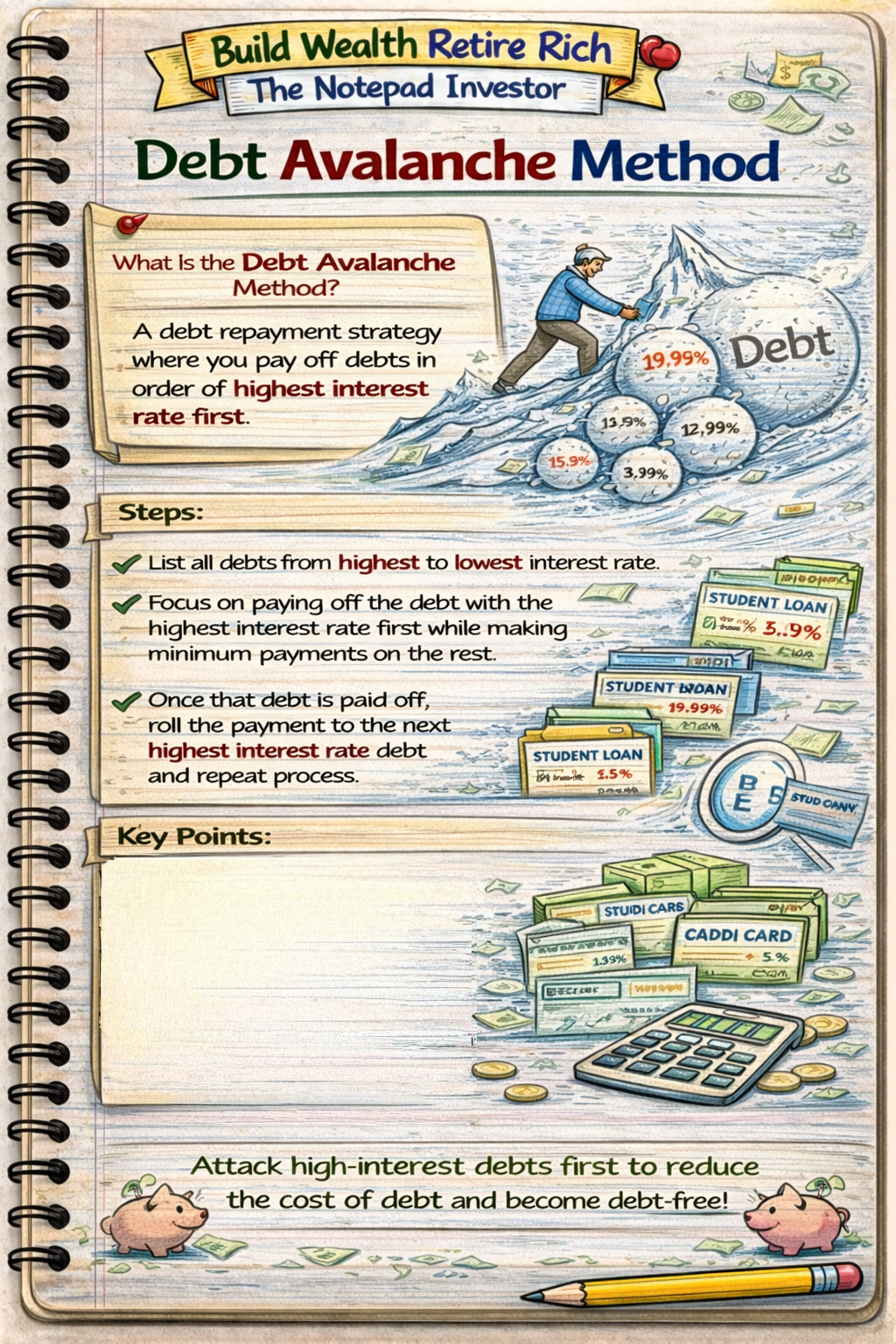

Debt avalanche method is mathematically-optimal debt elimination strategy prioritizing interest cost minimization by attacking highest APR debt first regardless of balance size—paying minimums on all debts except highest interest rate, applying all extra payment to highest APR debt, then rolling entire payment to next highest rate when first debt eliminated, minimizing total interest paid through mathematical optimization saving $500-2,000 typical versus debt snowball (smallest-first) approach on $15,000-20,000 total debt. While requiring greater discipline and delayed gratification—first victory potentially 8-15 months versus snowball’s 3-6 months—avalanche method produces superior outcomes for number-focused individuals motivated by optimization and comfortable with extended timeline before tangible progress, making avalanche ideal for financially-disciplined borrowers prioritizing total cost reduction over psychological wins, though requiring sustained commitment without early celebration milestones creating 60-70% completion rate versus snowball’s 80%+ due to discouragement risk from delayed first victory. Understanding when avalanche superior versus when snowball’s behavioral advantages outweigh mathematical savings enables informed method selection optimizing individual personality fit—disciplined analytical personalities thrive with avalanche saving maximum interest while psychology-driven individuals achieve better outcomes accepting snowball’s modest premium ensuring execution, demonstrating debt elimination success requires matching strategy to personality not universal method superiority declarations.

This article is designed for mathematically-inclined individuals wanting optimal debt elimination strategy, high-discipline borrowers comfortable delayed gratification, or anyone evaluating avalanche versus snowball methods. You do not need advanced math expertise to understand avalanche—basic interest calculation and ranking by APR accessible to anyone, though requires honest self-assessment recognizing whether motivated by mathematical optimization or psychological wins, disciplined commitment maintaining aggressive payments 12-24+ months without early victories, and realistic personality evaluation determining if capable sustaining motivation through extended timeline before first tangible progress milestone preventing discouragement-driven abandonment destroying optimization benefits through perpetual debt continuation.

