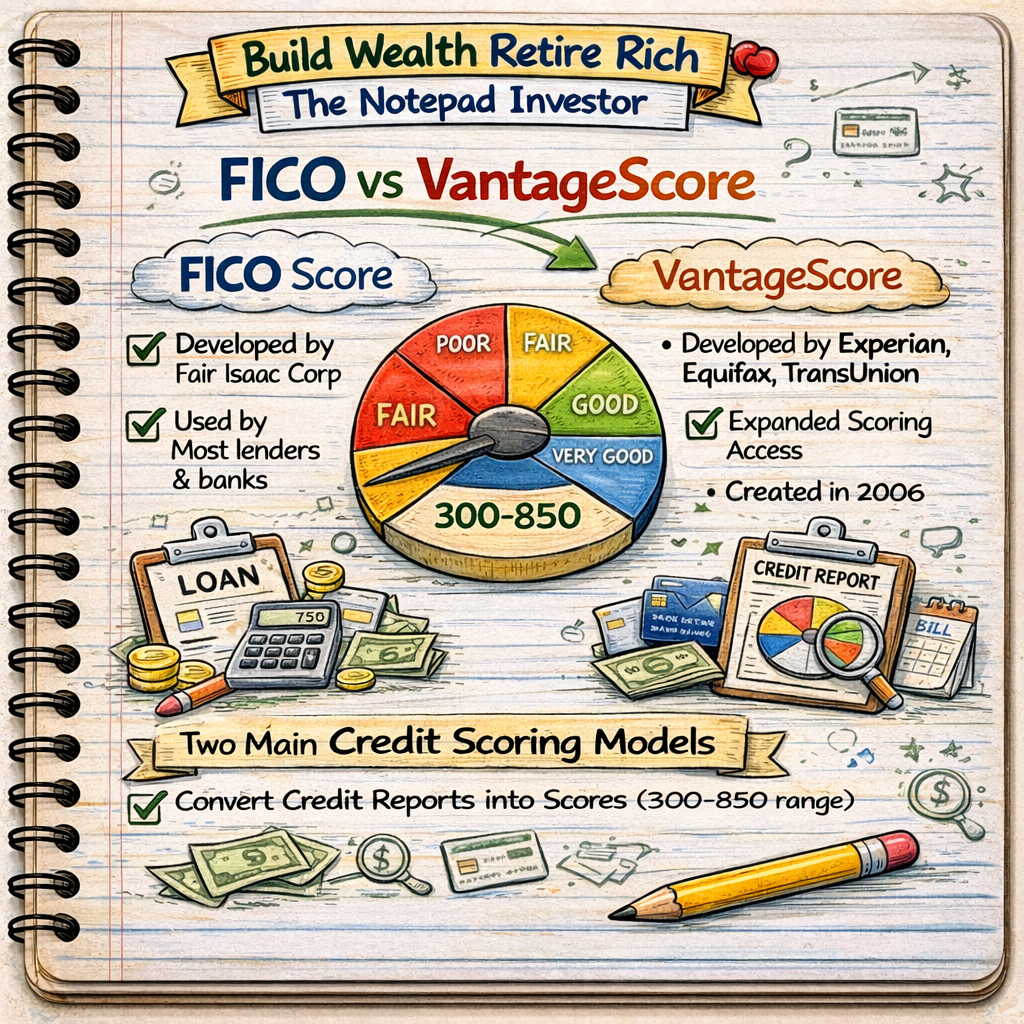

Two of the most commonly used credit scoring systems are FICO and VantageScore. Both systems analyze credit report information to generate a numerical score that helps lenders evaluate credit risk.

The FICO score is one of the oldest and most widely used credit scoring models. Many banks and financial institutions rely on FICO scores when making lending decisions, particularly for mortgages and other major loans.

VantageScore was developed later by the major credit reporting agencies as an alternative scoring model. While it uses similar data from credit reports, the weighting of certain factors may differ slightly.

Both scoring models generally produce scores within a similar range and evaluate similar financial behaviors such as payment history, credit utilization, and credit history length.

Although differences exist between the two systems, the general strategies for maintaining strong credit remain the same: pay bills on time, keep credit balances low, and avoid excessive borrowing.

Understanding these scoring models helps individuals interpret their credit scores and monitor their financial health more effectively.