The cash envelope system is a budgeting method where cash is withdrawn for variable spending categories (groceries, dining out, entertainment, gas, personal care) and divided into labeled physical envelopes, with spending limited to available cash in each envelope—preventing overspending through tangible visibility and forced accountability when envelopes empty. Unlike credit and debit card spending enabling unconscious purchases disconnected from budget limits, physical cash creates psychological friction making each transaction deliberate and visible, with empty envelope serving as hard stop preventing category overspending impossible with digital payments lacking physical constraints.

This article is designed for chronic overspenders, individuals struggling with credit card debt, or those wanting tangible spending control beyond digital tracking. You do not need financial expertise, special tools, or complex systems to implement envelope budgeting—simple cash withdrawal, labeled envelopes, and disciplined spending from designated envelopes create powerful control mechanism working immediately regardless of income level, though method works best for variable expenses while fixed bills still paid electronically for convenience and security.

Understanding the cash envelope system matters because digital payment ease enables unconscious overspending through disconnect between purchase and budget impact, credit cards create delayed consequences facilitating poor decisions, and app-based tracking lacks psychological weight preventing behavioral change—while envelope users experience immediate tangible consequences making overspending psychologically difficult, achieve dramatic spending reductions through forced awareness, and eliminate credit card dependency creating debt-free sustainable spending patterns impossible through digital-only approaches for many people.

Educational disclaimer: This article provides general educational information about cash envelope budgeting methodology. Individual circumstances, spending patterns, and budgeting preferences vary significantly. Cash handling involves theft/loss risks requiring security awareness. This is not financial planning or professional advice. Consult qualified financial professionals for personalized guidance.

Understanding the Cash Envelope System

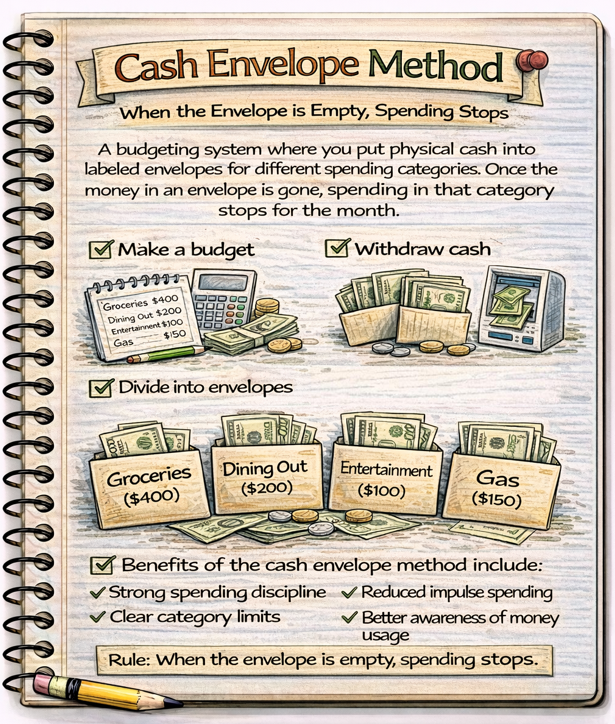

What Is the Cash Envelope System?

Core definition: Physical cash divided into labeled envelopes for specific spending categories, with spending limited to available cash

How it works:

- Create budget identifying variable spending categories

- Withdraw total budgeted amount in cash

- Divide cash into labeled envelopes by category

- Spend only cash from appropriate envelope for purchases

- When envelope empty, stop spending in that category

- Repeat monthly with fresh budget amounts

Example implementation:

- Monthly budget: Groceries $400, Dining out $150, Entertainment $100, Gas $120, Personal care $60

- Withdraw $830 cash at start of month

- Envelope 1: “Groceries” with $400

- Envelope 2: “Dining Out” with $150

- Envelope 3: “Entertainment” with $100

- Envelope 4: “Gas” with $120

- Envelope 5: “Personal Care” with $60

- Grocery shopping: Pay from Groceries envelope only

- Restaurant meal: Pay from Dining Out envelope only

- When Dining Out envelope empty (spent $150), no more restaurants that month

The Psychology Behind It

Tangible visibility creates awareness:

- Physical cash diminishing provides constant visual feedback

- Can see exactly how much remains at any moment

- Empty envelope = clear, undeniable limit reached

- Versus digital spending where limit abstract until checking app

Pain of payment increases with cash:

- Psychological research: Cash spending creates stronger negative emotion than card swipes

- Handing over physical money feels like loss

- Card swipe abstract, delayed consequence

- Cash = immediate tangible sacrifice

Physical constraint prevents overspending:

- Can’t spend $175 dining out when envelope contains $150

- Forced to stay within limits or explicitly transfer from another envelope (conscious decision)

- Credit cards enable overspending without immediate barrier

- Cash creates hard stop

Origin and Popularity

Historical use: Pre-credit card era, most people naturally used cash-based spending, often dividing into jars or envelopes for different purposes

Modern popularization:

- Dave Ramsey’s Financial Peace University prominently features envelope system

- Recommended for debt elimination and overspending correction

- Proven effective for millions struggling with credit card debt

Who it works best for:

- Chronic overspenders needing hard limits

- Credit card debt sufferers breaking card dependency

- People who struggle with abstract digital budgets

- Visual/kinesthetic learners needing tangible feedback

- Anyone who finds digital tracking insufficient for behavioral change

Setting Up the Cash Envelope System

Step 1: Create Budget Identifying Cash Categories

Typical cash envelope categories (variable expenses):

- Groceries: Food for home preparation

- Dining out/restaurants: Eating out, takeout, delivery

- Entertainment: Movies, events, recreation

- Gas/fuel: Vehicle fuel only (or general transportation)

- Personal care: Haircuts, toiletries, cosmetics

- Clothing: Apparel and shoes

- Household items: Cleaning supplies, home goods

- Fun money/blow money: Discretionary spending with no questions

- Coffee/beverages: Coffee shops, drinks out

- Gifts: Birthdays, occasions

NOT typically cash envelope categories (fixed/electronic payments):

- Rent/mortgage (paid electronically for record and security)

- Utilities (electronic bill pay)

- Insurance (automatic payments)

- Subscriptions (credit card or bank draft)

- Debt payments (need payment record)

- Online purchases (can’t use physical cash)

Customization: Choose categories matching YOUR problem areas—if overspend on dining but not entertainment, focus envelope on dining

Step 2: Determine Budget Amount Per Category

Use historical spending as baseline:

- Review last 3 months spending per category

- Calculate average

- Adjust downward if reducing spending is goal

Example budget calculation:

- Groceries last 3 months: $420, $465, $445 = Average $443, round to $450

- Dining out last 3 months: $285, $310, $265 = Average $287, reduce to $200 (goal)

- Entertainment: $135, $90, $110 = Average $112, budget $100

- Gas: $115, $120, $105 = Average $113, budget $120

- Personal care: $65, $70, $55 = Average $63, budget $60

Total monthly cash needed: $930

Step 3: Obtain Physical Envelopes

Options:

- Standard letter envelopes (free or minimal cost)

- Specialized budget envelopes with category labels (sold online, $10-25)

- Small cash envelopes (security envelopes work well)

- Accordion folder with labeled sections

- Cash envelope wallet system (all envelopes in one zippered wallet)

Label each envelope clearly:

- Category name in large letters

- Budget amount for reference

- Optional: Month/date range

Step 4: Withdraw Cash and Fill Envelopes

Timing:

- Beginning of month (or when budget period starts)

- After paycheck deposits clearing

- Or split across multiple paychecks if paid weekly/bi-weekly

Withdrawal strategy:

- Go to bank or ATM

- Withdraw total budgeted amount ($930 in example)

- Request smaller bills ($20s, $10s, $5s) for easier envelope division

- Divide into envelopes immediately at home

Bill denomination recommendations:

- Groceries ($450): Mix of $20s and smaller bills

- Dining out ($200): $20s and $10s

- Entertainment ($100): $20s and $5s

- Gas ($120): $20s

- Personal care ($60): $10s and $5s

Step 5: Spend Only From Designated Envelopes

Shopping process:

- Going grocery shopping? Take Groceries envelope

- At checkout, pay from envelope cash only

- Receive change, put back in same envelope

- Return envelope to storage location

Rules:

- Money in envelope ONLY for that category

- No borrowing from other envelopes without conscious decision and note

- When envelope empty, stop spending in that category

- Change and remaining cash stay in envelope

Step 6: Handle Empty Envelopes

When category depleted mid-month:

Option 1 (Strict):

- Stop spending in that category until next month

- Find alternatives (groceries for dining out, free entertainment, etc.)

