Automating finances is the systematic use of scheduled automatic transfers, bill payments, and investment contributions eliminating manual monthly financial tasks—including automatic savings transfers on payday, bill autopay for recurring expenses, retirement contribution automation, and investment account deposits occurring without active intervention. Unlike manual money management requiring weekly bill payments, monthly savings transfers, and conscious investment decisions creating opportunity for forgetting, procrastination, or poor timing, financial automation ensures essential actions happen consistently regardless of attention, willpower, or life circumstances through technology executing predetermined financial behaviors automatically.

This article is designed for busy professionals, individuals who struggle with financial consistency, or those wanting to reduce financial decision fatigue. You do not need advanced financial knowledge, expensive software, or complex systems to automate effectively—basic online banking features, employer retirement plans, and simple scheduled transfers create powerful automation requiring minimal initial setup producing ongoing benefits, though method requires sufficient income margin and stable cash flow accommodating automated withdrawals without overdraft risk.

Understanding financial automation matters because manual money management fails during busy periods when bills go unpaid creating late fees and credit damage, savings suffer from procrastination and “I’ll transfer it later” that never happens, and investment timing paralysis prevents regular contributions losing compound growth—while automation users never miss payments avoiding penalties, save consistently hitting targets without willpower, and invest systematically regardless of market conditions building wealth impossible through inconsistent manual approaches requiring constant attention and perfect execution.

Educational disclaimer: This article provides general educational information about financial automation strategies. Individual circumstances, income stability, cash flow patterns, and account features vary significantly. Automation requires careful setup and monitoring—errors can cause overdrafts or missed payments. This is not financial planning or professional advice. Consult qualified financial professionals for personalized guidance.

Understanding Financial Automation

What Is Financial Automation?

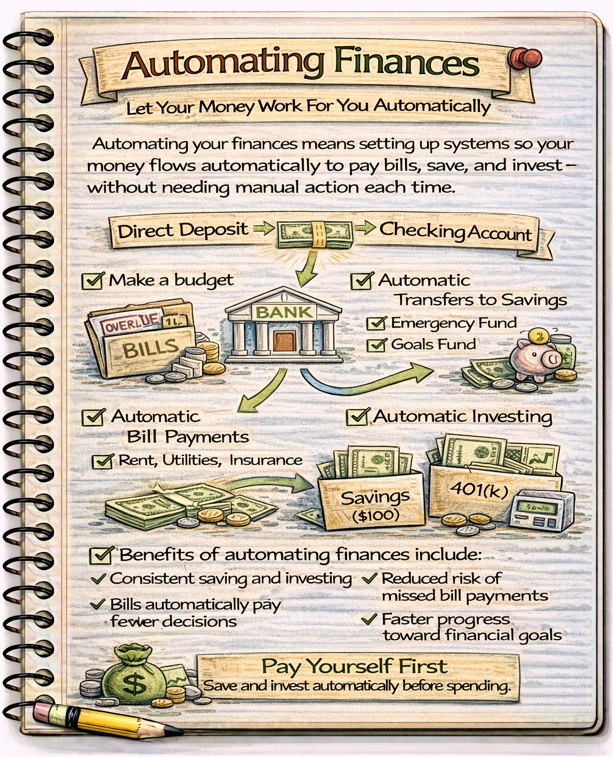

Core definition: Using technology to execute financial transactions and decisions automatically without manual intervention

Common automation areas:

- Savings: Automatic transfers from checking to savings/investment accounts

- Bill payments: Scheduled payments for recurring expenses

- Investments: Automated contributions to retirement and brokerage accounts

- Debt payments: Automatic minimum or fixed payments toward loans

- Income allocation: Direct deposit splitting to multiple accounts

Philosophy: “Set it and forget it”—configure once, benefit continuously without ongoing effort

Why Automation Works

Removes willpower dependency:

- Manual savings requires monthly decision to transfer money

- Easy to skip when month feels tight or other priorities arise

- Automation happens regardless of mood, energy, or competing desires

- Eliminates decision fatigue and procrastination

Ensures consistency:

- Payments happen on same schedule every period

- Savings occur with every paycheck

- Investments continue through market ups and downs

- Creates systematic progress impossible with sporadic manual actions

Prevents timing errors:

