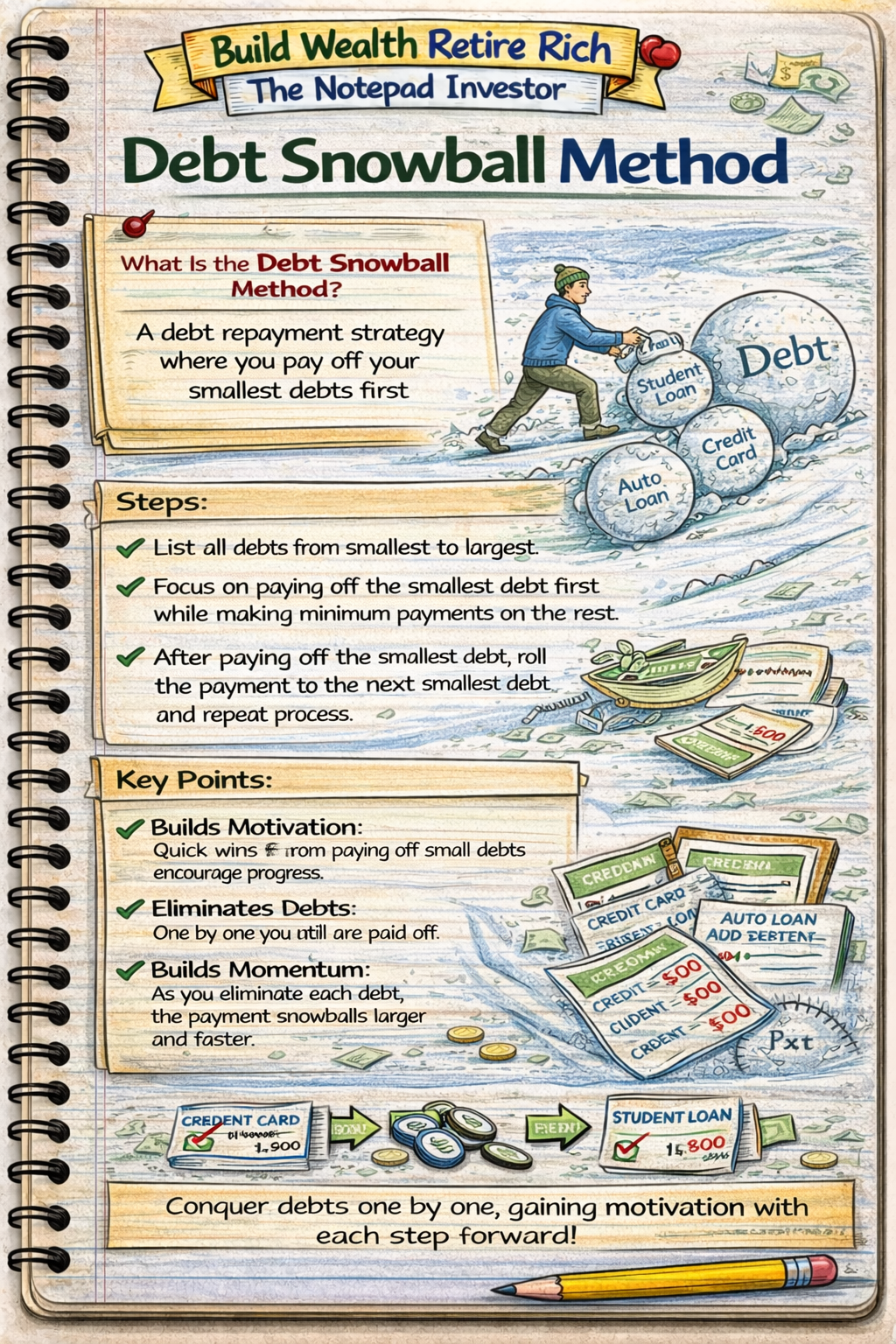

Debt snowball method is debt elimination strategy prioritizing psychological momentum over mathematical optimization by attacking smallest balance first regardless of interest rate—paying minimums on all debts except smallest, applying all extra payment to smallest balance, then rolling entire payment to next smallest when first debt eliminated creating accelerating “snowball effect” through quick wins and increasing payment amounts as debts disappear. Popularized by financial author Dave Ramsey, snowball method explicitly sacrifices mathematical efficiency (costs $200-1,000 more interest than debt avalanche attacking highest APR first on typical $15,000 total debt) in exchange for behavioral advantages—seeing account balances reach zero within 3-6 months creates motivation surge and tangible progress maintaining long-term commitment versus avalanche’s delayed gratification potentially causing abandonment before completion. While debt avalanche saves maximum interest mathematically optimal for disciplined number-focused individuals, snowball method produces superior outcomes for psychology-driven majority who need quick wins preventing discouragement during 18-36 month elimination journey, making $500 extra interest cost worthwhile investment preventing $15,000 debt perpetuation through method abandonment, demonstrating behavioral finance principle that imperfect plan executed consistently beats perfect plan abandoned halfway creating snowball’s practical superiority despite mathematical inferiority for most debt-burdened individuals requiring motivation maintenance impossible through interest-rate-focused approaches lacking visible progress milestones.

This article is designed for anyone carrying multiple debts wanting proven elimination strategy, individuals who’ve failed previous debt payoff attempts needing motivation-focused approach, or those confused by debt avalanche versus snowball debate. You do not need financial expertise to understand snowball method—fundamental concept accessible as simple ranked list and payment allocation, though requires honest self-assessment recognizing whether motivated by mathematical optimization or psychological wins, disciplined commitment maintaining aggressive payments for 18-36 months without deviation, and behavioral awareness that quick victories prevent discouragement enabling long-term adherence impossible when focusing solely on interest savings without considering human motivation factors driving actual completion versus theoretical efficiency.