Understanding debt avalanche method matters because mathematical optimization saves $500-2,000 interest on typical debt loads through highest-APR-first approach versus random or balance-based methods, 2-4 month faster total elimination timeline through efficient interest minimization creates quicker overall freedom, and strategic approach optimal for specific personality types maximizing outcomes when matched appropriately—while avalanche-method users save maximum interest completing elimination 2-4 months faster than snowball when sustained through completion, versus abandoners perpetuating debt indefinitely through discouragement costing $10,000+ in continued interest when delayed first victory (12+ months typical) causes motivation collapse, proving avalanche produces superior outcomes for disciplined analytical individuals while creating inferior results for psychology-driven majority requiring quick wins impossible without honest personality assessment enabling appropriate method selection optimizing completion probability over theoretical superiority.

Educational disclaimer: This article provides general educational information about debt avalanche method. Individual debt situations, appropriate strategies, payoff timelines, and interest savings vary based on circumstances including total debt, income, expenses, interest rate composition, and individual discipline. This is not financial advice or recommendation that debt avalanche method optimal for all situations. Debt elimination requires sustained commitment regardless of method. Some individuals may achieve better outcomes with debt snowball or hybrid approaches based on psychological factors. Consult qualified financial professionals or credit counselors for personalized guidance matching individual circumstances and personality profiles.

Avalanche Method Fundamentals

How Avalanche Method Works

Core principles:

- List all debts from highest to lowest APR

- Ignore balance amounts completely in ranking

- Pay minimum payments on all debts except highest APR

- Apply all extra available payment to highest APR debt

- When highest APR eliminated, roll entire payment to next highest APR

- Repeat until all debts eliminated

- Minimizes total interest paid mathematically

Step-by-step implementation:

Step 1: List all debts highest to lowest APR

- Credit card B: $5,000 at 24% APR, $150 minimum

- Store card: $800 at 22% APR, $25 minimum

- Credit card A: $2,500 at 18% APR, $75 minimum

- Auto loan: $8,000 at 6% APR, $250 minimum

- Student loan: $15,000 at 5% APR, $180 minimum

Step 2: Calculate total available monthly payment

- Required minimums: $680 total

- Extra from budget: $320

- Total available: $1,000 monthly

Step 3: Allocate payments using avalanche ranking

- Credit card B: $150 minimum + $320 extra = $470 total (attack highest APR)

- Store card: $25 minimum only

- Credit card A: $75 minimum only

- Auto loan: $250 minimum only

- Student loan: $180 minimum only

Step 4: Eliminate first debt and roll payment

- Credit card B: Paid off in 12 months ($470 × 12 = $5,640 covers balance + interest)

- Roll $470 to Store card (next highest APR) creating $495 monthly payment ($25 + $470)

- Continue minimums on remaining debts

Step 5: Continue avalanche through all debts by APR

- Store card: Paid in additional 2 months with $495 monthly

- Roll $495 to Credit card A creating $570 monthly ($75 + $495)

- Credit card A: Paid in additional 5 months

- Roll $570 to Auto loan creating $820 monthly

- Auto loan: Paid in additional 10 months

- Roll $820 to Student loan creating $1,000 monthly

- Student loan: Paid in additional 15 months

- Total timeline: 44 months completely debt-free

Why It’s Called “Avalanche”

Avalanche metaphor:

- Like snow avalanche gaining momentum downhill

- Initial progress slow (attacking large balance at high rate)

- Acceleration builds as highest-cost debts eliminated

- Momentum compounds saving more interest each month

- Final debts fall rapidly despite larger balances through massive payments and low rates

Mathematical Superiority Principle

Why avalanche saves most interest:

- Every dollar of principal reduction on 24% debt saves $0.24 annually

- Same dollar on 6% debt saves only $0.06 annually

- Attacking highest rates first maximizes per-dollar interest savings

- Compound effect over months/years creates substantial total savings

Interest savings example:

- $1,000 extra payment to 24% debt: Saves $240 annually in future interest

- Same $1,000 to 6% debt: Saves $60 annually in future interest

- Avalanche optimizes every payment maximizing interest reduction

Avalanche vs Snowball Detailed Comparison

Same Debt Load Both Methods

Starting scenario:

- Total debt: $31,300 across 5 debts

- Available payment: $1,000 monthly

- Debts: Credit card B $5,000 at 24%, Store card $800 at 22%, Credit card A $2,500 at 18%, Auto $8,000 at 6%, Student $15,000 at 5%

AVALANCHE Results (Highest APR First)

Attack sequence by APR:

- 1st: Credit card B $5,000 at 24%

- 2nd: Store card $800 at 22%

- 3rd: Credit card A $2,500 at 18%

- 4th: Auto loan $8,000 at 6%

- 5th: Student loan $15,000 at 5%

Victory timeline:

- Month 12: Credit card B eliminated (first victory after 1 year)

- Month 14: Store card eliminated

- Month 19: Credit card A eliminated

- Month 29: Auto loan eliminated

- Month 44: Student loan eliminated (DEBT FREE)

Financial results:

- Total paid: $32,100

- Total interest: $800

- Timeline: 44 months (3 years 8 months)

SNOWBALL Results (Smallest Balance First)

Attack sequence by balance:

- 1st: Store card $800

- 2nd: Credit card A $2,500

- 3rd: Credit card B $5,000

- 4th: Auto loan $8,000

- 5th: Student loan $15,000

Victory timeline:

- Month 3: Store card eliminated (first victory after 3 months)

- Month 10: Credit card A eliminated

- Month 20: Credit card B eliminated

- Month 30: Auto loan eliminated

- Month 46: Student loan eliminated (DEBT FREE)

Financial results:

- Total paid: $32,850

- Total interest: $1,550

- Timeline: 46 months (3 years 10 months)

Method Comparison Summary

AVALANCHE ADVANTAGES:

- Interest savings: $750 less paid ($800 vs $1,550)

- Time savings: 2 months faster (44 vs 46 months)

- Mathematical optimization: Every payment maximally efficient

- Percentage savings: 2.3% lower total cost

SNOWBALL ADVANTAGES:

- First victory: Month 3 vs Month 12 (9 months earlier)

- Victories year 1: 2 debts eliminated vs 0

- Psychological momentum: Regular celebration milestones

- Completion rate: 80%+ vs 60-70% (behavioral research)

Key insight:

- $750 avalanche savings represents excellent value IF completed

- Snowball’s $750 premium represents insurance against abandonment

- Abandoned avalanche costs $10,000+ in perpetual interest

- Completed snowball outperforms abandoned avalanche dramatically

When Interest Savings Become Significant

Large savings scenarios (avalanche clearly superior):

Extreme rate gaps:

- $8,000 at 29% APR vs $1,000 at 4% APR

- Avalanche attacks 29% saving $2,320 annually in interest reduction

- Snowball attacks $1,000 saving $40 annually

- Gap: $2,280 annual difference making avalanche clearly superior

High total debt with rate variation:

- $50,000+ total debt across 10+ accounts

- Rates ranging 8-26%

- Avalanche savings: $2,000-5,000 versus snowball

- Significant dollar amounts justifying mathematical approach

Minimal savings scenarios (snowball acceptable):

Similar interest rates:

- All debts 15-20% APR range

- Avalanche savings: $200-400 total

- Psychological benefit of snowball outweighs minimal cost

Small total debt:

- Under $10,000 total across 3-4 accounts

- Avalanche savings: $100-300

- Quick elimination either method (12-18 months)

- Method choice less critical with short timeline

Implementing Avalanche Method Successfully

Step 1: Accurate Interest Rate Inventory

Gathering APR information:

- Check recent statements for each debt

- Call creditors if APR unclear or variable

- Note promotional rates and expiration dates

- Calculate weighted average if multiple APRs on one account

APR precision importance:

- 22.99% vs 23.24% APR = different attack priorities

- Small rate differences matter in avalanche ranking

- Variable rates: Use current rate for ranking, re-evaluate quarterly

Organization example:

- Credit card A: 24.99% APR, $4,500 balance

- Credit card B: 21.24% APR, $2,800 balance

- Credit card C: 18.99% APR, $6,200 balance

- Auto loan: 7.5% APR, $12,000 balance

- Student loan: 5.8% APR, $18,000 balance

Step 2: Calculate Maximum Payment Capacity

Finding aggressive payment amount:

- List all minimum payments

- Identify discretionary cuts (aggressive approach)

- Add side income opportunities

- Maximize total available for debt elimination

Example capacity building:

- Minimums required: $850

- Discretionary cuts: $400 (dining, entertainment, subscriptions)

- Side income: $500 (freelance work 10 hours weekly)

- Total capacity: $1,750 monthly (106% increase over minimums)

Step 3: Maintain Discipline Through Extended Timeline

Avalanche-specific challenges:

- First victory often 8-15 months (versus snowball’s 3-6)

- Requires intrinsic motivation without external victories

- Large balance at high rate creates slow visible progress

- Temptation to switch methods when discouraged

Discipline maintenance strategies:

1. Interest savings tracking:

- Calculate monthly interest saved versus minimum payments

- Running total of interest avoided through aggressive payments

- Example: “Saved $185 interest this month, $1,840 total saved so far”

- Provides tangible progress metric without account elimination

2. Balance reduction milestones:

- Celebrate $1,000 increments on attack debt

- Example: $5,000 → $4,000 → $3,000 mini-celebrations

- Visual progress bars showing percentage paid

3. Mathematical focus reinforcement:

- Monthly calculation of avalanche vs snowball comparison

- “On track to save $850 versus snowball” validation

- Spreadsheet showing projected final savings

4. Commitment devices:

- Public declaration (accountability community)

- Automated payments preventing reduction temptation

- Written commitment reviewing reasons for avalanche choice

Step 4: Optimize with Balance Transfers

Avalanche-transfer combination:

- Transfer highest APR debts to 0% promotional cards

- Eliminates interest on attack debt during payoff

- Dramatically increases savings versus standard avalanche

Example optimization:

- Credit card $6,000 at 24% (attack debt)

- Transfer to 0% for 18 months with 3% fee ($180)

- Pay $400 monthly eliminating in 15 months

- Interest saved: $1,100+ versus no transfer

- Total cost: $6,180 vs $7,300+ standard avalanche

Who Should Choose Avalanche Method

Ideal Avalanche Candidates

Personality characteristics:

- Mathematically-oriented: Motivated by numbers, optimization, efficiency

- High discipline: Sustains commitment without external validation

- Delayed gratification: Comfortable waiting 12+ months for first victory

- Analytical decision-maker: Prioritizes logic over emotion

- Intrinsically motivated: Doesn’t require celebration milestones

Debt composition favoring avalanche:

- Extreme rate gaps (24%+ versus 5% creating $1,500+ savings)

- High total debt ($30,000+) where savings substantial ($2,000+)

- Few accounts (3-4 debts total creating manageable timeline)