- Late payment fees avoided through scheduled payments

- Credit score protected through on-time payment history

- Dollar-cost averaging happens automatically (investing regardless of market timing)

Reduces mental load:

- Fewer financial tasks requiring active monthly attention

- Decreased anxiety about forgetting payments or missing savings goals

- More mental energy for other priorities

Who Benefits Most From Automation

Ideal candidates:

- Busy professionals with limited time for financial management

- People who struggle with savings consistency

- Individuals with stable, predictable income

- Those who’ve experienced late payment fees or missed contributions

- Anyone wanting to reduce financial decision fatigue

- Couples needing simplified coordination

Less suitable for:

- Highly variable irregular income without predictable baseline

- Those living paycheck-to-paycheck with no margin (automation may cause overdrafts)

- People who need hands-on active engagement for motivation

- Individuals in acute financial crisis requiring daily monitoring

Types of Financial Automation

1. Automated Savings

Pay yourself first automation:

- Schedule automatic transfer from checking to savings on payday

- Money moves before you can spend it

- Builds savings consistently without willpower

Example setup:

- Paid bi-weekly on Fridays

- Automatic $500 transfer checking → high-yield savings every other Friday (payday)

- $1,000 monthly savings ($500 × 2) = $12,000 annually automatically

Emergency fund automation:

- Separate savings account for emergency fund only

- Automatic transfers until reaching 3-6 month expense target

- Once goal reached, redirect to other savings goals

Goal-based automation (sinking funds):

- Vacation fund: $200 monthly automatic transfer

- Car replacement: $150 monthly automatic transfer

- Home maintenance: $100 monthly automatic transfer

- Multiple savings goals funded simultaneously automatically

2. Automated Bill Payments

Fixed recurring bills (same amount monthly):

- Rent/mortgage payment

- Car payment

- Insurance premiums

- Subscriptions (streaming, gym, software)

- Phone and internet

Setup method:

- Bank bill pay: Schedule recurring payment from checking account

- Or company auto-draft: Authorize vendor to withdraw payment automatically

- Set payment date few days before due date ensuring on-time payment

Variable bills (fluctuating amounts):

- Utilities (electric, gas, water)

- Credit card bills (if balance varies monthly)

Two approaches:

- Auto-pay full amount: Vendor withdraws actual bill amount each month (recommended for utilities)

- Auto-pay minimum/fixed amount: Set amount withdraws, pay remainder manually if needed (credit cards)

Benefits:

- Never miss payment due date

- No late fees ($25-40 per occurrence)

- Maintains perfect on-time payment history (35% of credit score)

- Eliminates monthly bill-paying session

3. Automated Investing and Retirement

Employer retirement plans (401k, 403b):

- Contribution percentage deducted automatically from paycheck

- Never see money, never miss it

- Dollar-cost averaging happens automatically (buying at all market levels)

- Set percentage, receives automatic raises when salary increases

Example automation:

- Contribute 15% of salary to 401(k)

- $5,000 monthly gross salary × 15% = $750 monthly contribution

- Automatic deduction every paycheck

- $9,000 annual retirement savings without manual action

IRA contributions:

- Schedule automatic monthly transfer from checking to IRA

- $7,000 annual limit (2024) ÷ 12 = $583 monthly automatic transfer

- Maxes IRA without thinking about it

Taxable investment accounts:

- After maxing retirement accounts, automate taxable investing

- Schedule recurring transfer and investment purchase

- Example: $500 monthly → total market index fund automatically

Dividend reinvestment (DRIP):

- Dividends automatically reinvest buying more shares

- Compound growth on autopilot

- No manual reinvestment decisions needed

4. Automated Debt Repayment

Minimum payments automation:

- Schedule automatic minimum payments all debts

- Prevents missed payments and credit damage

- Baseline coverage while planning extra payments manually

Aggressive payoff automation:

- Automate amount exceeding minimum toward target debt

- Example: $200 minimum + $300 extra = $500 automatic monthly payment

- Accelerates payoff without monthly willpower to transfer extra

Debt snowball/avalanche automation:

- Automate minimum payments on all debts

- Automate extra payment toward target debt (smallest balance or highest interest)

- When target debt paid off, manually redirect automation to next debt

5. Income Allocation Automation

Direct deposit splitting:

- Many employers allow splitting paycheck across multiple accounts

- Designate specific amounts or percentages to different accounts

Example allocation:

- $3,000 bi-weekly paycheck

- $500 → high-yield savings (emergency fund)

- $300 → vacation savings account

- $200 → investment account

- $2,000 → checking (living expenses)

Benefit: Money allocated before hitting checking account, before temptation to spend

Setting Up Financial Automation

Step 1: Audit Current Financial Obligations

List all recurring expenses:

- Review last 3 months bank statements

- Identify every recurring charge

- Note: Amount, frequency, due date, payment method

Categorize:

- Fixed amount, same date: Rent, car payment, insurance, subscriptions

- Variable amount, same date: Utilities, credit cards

- Already automated: Current auto-payments

- Manual payments: Currently paying manually each month

Step 2: Create Automation Priority List

Automate in this order:

Priority 1 – Critical payments:

- Housing (rent/mortgage)

- Utilities (prevent shutoffs)

- Minimum debt payments (prevent default)

- Insurance (maintain coverage)

Priority 2 – Savings and retirement:

- Emergency fund transfer

- Retirement contributions

- Goal-based savings

Priority 3 – Discretionary bills:

- Subscriptions

- Memberships

- Non-essential services

Step 3: Set Up Automation Systems

For bill payments, choose method:

Option A: Bank bill pay

- Log into online banking

- Add payee (company name, address, account number)

- Schedule recurring payment: Amount, frequency, start date

- Bank sends payment (electronic or check) on schedule

Option B: Vendor auto-pay

- Log into vendor’s website

- Navigate to payment settings

- Authorize automatic withdrawal from checking or charge to card

- Vendor initiates payment on due date

For savings transfers:

- Log into savings account

- Set up recurring transfer

- Specify: Source account (checking), amount, frequency (monthly/bi-weekly), start date (align with payday)

For retirement:

- 401(k): Contact HR or log into plan website, set contribution percentage

- IRA: Set up recurring transfer with brokerage, automate investment purchase if available

Step 4: Align Automation Timing With Income

Critical for avoiding overdrafts:

If paid bi-weekly:

- Schedule half of monthly automations with paycheck 1

- Schedule half with paycheck 2

- Example: $1,000 monthly savings → $500 each paycheck

If paid monthly:

- Schedule automations few days after payday

- Ensures money available before withdrawals

Automation calendar example (bi-weekly pay on 1st and 15th):

- Paycheck 1 (1st): Rent auto-pay (2nd), savings transfer $500 (2nd), utilities autopay (5th), car payment (5th)

- Paycheck 2 (15th): Insurance autopay (16th), savings transfer $500 (16th), subscriptions (20th), credit card autopay (22nd)

Step 5: Create Monitoring System

Automation isn’t “set and forget forever”—requires periodic review:

Weekly monitoring:

- Quick check account balances ensuring automations occurred

- Verify no overdrafts or failed payments

- 5-10 minutes weekly

Monthly review:

- Review all automated transactions

- Confirm amounts correct

- Check for any errors or unexpected charges

- 15-20 minutes monthly

Quarterly adjustments:

- Update automation amounts for income changes

- Add/remove automated payments as circumstances change

- Rebalance if needed

Annual deep review:

- Complete audit of all automations

- Optimize for new financial goals

- Update for salary changes, expense changes

- 1-2 hours annually

Advanced Automation Strategies

The Two-Account System

Setup:

- Account 1 – Bills account (checking): All fixed bills autopay from here

- Account 2 – Spending account (checking): Variable spending (groceries, gas, discretionary)

How it works:

- Calculate total monthly bills: $2,500

- Paycheck direct deposit: $2,500 → Bills account, remainder → Spending account

- Bills account: Automated payments only, minimal manual activity

- Spending account: All variable expenses, can’t accidentally spend bill money

Benefits:

- Bills always covered (dedicated funding)

- Variable spending visible in spending account balance

- Prevents “I thought I had more money” when forgetting upcoming auto-payments

Percentage-Based Automation

Allocate by percentages instead of fixed dollars:

- 20% → savings

- 10% → investments

- 5% → extra debt payment

- 65% → living expenses

Adapts automatically to income changes:

- Get raise? Automated amounts increase proportionally

- Income decrease? Automated amounts adjust downward maintaining percentages

- Prevents lifestyle inflation through consistent allocation ratios

Automation Laddering for Irregular Income

Challenge: Irregular income makes fixed automation risky (overdrafts)

Solution – Tiered automation:

Tier 1 (Essential bills): Automated at conservative income level

- Automate only essentials at lowest typical monthly income

- Example: Minimum income month $3,000 → automate $2,500 critical bills

Tier 2 (Savings): Manual or triggered by income threshold

- When income exceeds baseline, manually transfer to savings

- Or use conditional automation if available (“if balance > $4,000, transfer $500”)

Tier 3 (Extra goals): Surplus allocation

- High income months, manually allocate surplus to investments, extra debt

Buffer Building

Goal: Build one month’s expenses as buffer in checking

Process:

- Reduce automated savings temporarily

- Build buffer to cover all automated monthly bills

- Once built, restore normal automated savings

- Live on last month’s income (money in checking earned previous month)

Benefit: Eliminates timing anxiety between paychecks and automated withdrawals

Common Automation Mistakes

Over-Automating Without Buffer

Mistake: Automating savings and bills leaving insufficient cushion in checking

Result: Overdraft fees when variable expenses higher than expected or automation timing misaligned

Solution: Maintain $500-1,000 buffer in checking, automate conservatively until stable

No Monitoring After Setup

Mistake: “Set and forget forever” without periodic review

Risk: Errors go unnoticed, amounts become outdated, forgotten subscriptions continue charging

Solution: Weekly quick checks, monthly review, quarterly adjustments

Automating Before Stabilizing Budget

Mistake: Automating aggressively before understanding actual spending patterns

Result: Constantly moving money back from savings to cover overspending

Solution: Track spending 2-3 months manually first, then automate based on realistic patterns

Inflexible Automation During Life Changes

Mistake: Maintaining same automations during job change, income reduction, major life event

Result: Financial stress from automations no longer aligned with circumstances

Solution: Immediately adjust automations when life changes occur, don’t wait for crisis

Forgetting to Update After Paying Off Debt

Mistake: Debt paid off but automated payment continues (if auto-debit) or freed cash flow not redirected

Result: Accidentally overpay closed account or lifestyle inflation consumes freed money

Solution: When debt eliminated, immediately redirect that automated amount to savings/investments

Relying Solely on Vendor Auto-Pay

Mistake: All automation through vendor-initiated withdrawals vs bank-controlled payments

Risk: Less control, harder to stop if dispute occurs, amounts may increase without notice

Solution: Prefer bank bill pay when possible, maintains your control over timing and amounts

Why Financial Automation Matters

Without financial automation, manual money management requires constant attention creating opportunities for forgetting bills and incurring late fees, savings suffer from procrastination and “I’ll do it tomorrow” that never comes, and investment consistency fails during busy periods or market volatility leading to poor timing—while automation users maintain perfect payment histories saving thousands in late fees, build wealth systematically through forced savings occurring before spending temptation, and achieve superior investment returns through dollar-cost averaging impossible with sporadic manual contributions dependent on willpower, mood, and market-timing guesses.

Understanding and implementing financial automation enables individuals to:

- Eliminate late fees and maintain perfect credit through automated on-time payments

- Build wealth consistently through forced savings before spending temptation

- Invest systematically achieving dollar-cost averaging and compound growth

- Reduce financial stress and decision fatigue through systematic execution

- Free mental energy for other priorities through reduced financial task load

- Achieve superior long-term outcomes through consistency impossible with manual approaches

Financial automation transforms inconsistent manual money management into systematic execution producing superior outcomes through consistency, removing willpower dependency, and ensuring essential financial behaviors happen regardless of attention or circumstances.

Common Misunderstandings

Many people assume financial automation means completely hands-off requiring zero monitoring or attention. In reality, automation reduces active tasks from daily/weekly to monthly/quarterly but still requires periodic review ensuring automations functioning correctly, amounts remain appropriate for current circumstances, and no errors or fraudulent charges occurring—proving automation reduces but doesn’t eliminate financial engagement completely.