Understanding debt snowball method matters because psychological barriers cause 80%+ of debt elimination attempts to fail within 6 months making behavioral approach more important than mathematical optimization, quick wins within 3-6 months create momentum maintaining 18-36 month commitment required for complete elimination, and increasing payment amounts through rolled balances provide tangible acceleration preventing plateau discouragement—while snowball-method users complete debt elimination in 24-30 months paying $500-1,000 extra interest but achieving debt freedom versus avalanche abandoners perpetuating debt indefinitely through discouragement costing $10,000+ in continued interest accumulation, proving $500 method premium represents excellent investment in completion probability creating dramatically superior real-world outcomes despite inferior theoretical mathematics impossible without understanding behavioral finance principles valuing execution over optimization.

Educational disclaimer: This article provides general educational information about debt snowball method. Individual debt situations, appropriate strategies, payoff timelines, and interest costs vary based on circumstances including total debt, income, expenses, interest rates, and payment capacity. This is not financial advice or recommendation that snowball method optimal for all situations. Debt elimination requires sustained discipline regardless of method chosen. Some situations may benefit from debt avalanche or hybrid approaches. Consult qualified financial professionals or credit counselors for personalized guidance matching individual circumstances and psychological profiles.

Snowball Method Fundamentals

How Snowball Method Works

Core principles:

- List all debts from smallest to largest balance

- Ignore interest rates completely in ranking

- Pay minimum payments on all debts except smallest

- Apply all extra available payment to smallest balance

- When smallest eliminated, roll entire payment to next smallest

- Repeat until all debts eliminated

Step-by-step implementation:

Step 1: List all debts smallest to largest

- Store card: $800 at 22% APR, $25 minimum

- Credit card A: $2,500 at 18% APR, $75 minimum

- Credit card B: $5,000 at 24% APR, $150 minimum

- Auto loan: $8,000 at 6% APR, $250 minimum

- Student loan: $15,000 at 5% APR, $180 minimum

Step 2: Calculate total available monthly payment

- Required minimums: $680 total

- Extra from budget: $320

- Total available: $1,000 monthly

Step 3: Allocate payments using snowball ranking

- Store card: $25 minimum + $320 extra = $345 total (attack smallest)

- Credit card A: $75 minimum only

- Credit card B: $150 minimum only

- Auto loan: $250 minimum only

- Student loan: $180 minimum only

Step 4: Eliminate first debt and roll payment

- Store card: Paid off in 3 months ($345 × 3 = $1,035 covers $800 + interest)

- Roll $345 to Credit card A creating $420 monthly payment ($75 + $345)