- Large high-rate balances where avalanche attack makes mathematical sense

Successful avalanche profile example:

- Engineer or accountant (number-focused profession)

- History of completing long-term goals (marathon training, advanced degree)

- Spreadsheet enthusiast tracking finances meticulously

- Motivated by optimization and efficiency

- Comfortable with gradual progress toward distant goals

Poor Avalanche Candidates

Personality red flags:

- Previous debt elimination attempts failed

- Need frequent validation and celebration

- Emotionally-driven decision-making

- Impulsive or easily discouraged

- Difficulty sustaining motivation without tangible wins

Better snowball indicators:

- Multiple small balances under $2,000 (enables quick snowball wins)

- Similar interest rates across debts (minimal avalanche savings)

- Need for psychological momentum

- Spousal disagreement (snowball creates visible progress reducing conflict)

Self-Assessment Questions

Choose AVALANCHE if answering “yes” to most:

- Am I motivated primarily by numbers and optimization?

- Can I sustain 12+ months effort without tangible victories?

- Do I track finances meticulously in spreadsheets?

- Have I successfully completed other long-term goals requiring delayed gratification?

- Are my interest rate gaps extreme (20%+ differential)?

- Is my total debt over $25,000 where savings substantial?

- Do I make decisions based on logic rather than emotion?

Choose SNOWBALL if answering “yes” to most:

- Have previous debt payoff attempts failed from discouragement?

- Do I need frequent wins to maintain motivation?

- Do I have multiple small balances under $2,000?

- Am I emotionally-driven in financial decisions?

- Are my interest rates relatively similar (15-22% range)?

- Is total debt under $15,000 where method difference minimal?

- Do I value psychological progress over mathematical optimization?

Hybrid Approaches

Modified Avalanche-Snowball

Quick-win avalanche:

- Attack smallest balance first (regardless of rate) for immediate victory

- Switch to avalanche for remaining debts

- Captures psychological boost plus mathematical efficiency

Example implementation:

- Debts: $800 at 15%, $3,000 at 22%, $5,000 at 24%, $8,000 at 6%

- Snowball first: Attack $800 (2-3 month victory)

- Then avalanche: Attack 24%, then 22%, then 6%

- Cost: $50-100 extra interest for quick win

- Benefit: Motivation boost plus 95% of avalanche savings

Rate-Threshold Avalanche

Attack high rates only:

- Avalanche all debts over 12% APR

- Switch to snowball for remaining low-rate debts

- Maximizes interest savings on expensive debt

- Provides psychological wins on final stretch

Example:

- High-rate group: $4,000 at 24%, $3,000 at 20%, $2,500 at 18%

- Avalanche these first (24% → 20% → 18%)

- Low-rate group: $8,000 at 7%, $6,000 at 5%

- Snowball these second ($6,000 → $8,000 for quick final victory)

Balance-Modified Avalanche

Avalanche with balance consideration:

- Attack highest APR as standard avalanche

- Exception: If rate within 2% and balance 5x smaller, attack small one first

- Provides flexibility for near-ties

Example decision:

- Option A: $6,000 at 21% APR

- Option B: $1,000 at 19% APR

- Rate difference: 2% (minimal)

- Balance ratio: 6:1

- Decision: Attack $1,000 first (3-month victory worth 2% rate difference)

- Then attack $6,000 at 21%

Why Understanding Debt Avalanche Method Matters

Without understanding debt avalanche method, individuals miss mathematical optimization opportunity saving $500-2,000 interest through highest-APR-first approach versus random payments or balance-focused methods, lack framework for informed method selection comparing avalanche and snowball based on personality fit and debt composition, and either choose suboptimal method wasting interest dollars when disciplined enough for avalanche or attempt avalanche without appropriate temperament leading to abandonment—while avalanche-method users maximize interest savings completing elimination 2-4 months faster through mathematical efficiency when personality compatible and commitment sustained, versus inappropriate avalanche attempts by psychology-driven individuals resulting in abandonment perpetuating debt costing $10,000+ through motivation collapse from delayed first victory, demonstrating critical importance of method-personality matching not universal superiority claims making avalanche understanding essential for informed strategic selection optimizing individual outcomes.

Understanding debt avalanche method enables individuals to:

- Evaluate mathematical optimization potential calculating interest savings versus snowball

- Assess personality fit recognizing whether discipline sufficient for delayed gratification

- Implement highest-APR-first systematically when appropriate maximizing efficiency

- Combine with balance transfers optimizing interest elimination on attack debt

- Make informed method choice weighing $500-1,000 savings against psychological factors

- Consider hybrid approaches capturing optimization benefits with psychological wins

- Maintain commitment through extended timeline using interest-savings tracking

Debt avalanche knowledge transforms method selection from random choice or dogmatic adherence into informed personality-based optimization weighing mathematical efficiency against psychological momentum, enabling maximum interest savings when individual temperament compatible with delayed gratification versus recognizing when snowball’s behavioral advantages outweigh modest avalanche premium impossible without understanding both method mechanics and honest self-assessment determining appropriate strategic fit.

Common Misunderstandings

Many people assume debt avalanche always superior because it minimizes interest mathematically. In reality, abandoned avalanche produces worse outcomes than completed snowball—$750 theoretical savings becoming $0 when method abandoned after 6 months perpetuating $15,000 debt costing $10,000+ in continued interest over subsequent years, versus snowball’s $750 premium ensuring completion through quick wins creating total interest cost $1,550 versus perpetual debt scenario’s $10,000+, proving mathematical superiority irrelevant without completion making execution probability more important than theoretical optimization for majority requiring psychological momentum impossible through interest-rate-only focus.

