunds, bonuses) to principal creating progress motivation, celebrate milestones ($5,000 paid, halfway point, final payment) maintaining engagement. Accountability systems—Inform spouse/partner of consolidation and reuse prevention commitment creating external accountability, join debt-free community (online forum, in-person group) sharing progress and struggles, schedule regular financial check-ins (monthly budget reviews, quarterly progress assessments) maintaining vigilance. Reality: 60-70% of consolidators reaccumulate debt within 36 months when not implementing systematic prevention, versus 10-20% reaccumulation when closing accounts, building fund, and maintaining discipline making prevention infrastructure essential not optional for consolidation success.

What’s better: balance transfer or personal loan for consolidation?

Balance transfer if can pay off during 0% promotion (12-21 months) AND good credit (670+) qualifying for approval, personal loan if need longer timeline or moderate credit making transfer difficult: Balance transfer advantages—0% interest during promotion meaning 100% of payments attack principal creating maximum savings, lower fees (3-5% transfer fee versus 3-8% origination), flexible amounts (up to card limits), can keep original cards open benefiting utilization. Balance transfer requirements—Good credit qualifying for approval (670+ typically), discipline paying off before promotion expires (monthly payment = balance ÷ promotional months), no new purchases on transfer card (lose grace period accruing immediate interest), perfect payment record (one late payment can cancel promotion). Balance transfer risks—If not paid during promotion reverts to 18-25% regular APR negating savings, temptation using old cards creating double debt, new purchases on transfer card accrue interest immediately. Personal loan advantages—Fixed rate and term creating predictable timeline (no promotion expiration worry), longer repayment options (24-84 months) reducing payment if needed, available to broader credit range (620+ often qualify), forced discipline through structured installment (cannot add charges). Personal loan disadvantages—Origination fees (3-8%) reducing net benefit, higher interest rates than 0% transfers (8-18% typical), immediate interest accrual from day one. Decision framework—Use balance transfer if: Have $15,000 or less (typical credit limits), can afford aggressive payment during promotion ($12,000 ÷ 18 months = $667 minimum monthly), credit score 670+ qualifying for approval, proven discipline avoiding old card reuse. Use personal loan if: Need longer than 21 months for comfortable payoff, credit below 670 making transfer approval difficult, larger amounts exceeding typical transfer limits ($20,000+), prefer fixed timeline certainty over promotion management. Combination approach: Transfer what qualifies for 0% (up to limits), consolidate remainder with personal loan, creates hybrid capturing both benefits. Example: Have $25,000 total, qualify for $15,000 balance transfer at 0% for 18 months with 3% fee ($450), take $10,000 personal loan at 10% for 36 months, pay $835 transfer + $323 loan = $1,158 monthly eliminating in 18 months (transfer) and 36 months (loan), total cost $15,450 + $11,628 = $27,078 versus $25,000 at 20% over 4 years = $36,000+, saves $8,000+ through strategic combination.

Can I consolidate federal student loans with other debt?

Technically possible but strongly NOT recommended—lose irreplaceable federal protections including income-driven repayment, forgiveness options, and deferment/forbearance: Federal loan protections lost through consolidation—Income-driven repayment plans (SAVE, PAYE, IBR) reducing payments to $0-10% discretionary income if income low, Public Service Loan Forgiveness potentially forgiving $50,000-100,000+ after 120 qualifying payments, deferment and forbearance during unemployment or hardship pausing payments without default, death and disability discharge preventing family liability. What happens when consolidating federal loans into personal loan—Transform federal loans into private debt immediately losing ALL protections permanently, become locked into fixed payment regardless of income changes (no income-driven options), lose forgiveness eligibility costing potential $50,000-100,000+ benefit, no deferment options if unemployment or hardship occurs forcing default risk, consolidation lender can sue and garnish wages without federal program protections. When consolidation MIGHT be acceptable—Have only private student loans (already lack federal protections making consolidation not losing anything), refinancing federal loans separately preserving some protections while lowering rate if credit excellent and income stable. Better approach—Keep federal loans separate using federal consolidation if needed (Direct Consolidation Loan preserving protections), consolidate only credit cards and other consumer debt into personal loan, maintain federal loan protections even if means higher overall interest rate recognizing protection value exceeds rate savings. Example risk: Have $30,000 federal loans at 6% plus $15,000 credit cards at 20%, consolidate ALL into $45,000 loan at 10% over 5 years, lose job unable to maintain $955 monthly payment, no income-driven option available (would have dropped federal payment to $0 under SAVE plan), forced into default destroying credit and facing garnishment, versus keeping separate maintaining federal protections dropping to $0 payment during unemployment while aggressively paying only cards. Key: Federal protections worth more than interest savings in vast majority of circumstances making federal loan consolidation into personal loan major mistake for most borrowers except those certain of permanent stable high income never needing protections (rare certainty).

Explore More in Money Basics

Disclosure

This article provides general educational information about debt consolidation strategies and products. Individual consolidation suitability, rates, terms, fees, and outcomes vary significantly based on circumstances including credit score, income, debt-to-income ratio, debt types, and lender policies. This is not financial advice, endorsement of specific consolidation products or lenders, or guarantee of approval or specific terms. Debt consolidation carries significant risks including origination fees (typically 1-8%), balance transfer fees (3-5%), extended repayment terms potentially increasing total interest paid despite lower rates, home foreclosure risk when using home equity products, potential debt reaccumulation if spending behavior unchanged creating worse financial position than before consolidation. Interest rate and payment examples represent typical scenarios—actual rates vary based on creditworthiness and market conditions. Total cost comparisons assume consistent payments and no reaccumulation—actual results depend on individual discipline and behavior changes. Balance transfer promotional periods vary (12-21 months typical) and require disciplined payoff before expiration to maximize savings. Home equity consolidation particularly risky transforming unsecured dischargeable debt into secured debt risking primary residence foreclosure—generally not recommended for consumer debt consolidation. Federal student loan consolidation into private personal loans eliminates irreplaceable federal protections including income-driven repayment, forgiveness programs, and deferment/forbearance options—strongly discouraged except rare circumstances. Debt management plans through credit counseling appear on credit reports and require account closures. Reaccumulation statistics based on industry observations not controlled scientific studies. Tax implications of different consolidation products vary—interest deductibility depends on product type and individual tax situation requiring professional tax advice. Some debt types may not be eligible for consolidation depending on lender policies. Consult qualified financial professionals, credit counselors (NFCC.org member agencies), or debt advisors for personalized guidance matching individual circumstances, debt compositions, and behavioral readiness. Focus on addressing root spending causes alongside mechanical consolidation preventing future cycles. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.