Another common misconception is that automation only works for high earners with surplus income making it irrelevant for modest earners. In practice, automation works at all income levels through careful setup aligning automated amounts with actual capacity—someone earning $40,000 can automate $200 monthly savings and essential bills just as effectively as someone earning $200,000 automating $10,000, proving principle applies universally when amounts calibrated appropriately.

Some believe automation creates inflexibility making it unsuitable for variable income situations. However, strategic automation using conservative baselines, tiered approaches, or percentage-based methods accommodates irregular income effectively—automating only essentials at minimum income levels while handling variable portions manually provides automation benefits without overdraft risk, proving flexibility and automation compatible through thoughtful design.

How Financial Automation Fits Into Financial Success

Financial automation provides essential infrastructure ensuring consistent execution of core financial behaviors regardless of attention, willpower, or circumstances—eliminates payment failures saving thousands in late fees and credit damage, forces systematic wealth building through automated savings and investing, and creates sustainable long-term financial success through reliable execution impossible with manual approaches requiring perfect discipline and attention month after month for years.

For example, two people each earn $5,000 monthly with goals to save $800 monthly and never miss bill payments. Person A manages manually—intends to transfer $800 monthly to savings and pay all bills on time. Reality: Some months forgets savings transfer (busy, procrastinated, “felt tight”), occasionally pays bills late (traveling, forgot, assumed already paid), averages $450 monthly actual savings (56% of goal) and incurs 3 late fees annually ($120). After year: saved $5,400 versus $9,600 goal, paid $120 late fees, stressed about financial inconsistency. Person B automates everything—sets up automatic $800 savings transfer on payday, autopay for all bills. After year: saved $9,600 (100% of goal), zero late fees, zero stress about financial tasks, total time spent 30 minutes monthly review versus Person A’s hours of manual payments and transfers. Person B achieved $4,200 more savings ($9,600 vs $5,400) plus $120 fee avoidance = $4,320 better outcome simply through automation enabling consistency impossible for Person A despite equal intent.

Financial automation separates successful systematic wealth builders from good-intentioned inconsistent strugglers through reliable execution producing superior outcomes impossible with manual approaches dependent on perfect discipline sustained indefinitely.

Recent Updates and Trends

In recent years, bank technology improvements have simplified automation setup—mobile apps now enabling one-click recurring transfer setup versus previous web-only complex processes, dramatically lowering barrier to automation adoption especially for younger generations preferring mobile financial management.

Artificial intelligence integration has emerged—apps like Digit and Qapital analyzing spending patterns and automatically saving optimal amounts based on available cash flow, creating “smart automation” versus fixed-amount approaches though requiring third-party access raising security considerations.

Direct deposit splitting has become more common—employers increasingly allowing paycheck division across multiple accounts directly enabling pay-yourself-first automation without separate transfer steps, though adoption varies by employer.

Subscription proliferation has created automation challenges—average household carrying 10-15+ automated subscriptions requiring periodic audit preventing forgotten charges accumulating, making automation review more important than ever.

Fundamental financial automation principles remain timeless: systematic execution beats sporadic manual action regardless of intent, removing willpower dependency creates superior consistency, aligning automation timing with income prevents overdrafts, periodic monitoring ensures automations remain appropriate, and forced savings through automation produces wealth accumulation impossible through “save what’s left” manual approaches—regardless of technology improvements, AI integration, or subscription trends, simple systematic automation of savings and bills produces dramatically superior financial outcomes versus manual management dependent on sustained perfect discipline.

3 Things You Can Do Today

Ready to automate your finances? Here are three simple steps you can take right now:

1. Set up one automatic savings transfer starting with next paycheck – Log into savings account online banking today. Set up recurring transfer from checking to savings. Choose realistic amount (10-20% of paycheck if possible, even $50-100 if starting small). Schedule for day after payday (if paid 1st and 15th, schedule transfers for 2nd and 16th). Frequency: Match your pay schedule (bi-weekly or monthly). This single action creates forced savings building wealth automatically. Example: $300 bi-weekly transfer = $7,800 annual savings without thinking about it. Takes 10 minutes setup, benefits forever.

2. Automate your three largest recurring bills – Review last month’s bills. Identify three largest recurring expenses (likely rent/mortgage, car payment, insurance, or utilities). For each one, set up autopay either through your bank bill pay or vendor’s auto-draft. Choose payment date few days before due date ensuring on-time payment. Write down what you automated and when payments occur (for monitoring). This prevents late fees and protects credit score through perfect payment history. Takes 20-30 minutes total setup, saves hours monthly plus late fee prevention.