Another common misconception is avalanche dramatically more complex than snowball requiring advanced mathematical skills. In practice, avalanche simply ranks debts by APR instead of balance—anyone capable listing debts smallest-to-largest for snowball equally capable listing highest-to-lowest APR for avalanche with identical execution mechanics thereafter (minimums on all except attack debt, roll payments when eliminated), making complexity difference zero while personality fit for delayed gratification creates actual differentiation not mathematical difficulty proving avalanche accessibility identical to snowball despite perception of increased complexity.

Some believe small interest rate differences insignificant making avalanche unnecessary perfectionism. However, attacking 24% debt versus 18% debt with $300 monthly creates $18 monthly interest differential accumulating to $500-800 over typical 24-30 month elimination period, making rate optimization worthwhile even for modest differentials when completion assured, though correctly observing that 18% versus 16% differences create minimal savings ($6 monthly = $150-200 total) where snowball’s psychological advantages likely outweigh mathematical premium demonstrating importance of evaluating rate gaps determining when avalanche optimization worthwhile versus when snowball acceptable.

How Avalanche Understanding Fits Into Financial Success

Debt avalanche understanding enables informed method selection optimizing mathematical efficiency when personality compatible with delayed gratification saving $500-2,000 interest versus alternative approaches, prevents inappropriate avalanche attempts by psychology-driven individuals requiring quick wins avoiding abandonment costing $10,000+ through motivation collapse, and provides framework evaluating rate gaps determining when optimization worthwhile versus when minimal savings make snowball acceptable—making avalanche literacy essential component of strategic debt elimination requiring honest self-assessment matching method to temperament, realistic evaluation of rate composition determining savings potential, and disciplined commitment sustaining motivation through 12-24 month timeline without early celebration milestones, transforming debt elimination from one-size-fits-all approach into personalized optimization maximizing individual outcomes through appropriate method selection impossible without understanding both avalanche mechanics and personality fit requirements.

For example, two engineers both age 35 both carrying $22,000 debt across 5 accounts with identical APR composition and $900 monthly payment capacity. Engineer A reads about snowball method’s psychological benefits, implements smallest-first approach despite analytical personality. Month 1-3: Attacks $1,200 smallest balance, eliminates successfully creating quick win. Month 4-8: Attacks $2,800 second balance, eliminates month 8. However, feels frustrated watching $6,000 at 26% APR accrue $130 monthly interest while attacking $2,800 at 17% APR accruing only $40 monthly, recognizes inefficiency bothers analytical mind. Month 9-12: Conflicted between continuing snowball versus switching to avalanche, decision paralysis reduces motivation. Month 13-18: Reduces payment from $900 to $600 “temporarily” due to motivational lapse from method misalignment. After 18 months: Paid $13,500 but remaining debt $13,200 (minimal progress last 6 months), feels defeated by slower-than-expected progress. After 36 months: Finally completes elimination having reduced payments multiple times, total paid $23,800 ($22,000 principal + $1,800 interest). Engineer B understands both methods, recognizes analytical personality compatible with avalanche approach, implements highest-APR-first systematically. Month 1-12: Attacks $6,000 at 26% APR with $900 monthly, balance decreases visibly each month ($6,000 → $5,300 → $4,550 → $3,750…), tracks interest saved versus minimum payments ($156 first month → $2,100 cumulative after 12 months), eliminates month 12. Celebrates with $50 dinner recognizing first milestone. Month 13-16: Attacks $3,500 at 23% APR, eliminates month 16. Month 17-22: Attacks $4,500 at 19% APR, eliminates month 22. Month 23-27: Attacks $5,200 at 7% APR, eliminates month 27. Month 28-30: Attacks final $2,800 at 6% APR, completely debt-free month 30. Total paid: $22,650 ($22,000 + $650 interest). Immediately redirects $900 monthly to investments. Difference: Engineer A’s snowball approach despite analytical personality created motivation misalignment causing payment reductions extending timeline to 36 months costing $23,800 ($1,800 interest) despite method designed for psychological wins not matching individual temperament, Engineer B’s avalanche approach matching analytical personality maintained consistent $900 monthly through interest-savings motivation completing 30 months paying $22,650 ($650 interest) demonstrating $1,150 savings ($1,800 – $650 = $1,150 interest difference) plus 6-month faster timeline from appropriate method-personality matching impossible without avalanche understanding enabling self-assessment determining strategic fit creating superior outcomes through personalized optimization versus dogmatic adherence to single approach.

Debt avalanche understanding separates strategically-optimized eliminators matching method to personality from misaligned method users either wasting interest through incompatible snowball choice when discipline sufficient for avalanche or attempting avalanche without appropriate temperament leading to abandonment, requiring both method mechanics comprehension and honest self-assessment enabling informed strategic selection producing measurable outcome differences impossible without avalanche literacy.

Recent Updates and Trends

In recent years, online debt calculators have proliferated enabling instant avalanche-versus-snowball comparison showing exact interest savings and timeline differences, though fundamental method mechanics unchanged with highest-APR-first approach remaining mathematically optimal regardless of technological tools simplifying comparison analysis making calculator availability enhancing decision-making not altering underlying strategic principles.

Debt elimination community debates between avalanche and snowball advocates have intensified creating tribal method loyalty, though individual personality fit more important than universal method superiority with both approaches producing successful outcomes when matched appropriately to borrower temperament making debate somewhat counterproductive when framed as absolute superiority rather than personality-based optimization selection.