- Most effective for breaking overspending habits

Option 2 (Flexible):

- Consciously transfer from another envelope with surplus

- Document the transfer (“Moved $30 from Entertainment to Dining Out”)

- Understand trade-off being made

- Maintains accountability through deliberate choice

Option 3 (Emergency):

- For genuine emergencies only, use emergency fund or savings

- Replenish next month

- Rare exception not regular practice

Practical Implementation Strategies

Hybrid Approach (Cash + Digital)

Reality: Full cash-only living impractical for most people in modern world

Recommended hybrid system:

Use cash envelopes for:

- Variable spending categories where you overspend

- Categories benefiting from tangible limits (groceries, dining, entertainment, shopping)

- Discretionary spending

Use electronic payments for:

- Fixed bills (rent, utilities, insurance)

- Online purchases (Amazon, subscriptions)

- Automatic payments

- Large purchases requiring security/documentation

- Business expenses needing receipts

Example hybrid budget ($4,500 monthly income):

- Electronic payments ($2,900): Rent $1,200, Utilities $180, Car payment $350, Insurance $300, Phone/Internet $140, Subscriptions $65, Debt payments $300, Savings $365

- Cash envelopes ($1,600): Groceries $450, Dining out $200, Entertainment $150, Gas $350, Personal care $80, Clothing $100, Household $80, Miscellaneous $190

Handling Common Situations

Returns and refunds:

- Cash purchases returned for cash → money back in original envelope

- Card purchases (if made) returned to card → doesn’t affect envelopes

Mixed purchases (Target/Walmart):

- Option 1: Bring multiple envelopes, split payment by category (groceries, household, clothing)

- Option 2: Pay from primary category envelope, estimate proportions

- Option 3: Make separate trips for different categories

Gas stations (card required at pump):

- Use debit card at pump

- Immediately remove equivalent cash from Gas envelope, deposit to checking

- Or prepay inside with cash

- Or use gas station gift card purchased with envelope cash

Online purchases:

- Remove cash from appropriate envelope when ordering

- Set aside in “pending” envelope

- Deposit to checking to cover card charge when it posts

- Maintains envelope accountability for online spending

Safety and Security

Storage at home:

- Keep envelopes in secure location (safe, locked box, hidden spot)

- Don’t advertise to visitors where you keep cash

- Consider home safe for large amounts

Carrying envelopes:

- Take only envelope(s) needed for that trip

- Use envelope wallet keeping multiple envelopes together securely

- Be aware of surroundings when handling cash in public

- Don’t flash large amounts of cash

Loss/theft risk management:

- Accept small risk as cost of method’s benefits

- Losing $150 dining envelope once painful but not devastating

- Versus losing thousands to credit card overspending over year

- Risk calculation favors envelope system for chronic overspenders

Tracking and Adjustments

Optional: Keep spending log in envelope

- Small paper slip noting: Date, Store, Amount spent, Balance remaining

- Provides detail beyond just seeing cash diminish

- Helps refine future budget amounts

Month-end review:

- Empty envelopes: Underfunded category or overspending problem

- Substantial surplus: Overfunded, can reduce next month or reallocate

- Adjust next month’s allocations based on learnings

Digital Envelope Systems

Concept: Virtual Envelopes Without Physical Cash

How digital envelope systems work:

- Money stays in bank account

- App or spreadsheet tracks “virtual envelopes”

- Spending tracked against envelope balances

- Maintains envelope principle without cash handling

Digital Envelope Apps and Tools

Goodbudget:

- Digital envelope budgeting app

- Free version: 10 envelopes

- Plus version: $8/month or $70/year, unlimited envelopes

- Syncs across devices

- Maintains envelope discipline without physical cash

Mvelopes:

- Digital envelope system with bank syncing

- $6-20/month depending on features

- Automatic transaction categorization

- Envelope-style interface

YNAB (You Need A Budget):

- Not explicitly “envelopes” but functions similarly

- Assign every dollar to category (envelope principle)

- Digital with envelope-like accountability

- $99/year

Spreadsheet envelope tracking:

- Create virtual envelopes in spreadsheet

- Columns: Category (envelope), Budgeted, Spent, Remaining

- Manually update spending, see balances

- Free but requires discipline

Bank account sub-accounts:

- Some banks allow multiple savings “buckets”

