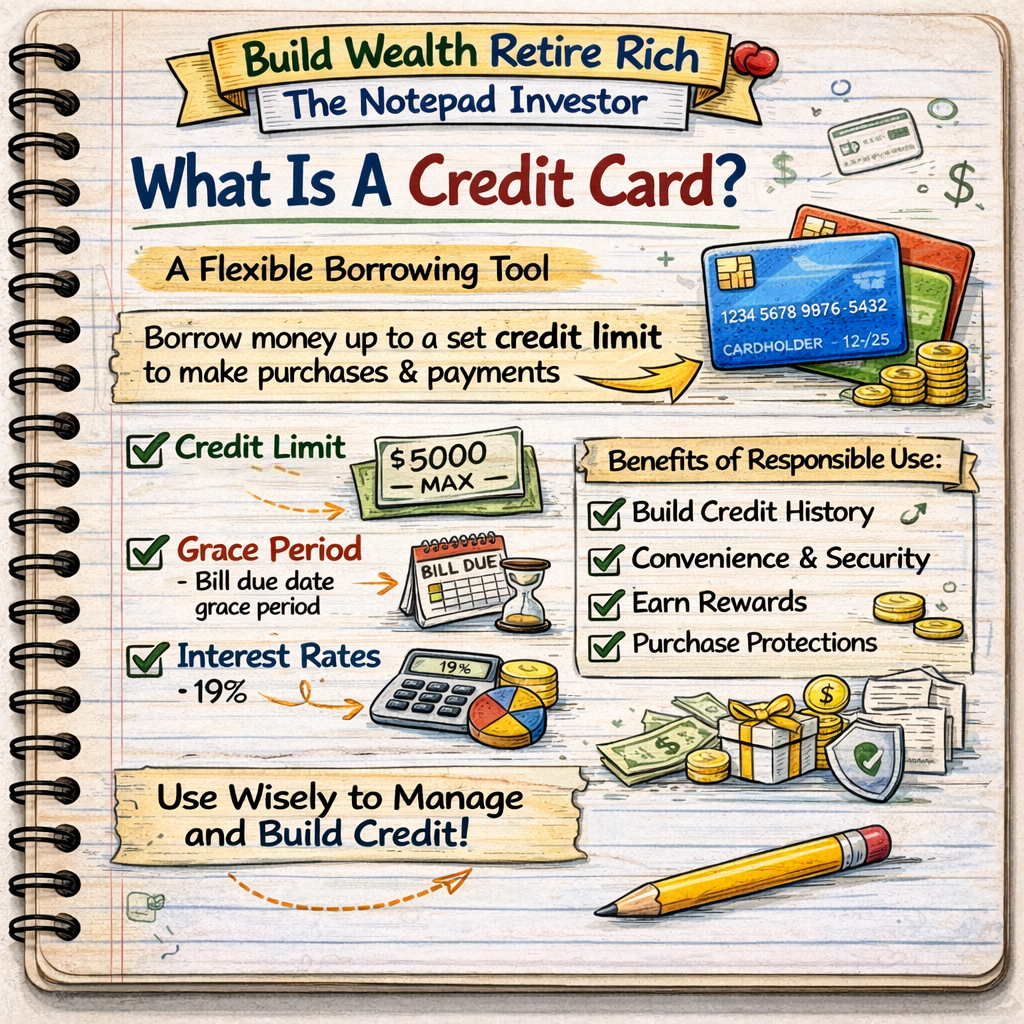

Credit cards allow individuals to borrow money for purchases with the expectation that the balance will be repaid later. While credit cards offer convenience and flexibility, they can also become a significant source of debt if not managed carefully.

Credit card balances typically carry high interest rates compared to other types of loans. When balances are not paid in full each month, interest charges accumulate on the remaining balance.

Over time, interest costs can make it difficult for borrowers to reduce their debt, particularly if only minimum payments are made. Minimum payments often cover only a small portion of the principal, allowing the remaining balance to continue generating interest.

Managing credit card debt effectively involves limiting unnecessary spending, paying balances regularly, and prioritizing repayment of high-interest balances.

Using credit cards responsibly—such as paying the full balance each month—can help individuals avoid interest charges while maintaining a positive credit history.