3. Create simple automation tracking spreadsheet or calendar – Open spreadsheet or use calendar app. List all automated transactions: Savings transfers (amount, date), Bill autopay (vendor, amount, date), Retirement contributions (percentage or amount). This creates monitoring system ensuring automation working correctly. Add recurring calendar reminders: Weekly quick check (5 minutes verifying transactions occurred), Monthly review (15 minutes checking all automations). Without monitoring, automation errors go unnoticed. Takes 15 minutes creating system, prevents automation failures.

These actions create functional automation foundation handling savings and major bills automatically while establishing monitoring system ensuring everything works correctly—transforming manual financial management into systematic automated execution within one day.

Quick FAQ

What if I don’t have enough money to automate savings?

Start smaller than you think necessary—even $25-50 per paycheck creates automation habit and builds momentum. As income increases or expenses decrease, increase automated amount. Key: Start automation principle immediately at any amount rather than waiting for “perfect” circumstances. Someone automating $50 bi-weekly ($100 monthly, $1,200 annually) dramatically outperforms someone planning to save $500 monthly “when I can afford it” that never happens. Start where you are, increase later.

Should I use bank bill pay or vendor auto-pay for bills?

Bank bill pay generally preferred—you control timing and amounts, easier to modify or stop if needed, maintains payment records in one place. Vendor auto-pay acceptable for trusted companies with stable amounts. Avoid for small/unknown vendors or disputed services. If using vendor autopay, verify charge each month ensuring correctness. Never autopay variable bills (like credit cards) in full from vendor—risk of incorrect charges getting paid automatically. Use bank bill pay for maximum control.

How do I prevent overdrafts when automating?

Five strategies: (1) Maintain buffer—keep $500-1,000 minimum in checking always, (2) Align timing—schedule automations 2-3 days after payday ensuring money available, (3) Start conservative—automate less than you think possible, increase gradually, (4) Monitor weekly—catch issues before they cascade, (5) Link overdraft protection—connect savings account as backup (better than overdraft fees). Most automation overdrafts come from poor timing or over-optimistic amounts, both preventable through conservative setup.

What happens if my income changes—do I need to redo all automation?

Income increase: Review and increase automated amounts proportionally (this is good problem). Income decrease: Immediately reduce automated savings/investments temporarily maintaining bill automations. Don’t wait—pause savings automation same day job loss occurs, resume when stabilized. Automations should flex with life changes, not remain static forever. Review quarterly or whenever major life change occurs, adjusting amounts staying aligned with current reality.

Is automation safe? What about fraud or errors?

Generally safe but requires monitoring. Banks have fraud protection and error resolution. However, risks exist: Vendor charging wrong amount (caught through monthly review), automated payment to closed account (update when circumstances change), fraudulent charges continuing via autopay (monitor statements). Mitigation: Use bank bill pay over vendor autopay when possible, review all automated charges monthly, never autopay from debit card (credit card has better fraud protection), maintain alerts for large withdrawals. Automation + monitoring = safe and effective.

Can I automate finances if I have irregular income?

Yes, with modifications: (1) Conservative essential automation—automate only critical bills at your minimum income level, (2) Manual variable handling—manually transfer to savings when income exceeds baseline, (3) Tiered approach—essential bills automated, savings manual until income stabilizes, (4) Buffer building—larger checking buffer (one month expenses) accommodates variability. Many freelancers and business owners successfully use partial automation for predictable minimum expenses while handling variable portions manually. Automation principle works, just adapted to irregular patterns.

Explore More in Money Basics

Disclosure

This article is provided for educational purposes only and does not constitute financial planning or professional advice. Financial automation requires careful setup and monitoring—errors can cause overdrafts, missed payments, or other issues if improperly configured. Individual circumstances vary significantly—income stability, cash flow patterns, and appropriate automation levels differ by person. Examples are illustrative using simplified scenarios—actual situations vary. Bank and app features change frequently—verify current capabilities. Security risks exist requiring vigilance and monitoring. Consult qualified financial planners and advisors for personalized guidance. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.