- Continue minimums on remaining debts

Step 5: Continue snowball through all debts

- Credit card A: Paid in additional 7 months with $420 monthly

- Roll $420 to Credit card B creating $570 monthly ($150 + $420)

- Credit card B: Paid in additional 10 months

- Roll $570 to Auto loan creating $820 monthly

- Auto loan: Paid in additional 10 months

- Roll $820 to Student loan creating $1,000 monthly

- Student loan: Paid in additional 16 months

- Total timeline: 46 months (under 4 years) completely debt-free

The Snowball Effect Visualization

Payment amount growth:

- Months 1-3: $345 attacking store card

- Months 4-10: $420 attacking Credit card A (21% increase)

- Months 11-20: $570 attacking Credit card B (36% increase from start)

- Months 21-30: $820 attacking Auto loan (138% increase from start)

- Months 31-46: $1,000 attacking Student loan (190% increase from start)

Why it’s called “snowball”:

- Like snowball rolling downhill gaining mass and momentum

- Payment amounts accelerate as debts eliminated

- Psychological momentum builds with each victory

- Final debts fall quickly despite larger balances through massive payments

Key Snowball Principle: Psychology Over Mathematics

Deliberate trade-off:

- Snowball costs more interest than debt avalanche (highest APR first)

- Accepts $200-1,000 premium on typical debt loads

- Invests extra cost in motivation maintenance and completion probability

- Behavioral finance: Executed imperfect plan beats abandoned perfect plan

Why quick wins matter more than interest savings:

- First debt elimination in 3-6 months provides tangible victory

- Proves method works creating belief in process

- Reduces number of bills and payment dates immediately

- Creates celebration moments maintaining 2-3 year commitment

- Prevents discouragement from slow initial progress attacking large balances

Snowball vs Avalanche Comparison

Debt Avalanche Method (Mathematical Alternative)

Avalanche approach:

- List debts from highest to lowest APR (ignore balances)

- Pay minimums on all except highest APR

- Apply all extra to highest APR debt

- Minimizes total interest mathematically

- Best for disciplined number-focused individuals

Same example using avalanche:

- Credit card B: $5,000 at 24% APR (highest, attack first)

- Store card: $800 at 22% APR

- Credit card A: $2,500 at 18% APR

- Auto loan: $8,000 at 6% APR

- Student loan: $15,000 at 5% APR

Avalanche allocation ($1,000 total monthly):

- Credit card B: $150 minimum + $320 extra = $470

- Store card: $25 minimum

- Credit card A: $75 minimum

- Auto loan: $250 minimum

- Student loan: $180 minimum

Side-by-Side Results Comparison

Total debt: $31,300 across 5 debts, $1,000 monthly payment

SNOWBALL METHOD:

- First victory: Month 3 (store card eliminated)

- Second victory: Month 10 (Credit card A eliminated)

- Third victory: Month 20 (Credit card B eliminated)

- Fourth victory: Month 30 (Auto loan eliminated)

- Final victory: Month 46 (Student loan eliminated, DEBT FREE)

- Total paid: $32,850

- Total interest: $1,550

- Timeline: 46 months

AVALANCHE METHOD:

- First victory: Month 12 (Credit card B eliminated)

- Second victory: Month 13 (Store card eliminated)

- Third victory: Month 19 (Credit card A eliminated)

- Fourth victory: Month 28 (Auto loan eliminated)

- Final victory: Month 44 (Student loan eliminated, DEBT FREE)

- Total paid: $32,100

- Total interest: $800

- Timeline: 44 months

AVALANCHE ADVANTAGE:

- Interest savings: $750 (2.3% less total paid)

- Time savings: 2 months faster

SNOWBALL ADVANTAGE:

- First win: Month 3 vs Month 12 (9 months earlier motivation boost)

- Victories by 1 year: 2 debts vs 0 debts (tangible progress earlier)

- Psychological momentum: Consistent quick wins every 3-7 months

When to Choose Each Method

Choose SNOWBALL when:

- Previous debt elimination attempts failed due to discouragement

- Need motivation and quick wins to maintain commitment

- Multiple small balances under $2,000 enabling rapid victories

- Emotionally driven decision-maker valuing progress over optimization

- Interest rate differences relatively small (all debts 15-25% range)