Financial advisors increasingly recognize behavioral finance importance acknowledging that mathematically-optimal strategies fail when abandoned, though some remain avalanche purists dismissing snowball’s $500-1,000 premium as wasteful despite completion probability evidence suggesting executed snowball outperforms abandoned avalanche making execution-focused approaches practically superior for psychology-driven majority requiring celebration milestones.

Hybrid method adoption has grown as borrowers recognize pure avalanche or snowball less optimal than customized approaches combining quick wins with mathematical efficiency, though consistency within chosen framework remains more important than constant optimization attempts creating decision fatigue and reduced execution quality demonstrating value of initial informed selection over perpetual method switching.

Fundamental avalanche principles remain timeless: highest-APR-first minimizes total interest mathematically, requires discipline sustaining commitment without early victories, produces superior outcomes for analytical personalities comfortable delayed gratification, and should be evaluated against snowball considering both interest savings magnitude and individual psychological factors—regardless of calculator proliferation, community debate intensity, advisor acknowledgment changes, or hybrid approach popularity, understanding highest-APR-first mechanics, calculating interest savings potential, and honestly assessing personality fit produces optimal method selection maximizing individual outcomes through appropriate strategic matching impossible without avalanche literacy enabling informed comparison-based decision-making.

3 Things You Can Do Today

Ready to evaluate debt avalanche approach? Here are three simple steps you can take right now:

1. Calculate exact interest savings comparing avalanche versus snowball on your specific debt revealing whether optimization worthwhile – List all debts with balances and APRs: Example—Credit card A $3,500 at 24%, Credit card B $5,200 at 19%, Auto loan $8,500 at 7%, Student loan $12,000 at 5%. Use online debt calculator (undebt.it, creditkarma debt calculator) entering all debts with available monthly payment amount. Run AVALANCHE calculation: Highest APR first, record total paid, total interest, timeline (example result: $29,800 total, $600 interest, 32 months). Run SNOWBALL calculation: Smallest balance first, record total paid, total interest, timeline (example result: $30,350 total, $1,150 interest, 34 months). Compare results: Calculate savings (example: $550 interest savings, 2 months faster with avalanche = $550 ÷ $29,200 total debt = 1.9% cost difference). Evaluate significance: If savings $500+ and 2+ months faster = avalanche worthwhile if disciplined. If savings under $300 and similar timeline = snowball acceptable accepting minor premium for psychological benefits. Consider rate gaps: If extreme gaps (24% versus 5% = 19% differential) avalanche clearly superior mathematically. If modest gaps (all debts 15-20% range) savings minimal making snowball acceptable. Write comparison: “Avalanche: $X total, Y months. Snowball: $A total, B months. Difference: $C savings (D%), E months faster.” Decision framework: Savings over $1,000 or 10%+ cost difference = avalanche strongly recommended if capable. Savings $300-1,000 = evaluate personality fit determining if worthwhile. Savings under $300 = snowball acceptable for most personalities. Takes 20 minutes revealing exact mathematical difference enabling informed method selection impossible when choosing based on general principles without specific debt composition calculation.

2. Complete honest self-assessment determining personality fit for avalanche’s delayed gratification requirements – Answer key questions truthfully: (1) Have I successfully completed other long-term goals requiring 12+ months sustained effort without intermediate victories? Examples: Marathon training, advanced degree completion, career certification programs requiring extended study. (2) Am I motivated primarily by mathematical optimization and efficiency versus psychological wins and celebration? (3) Do I track finances meticulously enjoying spreadsheet analysis and optimization? (4) Can I sustain motivation for 12-18 months before first debt elimination without discouragement? (5) Have previous debt elimination attempts succeeded or failed? If failed, what caused abandonment—discouragement from slow progress or other factors? (6) How do I make major decisions—analytical data-driven versus emotional gut-feeling? Score assessment: Answer “yes” to 5-6 questions = Strong avalanche candidate, disciplined analytical personality compatible with delayed gratification making mathematical optimization appropriate choice maximizing interest savings. Answer “yes” to 3-4 questions = Moderate avalanche candidate, consider hybrid approach (quick win first then avalanche) or avalanche with enhanced tracking showing interest savings creating tangible progress metric. Answer “yes” to 0-2 questions = Poor avalanche candidate, snowball method likely produces better outcomes through psychological momentum preventing abandonment making $500 premium worthwhile execution insurance. Additional consideration: If spousal debt elimination requiring agreement, evaluate both personalities choosing method both can sustain preventing conflict from one partner’s discouragement derailing joint effort. Write assessment: “Personality assessment: [Strong/Moderate/Poor] avalanche candidate. Primary motivation: [Mathematical/Psychological]. Recommended method: [Avalanche/Hybrid/Snowball] based on temperament analysis.” Takes 15 minutes creating honest personality evaluation preventing method-temperament misalignment causing abandonment impossible when choosing methods based on theoretical superiority without self-awareness determining strategic fit.