- Create sub-account for each envelope category

- Transfer budgeted amount to each bucket monthly

- Spend from designated bucket

Digital vs Physical: Pros and Cons

Physical cash envelopes advantages:

- Stronger psychological impact (tangible, visible)

- Impossible to overspend (hard physical limit)

- Forces conscious decisions

- Better for breaking credit card dependency

Physical cash envelopes disadvantages:

- Theft/loss risk

- Inconvenient for online purchases

- Some vendors don’t accept cash

- Requires bank trips for withdrawals

- Less detailed spending tracking

Digital envelope advantages:

- No theft/loss risk

- Works for all purchase types including online

- Automatic tracking and reporting

- More convenient

- Detailed transaction history

Digital envelope disadvantages:

- Weaker psychological impact

- Easier to overspend and ignore limits

- Requires app subscription or spreadsheet discipline

- Less effective for chronic overspenders needing hard stops

Recommendation: Start with physical cash for problem categories breaking overspending patterns, transition to digital once self-control established

Success Stories and Results

Typical Outcomes

Spending reductions:

- Groceries: 15-30% reduction through increased awareness and reduced waste

- Dining out: 40-60% reduction (most dramatic category)

- Entertainment: 30-50% reduction through free/low-cost alternatives

- Impulse shopping: 60-80% reduction (physical cash creates friction)

Example transformation:

Before envelope system:

- Groceries: $550 monthly (frequent trips, waste, impulse buys)

- Dining out: $480 monthly (convenience, unconscious frequency)

- Entertainment: $220 monthly (movies, events, activities)

- Shopping: $320 monthly (clothing, home items, impulse)

- Total: $1,570 monthly variable spending

After envelope system (3 months):

- Groceries: $400 monthly (meal planning, shopping lists, reduced waste)

- Dining out: $200 monthly (conscious decisions, pack lunches)

- Entertainment: $120 monthly (free alternatives, selective activities)

- Shopping: $100 monthly (need-based only, no impulse)

- Total: $820 monthly variable spending

- Reduction: $750 monthly = $9,000 annually

Why It Works

Psychological mechanisms:

- Loss aversion: Handing over cash feels like losing something valuable

- Visual feedback: Diminishing stack of bills creates immediate awareness

- Hard constraint: Can’t overspend what’s not there physically

- Pre-commitment: Budgeting upfront removes in-moment decision burden

- Conscious friction: Cash handling slower than card swipe, creates pause for consideration

Best Practices From Successful Users

Start with problem categories only:

- Don’t try all categories immediately

- Focus on 2-3 categories where you overspend most

- Expand once comfortable

Be realistic with amounts:

- Don’t slash budgets 50% first month

- Start with current spending, reduce 10-20% gradually

- Unsustainable cuts lead to system abandonment

Prepare for adjustment period:

- First month challenging while learning

- Some categories will run out, others have surplus

- Adjust allocations month 2-3 based on experience

- By month 4, system feels natural

Involve partner/family:

- Both spouses need buy-in for household categories

- Consider individual “fun money” envelopes for personal spending

- Teach children using envelope system for allowance

Why the Cash Envelope System Matters

Without tangible spending controls, digital payments enable unconscious overspending through abstract transactions disconnected from budget limits, credit cards create delayed consequences facilitating poor decisions and debt accumulation, and app-based tracking lacks psychological weight preventing meaningful behavioral change—while envelope users experience immediate tangible consequences through diminishing visible cash, achieve dramatic spending reductions of 30-50%+ in problem categories through forced awareness, and eliminate credit card dependency creating debt-free sustainable patterns impossible through digital-only approaches for chronic overspenders.

Understanding and implementing the cash envelope system enables individuals to:

- Create hard physical limits preventing overspending in problem categories

- Experience immediate tangible consequences making excess spending psychologically difficult

- Break credit card dependency and eliminate debt accumulation patterns

- Achieve dramatic spending reductions (30-60%) through heightened awareness

- Develop sustainable spending habits through deliberate friction and constraint

- Gain visual control and accountability impossible with abstract digital tracking

The cash envelope system transforms abstract digital budgeting into tangible physical control creating behavioral change and spending reductions impossible through tracking apps alone for many chronic overspenders.

Common Misunderstandings

Many people assume envelope system requires using cash for ALL spending including fixed bills and online purchases. In reality, hybrid approach using cash envelopes only for variable overspending categories while maintaining electronic payments for fixed bills, online purchases, and automatic payments provides practical implementation, proving system targets problem areas not comprehensive cash-only living impossible in modern digital economy.