- Family debt elimination requiring spousal motivation through visible wins

Choose AVALANCHE when:

- Highly disciplined and number-focused personality

- Motivated by mathematical optimization and interest savings

- Large interest rate gaps (24% credit card vs 4% auto loan)

- Comfortable with delayed gratification waiting 12+ months for first win

- Strong intrinsic motivation not requiring external validation

Consider HYBRID approach when:

- Want quick win but also significant rate gaps

- Snowball smallest debt under $1,000 for immediate victory

- Then switch to avalanche for remaining debts

- Captures psychological boost plus mathematical efficiency

Implementing Snowball Method Successfully

Step 1: Create Complete Debt Inventory

Information needed for each debt:

- Creditor name

- Current balance (exact amount)

- Interest rate (APR)

- Minimum payment amount

- Payment due date

- Account number (for tracking)

Organization method:

- Spreadsheet listing all debts

- Rank by balance smallest to largest

- Calculate total debt and total minimum payments

- Identify attack debt (smallest balance)

Step 2: Determine Total Available Payment

Calculate payment capacity:

- Sum all minimum payments required

- Add any extra available from budget

- Include irregular income (100% to debt)

- Total = minimum firepower for snowball

Finding extra payment amount:

- Budget analysis revealing discretionary cuts ($200-500 typical)

- Side income (DoorDash, freelance, overtime) = $400-800

- Expense reductions (subscriptions, dining, shopping) = $300-600

- Target: 20-40% increase above minimums accelerating elimination

Example capacity calculation:

- Required minimums: $680

- Budget cuts: $300 (dining out eliminated, subscriptions canceled)

- Side gig: $400 (DoorDash 12 hours weekly)

- Total capacity: $1,380 monthly (103% increase over minimums)

Step 3: Set Up Payment Automation

Automation strategy:

- Automatic minimums on all non-attack debts (prevents missed payments)

- Manual extra payment to attack debt (allows flexibility increasing amounts)

- Set up day after payday ensuring funds available

- Calendar reminders for manual attack payment

Payment timing:

- Biweekly approach: Half total available every 2 weeks (26 payments = 13 monthly)

- Monthly approach: Full amount on specific date after income received

- Hybrid: Minimums automated, extra applied whenever funds available

Step 4: Track Progress and Celebrate Wins

Progress tracking methods:

- Spreadsheet updating balances monthly

- Visual thermometer or chart showing payoff progress

- Debt-free countdown (months remaining to final debt elimination)

- Running total of interest saved through aggressive payments

Celebration milestones:

- Each debt eliminated: Small celebration (dinner, activity under $50)

- 50% total debt paid: Moderate celebration

- Final debt eliminated: Significant celebration (budgeted $200-500)

- Visual markers: Cut up paid-off credit cards, frame final statement

Step 5: Roll Payments and Maintain Momentum

Payment rolling process:

- When debt eliminated, immediately redirect entire payment to next smallest

- Update budget allocating freed minimum to attack debt

- Resist temptation to reduce total payment amount

- Maintain or increase total debt payment throughout process

Momentum maintenance:

- Review progress weekly reinforcing commitment

- Share victories with accountability partner or community

- Calculate months until next victory maintaining excitement

- Visualize debt-free future during difficult moments

Common Snowball Challenges and Solutions

Challenge: First Debt Taking Longer Than Expected

Problem scenario:

- Smallest debt: $2,500

- Available payment: $400 monthly

- Expected timeline: 6-7 months

- Reality: Interest and unexpected charges extend to 8-9 months

- Frustration threatens commitment

Solutions:

- One-time payment boost: Apply tax refund, sell items, extra work week

- Temporary payment increase: $100-200 extra for 2-3 months forcing completion

- Stop using card preventing new charges adding to balance

- Focus on progress not perfection: 8 months still victory versus indefinite minimum payments

Challenge: Temptation to Deviate from Smallest Balance

Common deviation thoughts:

- “Credit card at 24% costing more interest than $800 store card at 22%”

- “Makes more sense to attack higher rate first”

- Switching to avalanche mid-process

Why consistency matters:

- Method-switching reduces psychological momentum

- Quick win from small balance more valuable than interest savings

- Commitment to single approach prevents analysis paralysis

- If avalanche better fit, should have chosen initially not mid-stream

Resolution:

- Stay committed to snowball through first debt elimination

- Evaluate method after experiencing first victory

- Calculate actual interest difference (usually $50-200 not thousands)

- Remember: Completion more important than optimization

Challenge: Income Disruption During Elimination

Disruption scenario:

- Job loss, hours reduction, or unexpected expenses

- Cannot maintain aggressive payment amount

- Risk of abandoning method entirely

Survival strategies:

- Temporarily revert to minimums only (preserves accounts good standing)

- Maintain debt-free mindset and tracking

- Resume aggressive payments immediately when income stabilizes

- Small payments better than zero: Even $50 extra maintains momentum

- Use disruption to cut expenses further (more aggressive than initial budget)

Challenge: Lifestyle Inflation Pressure

Temptation pattern:

- After 12 months, eliminated 2 small debts

- Psychologically feels like “more money available”

- Temptation to reduce debt payment amount

- “Deserve a break” or “treat myself” thinking

Resistance tactics:

- Automatic payment increases preventing manual reduction

- Visualization: Calculate months until complete freedom

- Small planned rewards (under $50) at milestones preventing major deviation

- Accountability partner preventing lifestyle creep

- Remember: Temporary sacrifice, permanent freedom

Challenge: Spousal Agreement on Method

Disagreement scenario:

- One spouse prefers snowball, other prefers avalanche

- Mathematically-minded partner resents “wasting” interest money

- Conflict threatens joint debt elimination effort

Resolution approaches:

- Calculate actual interest difference (usually $500-1,500 not $10,000)

- Frame as marriage investment: $500 for harmony and momentum worth cost

- Compromise: Snowball first small debt, evaluate after victory together

- Hybrid: Attack one small debt for quick win, then switch to avalanche

- Focus on agreement: ANY method better than continued perpetual minimums

Maximizing Snowball Success

Intensity Techniques

Temporary extreme measures accelerating elimination:

Spending freeze (30-90 days):

- Zero discretionary spending beyond essentials

- Redirect 100% of normal discretionary budget to smallest debt

- Example: $600 monthly discretionary frozen = first debt $1,200 eliminated in 2 months versus 4 months

Side income sprint:

- Temporary second job or intensive gig work

- 100% of side income to debt (not incorporated into regular budget)

- Example: 20 hours weekly DoorDash = $800-1,000 monthly extra eliminating small debts in weeks not months

Sell-everything approach:

- Garage, basement, storage unit purge

- Online marketplace sales (Facebook, OfferUp, eBay)

- Large items (spare vehicle, boat, RV, equipment)

- Example: $3,000 from selling accumulated items eliminates 2-3 small debts immediately

Psychological Reinforcement

Visual progress tracking:

- Thermometer chart on refrigerator showing payoff progress

- Debt chains: Paper links for each $100, remove as paid creating visual shrinking

- Before/after comparison: Initial debt list versus current (cross off eliminated accounts)

Community and accountability:

- Online debt-free communities sharing victories

- Accountability partner checking in weekly

- Family involvement: Kids tracking progress earning small rewards at milestones

- Social media sharing (if comfortable) creating public commitment

Reward structure:

- Each debt eliminated: $25-50 celebration meal or activity

- Halfway point: $100-150 special experience

- Final debt: $300-500 budgeted celebration vacation or major experience

- Rewards pre-planned maintaining motivation through difficult months

Avoiding New Debt

Prevention during elimination:

- Credit cards: Cut up or freeze in ice block preventing use

- Cash-only lifestyle: Debit card for fixed bills, cash envelopes for variable

- Emergency buffer: $1,000 starter fund before aggressive debt attack

- No new debt rule: Absolute commitment regardless of temptation

Emergency handling:

- True emergency: Use starter fund, pause debt payments to replenish

- Pseudo-emergency: Delay or find alternative (borrow item, cheaper solution)