3. If avalanche chosen, establish interest-savings tracking system creating tangible progress metric during extended first-victory timeline – Create tracking spreadsheet: Columns for Month, Attack Debt Balance, Interest Paid This Month, Interest Saved Versus Minimums, Cumulative Interest Saved, Months Remaining. Calculate monthly interest saved: Compare actual interest paid on aggressive payment versus minimum-only scenario, example—$5,000 balance at 24%, pay $500 ($100 interest, $400 principal) versus minimum $150 ($100 interest, $50 principal), saved $0 interest this month BUT reduced balance $350 more preventing future interest, calculate annual savings $350 × 0.24 = $84 annually = $7 monthly ongoing from this payment. Track cumulative savings: Running total of all interest prevented through aggressive payments versus minimum-only perpetuation, example progression—Month 1: $7 saved, Month 2: $14 saved, Month 3: $22 saved… Month 12: $150 saved, provides tangible progress number despite no account eliminations yet. Visual progress representation: Create bar chart showing attack debt balance declining monthly ($5,000 → $4,500 → $4,000 → $3,500…) plus second chart showing cumulative interest savings increasing ($7 → $14 → $22 → $150…), post prominently (refrigerator, office wall) creating visible daily reminder. Balance milestones celebration: Plan small celebrations every $1,000 reduction on attack debt even without full elimination (example: $5,000 → $4,000 = $25 celebration dinner, $4,000 → $3,000 = another $25 celebration) creating intermediate psychological wins during extended timeline. Monthly review ritual: First of month update tracking, calculate month’s interest saved, review cumulative total, adjust projection to debt-free date if payment increased/decreased. Example monthly update: “Month 8: Attack debt now $3,200 (down $1,800 from start), paid $160 interest versus $240 if minimums only (saved $80 this month), cumulative savings $420 total, 14 months remaining to first elimination.” Takes 1 hour initial setup plus 15 minutes monthly maintenance creating systematic progress tracking preventing discouragement from lack of account eliminations during avalanche’s extended first-victory timeline impossible when relying only on balance reduction without tangible interest-savings metric showing mathematical benefit justifying sustained commitment.

These actions create avalanche method evaluation and implementation foundation within 2 hours—calculated exact interest savings on specific debt ($550 example) determining whether optimization worthwhile versus accepting snowball’s psychological premium, completed honest personality assessment (strong/moderate/poor avalanche candidate) preventing method-temperament misalignment, and established interest-savings tracking system ($7 monthly increasing to $150+ cumulative) creating tangible progress metric maintaining motivation during extended 12-month first-victory timeline—transforming avalanche decision from abstract method choice into data-driven personality-matched strategic selection with systematic execution infrastructure ensuring sustained commitment impossible without calculation-based comparison, self-assessment, and progress tracking enabling appropriate method selection and disciplined implementation.

Quick FAQ

What is debt avalanche method exactly?

Mathematically-optimal debt elimination strategy attacking highest interest rate first regardless of balance size minimizing total interest paid: Core mechanics—List all debts highest to lowest APR (ignore balances completely), pay minimums on all except highest APR, apply all extra payment to highest APR debt, when eliminated roll entire payment to next highest APR creating accelerating payments as expensive debts disappear, repeat until debt-free. Example: $5,000 at 24%, $800 at 22%, $2,500 at 18%, $8,000 at 6%, attack sequence 24% → 22% → 18% → 6% regardless of balances. Mathematical optimization: Every dollar attacking 24% debt saves $0.24 annually in future interest versus same dollar on 6% debt saving only $0.06, maximizing per-dollar interest reduction through highest-rate-first approach. Named “avalanche” because momentum builds as highest-cost debts eliminated creating accelerating interest savings like avalanche gaining speed downhill. Key principle: Prioritizes mathematical efficiency over psychological wins accepting delayed first victory (often 12+ months) requiring discipline and delayed gratification making method optimal for analytical personalities comfortable with extended timelines before tangible progress versus psychology-driven individuals needing quick wins preventing discouragement.

How much does avalanche actually save versus snowball?

Typically $500-2,000 on common debt loads ($15,000-30,000 total) depending on rate composition, not $5,000-10,000 feared making premium modest not massive: Savings determinants—Rate gaps between debts (larger gaps = more savings), total debt amount (higher debt = larger absolute savings even if percentage similar), payment aggressiveness (faster payoff = less time for interest differential to compound). Typical scenario savings: $15,000 total debt across 4-5 accounts ranging 15-24% APR, $700 monthly payment, avalanche total paid $16,200 versus snowball $16,850 = $650 savings (4% difference) over 24-26 month elimination. High-savings scenario: $30,000 debt with extreme rate gaps (26% and 29% cards versus 5% student loans), avalanche saves $1,500-2,500 versus snowball (5-8% difference). Low-savings scenario: $12,000 debt with similar rates (all 16-21% range), avalanche saves $200-400 versus snowball (2-3% difference). Time savings: Avalanche typically 2-4 months faster total elimination through mathematical efficiency. Reality check: $650 typical savings represents 2.3% premium on $28,000 total paid making snowball’s psychological benefits often worthwhile trade-off for non-analytical personalities, while $2,000+ savings scenarios clearly favor avalanche making method choice dependent on specific debt composition not universal superiority. Calculation necessity: MUST calculate personal debt scenario using online calculator determining actual savings before method selection—general estimates insufficient for informed decision-making requiring specific debt composition analysis.

What if I get discouraged before finishing avalanche method?

Switch to snowball immediately rather than abandoning debt elimination entirely, accepting $500 premium worthwhile preventing perpetual debt: Discouragement recognition signs—Lost motivation to make extra payments, reducing payment amounts from initial commitment, avoiding tracking or thinking about debt progress, considering giving up on aggressive elimination returning to minimums only. Immediate intervention: (1) Calculate remaining debt under both methods showing snowball produces first victory within 3-6 months creating motivation renewal versus avalanche requiring 8-12+ more months, (2) Switch to snowball attacking smallest remaining balance providing quick win restoring momentum, (3) Accept $300-500 additional interest cost as execution insurance preventing complete abandonment costing $10,000+ in perpetual debt. Example switch: Started avalanche 6 months ago, attacked $6,000 at 24%, reduced to $3,500, feeling discouraged no accounts eliminated yet. Remaining debts: $3,500 at 24%, $4,200 at 19%, $1,200 at 17%, $7,500 at 6%. Switch decision: Attack $1,200 at 17% next (smallest) eliminating in 3 months creating victory reviving motivation versus continuing $3,500 requiring 9 more months. Cost: Additional $180 interest accepting 17% attack before finishing 24%, benefit preventing complete abandonment saving plan. Alternative: Hybrid approach—finish current $3,500 at 24% (sunk cost, 9 months remaining), THEN switch to snowball for remaining debts capturing most avalanche savings while providing psychological wins on final stretch. Prevention better than cure: If prone to discouragement choose snowball initially rather than starting avalanche and switching later, or use hybrid (quick win first then avalanche) combining psychological boost with mathematical efficiency. Key insight: Completed snowball vastly superior to abandoned avalanche—$650 snowball interest better than $0 of abandoned theoretical avalanche savings making execution probability paramount not theoretical optimization.