Another common misconception is that envelope system means never using credit cards again permanently. In practice, envelopes serve as training wheels breaking overspending patterns and credit dependency—many people successfully transition back to responsible card use after 6-12 months establishing self-control, proving method provides temporary intensive intervention not permanent lifestyle requirement though some choose to continue indefinitely.

Some believe cash handling makes envelope system too inconvenient for modern life. However, strategic envelope selection focusing only on 3-5 problem categories rather than all spending, combined with digital payments for everything else, creates manageable implementation requiring only weekly cash handling for targeted categories, proving convenience objection overstated when system thoughtfully customized versus dogmatically applied.

How Cash Envelope System Fits Into Financial Success

Cash envelope system provides intensive behavioral intervention for chronic overspending creating immediate tangible accountability impossible through digital tracking, serves as training mechanism establishing spending discipline and awareness transferable to future budgeting methods, and enables debt elimination through credit card dependency breaking and dramatic discretionary spending reductions, making envelopes powerful temporary or permanent tool depending on individual needs and self-control development.

For example, two people each earn $4,000 monthly struggling with $8,000 credit card debt and chronic overspending. Person A uses budgeting app tracking spending digitally—sees overspending warnings in app, feels guilty, continues swiping card anyway because abstract notifications lack behavioral impact. After year: reduced spending slightly through awareness ($200 monthly saved), paid $2,400 toward debt, still carrying $5,600 balance, frustrated by lack of progress despite “budgeting.” Person B implements envelope system for problem categories (dining out, entertainment, shopping)—withdraws budgeted cash monthly, experiences physical pain handing over bills, sees envelopes empty mid-month forcing free alternatives. After year: Dramatic behavioral change—dining out reduced $350 monthly, entertainment reduced $120 monthly, shopping reduced $200 monthly totaling $670 monthly savings = $8,040 annually. Applied to debt: Eliminated entire $8,000 plus $40 toward building emergency fund. Person B debt-free while Person A still struggling—difference created by tangible physical intervention versus ineffective digital awareness.

Cash envelope system separates successful overspending interventions from failed digital tracking through tangible physical accountability creating behavioral change impossible with abstract app notifications alone for many chronic overspenders.

Recent Updates and Trends

In recent years, cashless business trend has complicated envelope system—some vendors no longer accepting cash requiring hybrid digital approach for envelope accountability with electronic payments, though majority of envelope categories (groceries, gas, dining, entertainment) still widely cash-accepting.

Digital envelope apps have proliferated offering compromise—Goodbudget, Mvelopes, and YNAB providing virtual envelope frameworks for users wanting envelope psychology without cash handling, though effectiveness debate continues whether digital versions provide sufficient behavioral impact.

Social media has created envelope system renaissance—Instagram and TikTok featuring “cash stuffing” videos showing envelope filling and tracking reaching millions of young people rediscovering method, driving renewed popularity especially among debt-payoff communities.

Debit card rewards have created tension—envelope users potentially missing 1-2% cash back rewards from card spending, though overspending prevention savings (30-60% reductions) vastly exceeds reward losses making rewards objection mathematically irrelevant for chronic overspenders.

Fundamental envelope system principles remain timeless: tangible physical cash creates psychological impact digital payments cannot replicate, visible diminishing cash provides constant feedback impossible with abstract balances, hard physical limits prevent overspending more effectively than app notifications, and intensive behavioral intervention through friction and constraint produces lasting spending habit improvements—regardless of cashless trends, digital alternatives, or social media popularity, physical envelope method continues producing dramatic overspending corrections for millions of chronic strugglers where digital tracking alone fails.

3 Things You Can Do Today

Ready to try the cash envelope system? Here are three simple steps you can take right now:

1. Identify your top 3 overspending problem categories – Review last month’s bank and credit card statements. Which variable spending categories exceeded budget or where you felt loss of control? Common culprits: dining out, entertainment, shopping, groceries. Choose your top 3 worst categories. These become your initial envelope categories. Don’t start with all categories—focus on problems. Example: “I overspend on dining out ($450 vs $200 budget), entertainment ($180 vs $100), and shopping ($280 vs $100)” = 3 envelope categories. Takes 10 minutes identifying targets.