- Resume aggressive payments immediately when emergency fund restored

Why Understanding Debt Snowball Method Matters

Without understanding debt snowball method, individuals either perpetuate debt through minimum-only payments lacking elimination strategy or abandon mathematically-optimal avalanche method through discouragement from delayed first victory requiring 12+ months without tangible progress, missing behavioral approach proven creating 3-6 month quick wins maintaining motivation through 24-36 month elimination journey—while snowball-method users complete debt freedom in 24-30 months through consistent execution despite paying $500-1,000 extra interest, versus avalanche abandoners perpetuating debt indefinitely costing $10,000+ continued interest or random-payment users lacking systematic approach never achieving momentum, demonstrating behavioral finance principle that executed imperfect plan dramatically superior to theoretically-optimal plan abandoned halfway creating snowball’s practical superiority for psychology-driven majority requiring celebration milestones impossible through interest-rate-focused approaches prioritizing mathematics over human motivation factors.

Understanding debt snowball method enables individuals to:

- Implement proven psychological approach prioritizing execution over optimization

- Achieve quick wins within 3-6 months creating motivation maintaining long-term commitment

- Experience increasing payment amounts through rolled balances providing tangible acceleration

- Make informed method choice recognizing personality fit (snowball vs avalanche)

- Maintain consistency through single systematic approach preventing method-switching paralysis

- Celebrate progress milestones reinforcing commitment during difficult months

- Accept deliberate interest premium as worthwhile investment in completion probability

Debt snowball knowledge transforms debt elimination from theoretical mathematical exercise into practical behavioral strategy optimizing human psychology over pure numbers, enabling completion through quick wins and momentum versus abandonment through discouragement impossible without understanding that $500 extra interest cost represents excellent investment ensuring execution versus perpetual debt costing $10,000+ through method abandonment or lack of systematic approach.

Common Misunderstandings

Many people assume debt avalanche always superior because it minimizes interest mathematically. In reality, 80%+ of debt elimination attempts fail within 6 months through discouragement making completion probability more important than theoretical optimization—snowball’s $500-1,000 extra interest on typical $15,000 debt represents 3-7% premium ensuring execution through quick wins versus avalanche’s zero cost if abandoned after 6 months perpetuating $15,000 debt indefinitely costing $10,000+ in continued interest, proving executed snowball producing $10,000+ better outcome than abandoned avalanche despite mathematical inferiority demonstrating behavioral finance reality that imperfect plan completed beats perfect plan abandoned.

Another common misconception is snowball method wastes thousands in unnecessary interest versus avalanche. In practice, interest difference typically $200-1,000 on common debt loads ($10,000-20,000 total) not $5,000-10,000 feared—example: $15,000 across 4 debts, $800 monthly, snowball costs $1,200 interest versus avalanche $850 ($350 difference = 2.3% of total paid), making premium negligible investment in motivation maintenance through 24-30 month journey proving interest gap smaller than anticipated while psychological benefits substantial creating worthwhile trade-off not wasteful spending spree as commonly portrayed by avalanche advocates.

Some believe switching between snowball and avalanche mid-process optimizes both psychology and mathematics. However, method consistency more important than hybrid optimization—switching creates confusion about current strategy, reduces psychological momentum from committed singular approach, and creates decision fatigue at each debt transition questioning whether to continue method or switch, proving hybrid approach’s attempted optimization actually reduces execution quality versus committed snowball or avalanche completion demonstrating value of singular systematic approach chosen upfront and executed consistently regardless of temptation toward mid-stream optimization.

How Debt Snowball Understanding Fits Into Financial Success

Debt snowball understanding enables systematic elimination completing debt freedom in 24-30 months through proven behavioral approach versus perpetual minimum payments or abandoned mathematical methods, provides psychological momentum through 3-6 month quick wins maintaining commitment impossible through delayed-gratification approaches lacking tangible progress, and creates increasing payment acceleration through rolled balances demonstrating compound progress reinforcing long-term adherence—making snowball literacy essential component of debt freedom for psychology-driven majority requiring motivation maintenance, proving $500-1,000 interest premium worthwhile investment ensuring completion versus theoretical savings from abandoned optimal approach, and enabling informed method selection recognizing personality fit optimizing execution probability over mathematical perfection impossible without understanding behavioral finance principles valuing completed action over theoretical optimization.