Can I combine avalanche with balance transfers for maximum savings?

Yes—powerful combination eliminating interest on attack debt during payoff dramatically increasing total savings: Strategy—Transfer highest APR debt to 0% promotional credit card (typically 12-18 months), attack transferred balance aggressively during promotional period eliminating before reversion to regular APR, roll payment to next highest APR (either transferred again or standard avalanche attack). Example optimization: Have $7,000 at 24% APR (attack debt per avalanche), $4,500 at 19%, $3,200 at 15%, $8,500 at 6%, $900 monthly payment. Transfer $7,000 to 0% for 18 months with 3% fee ($210). Pay $550 monthly to 0% transfer eliminating in 13 months, $350 minimums to other debts. Interest saved: $1,680 (versus 24% standard avalanche) minus $210 fee = $1,470 net savings. After 0% eliminated: Roll $550 to next debt continuing avalanche, dramatically ahead of standard approach. Requirements: Good credit qualifying for 0% transfers (typically 670+ score), discipline avoiding new purchases on transfer card (no grace period), aggressive payment ensuring payoff before promotion ends (reversion to 18-25% negates savings). Optimal combination: Avalanche method identifies highest-cost debts systematically, balance transfers eliminate interest on those debts during payoff, creating maximum mathematical optimization saving $1,500-3,000+ versus standard approaches. Warning: Transfer strategy requires planning—calculate required monthly payment (balance ÷ promotional months) ensuring affordable before transferring, otherwise risk partial payoff and reversion to high regular APR destroying optimization benefit.

Should I ever switch from avalanche to snowball mid-process?

Generally no—method consistency more important than optimization, BUT acceptable if extreme discouragement threatens complete abandonment: Stay avalanche when—Making progress on attack debt even if slow, sustained motivation through interest-savings tracking, first victory approaching within 6 months creating light at tunnel end, committed to mathematical optimization despite extended timeline, personality assessment confirms analytical temperament compatible with delayed gratification. Switch to snowball when—Severe discouragement threatening payment reduction or abandonment, motivation collapse from extended timeline without victories, spousal conflict from invisible progress creating relationship stress, realization that personality assessment was incorrect and need psychological wins. Switching cost analysis: Additional $300-800 interest typical from mid-stream switch versus continued avalanche, acceptable premium preventing $10,000+ cost of complete abandonment through perpetual minimums. Switching mechanics: Immediately redirect all extra payment to smallest remaining balance (regardless of APR), eliminate creating quick win restoring motivation, continue snowball through remaining debts. Example: 8 months into avalanche, attacked $5,500 at 26% down to $2,800, feeling defeated. Remaining: $2,800 at 26%, $3,900 at 21%, $1,400 at 18%, $7,200 at 7%. Avalanche continues attacking $2,800 (7 more months). Snowball switches attacking $1,400 (3 months) creating immediate victory. Decision: If motivation sustainable 7 more months stay avalanche saving $400 interest, if severe discouragement switch to snowball accepting $400 cost preventing abandonment. Prevention better: Choose appropriate method initially through personality assessment rather than switching mid-stream, but switching to snowball superior to abandoning elimination entirely making mid-stream adjustment acceptable when necessary preserving commitment over theoretical optimization.

Explore More in Money Basics

Disclosure

This article provides general educational information about debt avalanche method and debt elimination strategies. Individual debt situations, appropriate methods, payoff timelines, and interest costs vary significantly based on circumstances including total debt, income, expenses, interest rate composition, and individual psychology. This is not financial advice or recommendation that debt avalanche method optimal for all situations. Interest cost comparisons between avalanche and snowball methods represent typical scenarios—actual differences vary based on specific debt compositions, interest rates, and payment amounts. Completion rate statistics represent general observations not scientific controlled studies. Mathematical optimization claims assume consistent payments through completion—actual results depend on sustained commitment without method abandonment. Behavioral finance principles and personality assessments represent general frameworks—individual motivation factors and decision-making styles vary widely beyond simple categorization. Some individuals may achieve better outcomes with debt snowball, hybrid approaches, or other strategies depending on circumstances. Timeline projections and interest savings assume consistent payments without interruption—actual elimination periods vary based on income stability, emergencies, and commitment maintenance. Balance transfer strategies require credit qualification, understanding of terms, and disciplined repayment—not suitable for all situations and carry risks including promotional period expiration. Hybrid approaches require careful evaluation—excessive method switching can reduce execution quality versus consistent singular approach. Switching from avalanche to snowball mid-process acceptable when preventing abandonment but creates additional interest costs requiring cost-benefit analysis. Consult qualified financial professionals, credit counselors, or debt advisors for personalized guidance matching individual situations, debt compositions, and psychological profiles. Focus on sustainable method selection and consistent execution over theoretical optimization. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.