2. Set realistic cash budget for each category and obtain envelopes – For each problem category, set budget amount: Start with current spending reduced 20-30% (sustainable cut not unsustainable slash). Example: Dining out currently $450 → budget $300 month 1 (33% reduction). Calculate total cash needed. Purchase or find 3+ envelopes. Label clearly: “DINING OUT – $300,” “ENTERTAINMENT – $100,” “SHOPPING – $75.” Takes 15 minutes establishing amounts and preparing envelopes.

3. Withdraw cash this week and fill your first envelopes – Go to bank or ATM today or tomorrow. Withdraw total amount for your 3 categories (example: $475 total). Request smaller bills ($20s, $10s, $5s). Return home, immediately divide cash into labeled envelopes. Place in secure location. Next purchase in these categories: Take appropriate envelope, pay cash only, return change to envelope. When empty, stop spending that category. This begins your envelope system creating immediate tangible accountability. Takes 30 minutes total (bank trip plus division).

These actions create functioning envelope system for problem categories within one day requiring minimal setup producing immediate behavioral impact through tangible physical spending limits.

Quick FAQ

Do I need to use cash envelopes for ALL my spending?

No—hybrid approach recommended. Use cash envelopes ONLY for variable categories where you overspend (groceries, dining, entertainment, shopping, personal care). Pay fixed bills electronically (rent, utilities, insurance, debt payments). This targets problem areas with intensive intervention while maintaining electronic payment convenience and security for everything else. Most successful users have 3-7 cash envelope categories, not 20+.

What if the envelope runs out before the end of the month?

Three options: (1) Stop spending in that category until next month (strictest, most effective), (2) Consciously transfer money from another envelope with surplus (documents trade-off), (3) Use emergency fund for genuine emergency (rare exception). Empty envelope = wake-up call revealing underfunded category or overspending problem. Month 2 adjust: increase allocation if legitimate need or commit to reduced spending if overspending habit.

How do I handle online purchases with cash envelopes?

When ordering online, immediately remove equivalent cash from appropriate envelope. Set cash aside in “pending” envelope or deposit to checking account to cover card charge. This maintains envelope accountability for digital purchases. Example: Order $75 Amazon household items, remove $75 from household envelope, deposit to checking before card charge posts. Money spent from envelope even though transaction digital.

Isn’t carrying cash dangerous? What about theft or loss?

Risk exists but manageable: (1) Take only envelope(s) needed for that trip, not all envelopes, (2) Use envelope wallet keeping cash secure and organized, (3) Be aware of surroundings when handling cash publicly. Losing $150 dining envelope once is painful but minor compared to thousands lost to credit card overspending annually. Risk-reward calculation favors envelopes for chronic overspenders. Theft risk less than credit card debt damage.

Can I still get credit card rewards with envelope system?

Hybrid approaches exist: Use credit card for purchase, immediately remove equivalent cash from envelope and pay card bill weekly from collected cash. Maintains envelope psychology while earning rewards. However, this requires strong self-discipline—defeats envelope purpose if card enables overspending. For chronic overspenders, missing 1-2% rewards worth sacrificing to prevent 30-50% overspending. Rewards mathematically irrelevant compared to spending control benefits.

How long should I use cash envelopes?

Varies by person: Some use temporarily (6-12 months) breaking overspending habits then transition to digital tracking with established discipline. Others use permanently because tangible control provides ongoing benefit and prevention. Minimum: 3-4 months allowing habit formation and behavioral change. Evaluate after 6 months: If spending controlled and credit cards managed responsibly, can transition to digital. If envelopes removed and overspending returns, resume envelope system. Use as long as beneficial.

Explore More in Money Basics

- Read all Money Basics articles Cash envelope system: Learn psychology, setup steps, hybrid approaches, digital alternatives, safety tips, and tangible spending control.

- Explore the Easy Learning Series library

Disclosure

This article is provided for educational purposes only and does not constitute financial planning or budgeting advice. Cash envelope system requires cash handling involving theft and loss risks—security awareness essential. Individual effectiveness varies—method works excellently for chronic overspenders but may be unnecessary for disciplined spenders. Hybrid approaches combining cash and digital recommended for practical modern implementation. App and software mentions (Goodbudget, Mvelopes, YNAB) are informational—no endorsements implied. Examples are illustrative—actual spending reductions vary by individual discipline and circumstances. Consult qualified financial planners and advisors for personalized guidance. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.