For example, two individuals both age 32 with identical $18,000 debt across 5 accounts ranging $800-$6,000 balances and 15-24% APRs. Person A mathematically-inclined, calculates avalanche saves $650 interest versus snowball, implements avalanche attacking $6,000 at 24% first. Month 1-6: Pays $900 monthly ($530 minimums + $370 extra), $6,000 balance drops to $3,800, feels slow progress attacking large balance, no victories yet. Month 7-9: Gets discouraged seeing 5 accounts still active despite $8,100 paid total, feels defeated by lack of tangible accomplishment, questions if working. Month 10: Holiday spending temptation, reduces payment to $530 minimums only “temporarily.” Month 12-18: Never resumes aggressive payments, perpetually paying minimums on all 5 accounts, debt barely shrinking. Age 40 (8 years later): Still carrying $12,000 across 3 remaining accounts, paid $48,000 total over 8 years ($18,000 principal + $30,000 interest), nowhere near debt-free from method abandonment. Person B understands snowball method, implements smallest-first approach despite knowing costs $650 extra interest. Lists debts: $800, $1,500, $3,200, $6,000, $6,500. Month 1-2: Attacks $800 balance paying $900 monthly ($530 minimums + $370 to smallest), eliminates first debt month 2. Celebration: Cuts up card, announces victory to spouse, feels motivated seeing 4 accounts remaining versus original 5. Month 3-5: Rolls $150 freed minimum to next debt, attacks $1,500 with $520 monthly, eliminates month 5. Now 3 accounts remaining, psychological momentum building. Month 6-11: Attacks $3,200 with $595 monthly, eliminates month 11. Halfway celebration: Special dinner, reviews progress (3 of 5 debts eliminated, $5,500 of $18,000 paid). Month 12-21: Attacks $6,000 with $745 monthly, eliminates month 21. Final push: One debt remaining! Month 22-29: Attacks final $6,500 with $900 monthly, completely debt-free month 29 (under 2.5 years). Age 34 (2.5 years later): Debt-free, paid $19,650 total ($18,000 principal + $1,650 interest), immediately redirects $900 monthly to investments. Age 40 (8 years total): Invested $900 monthly for 5.5 years (66 months) at 8% return = $85,000 accumulated wealth. Difference: Person A’s avalanche abandonment through discouragement created $12,000 remaining debt plus $30,000 interest paid = $42,000 hole, Person B’s snowball completion created $85,000 wealth despite $650 extra interest during elimination demonstrating $127,000 outcome difference ($42,000 hole versus $85,000 wealth) from understanding behavioral approach valuing execution through quick wins over mathematical optimization leading to abandonment impossible without snowball method literacy recognizing human psychology more important than interest rate mathematics for successful debt elimination.

Debt snowball understanding separates successful debt eliminators completing freedom through behavioral approach from failed mathematical optimizers abandoning strategies lacking psychological reinforcement, requiring method comprehension valuing execution probability over theoretical savings enabling informed personality-based selection producing dramatically superior real-world outcomes impossible without behavioral finance literacy.

Recent Updates and Trends

In recent years, debt snowball method has gained mainstream acceptance through social media success stories and financial influencer promotion making behavioral approach more culturally normalized, though fundamental psychological principles unchanged requiring quick wins maintaining motivation regardless of social validation or community support amplifying core method mechanics through shared celebration impossible to achieve in isolation.

Online debt payoff communities and apps have proliferated providing digital tracking, celebration sharing, and accountability partnerships enhancing traditional snowball method through technology-enabled connection, though basic smallest-first approach works identically with or without digital tools making community support valuable enhancement not requirement for successful execution when individual commitment strong.

Debate intensity between snowball and avalanche advocates has increased creating tribal loyalty to specific methods, though individual personality fit more important than universal superiority with snowball optimal for psychology-driven individuals and avalanche for disciplined number-focused personalities making method selection personal optimization not one-size-fits-all declaration requiring honest self-assessment rather than dogmatic adherence to single approach.

Financial advisors increasingly recognize behavioral finance importance acknowledging that theoretically-optimal strategies fail when abandoned making execution-focused approaches practically superior, though some remain avalanche purists dismissing $500-1,000 snowball premium as wasteful despite evidence that completed snowball outperforms abandoned avalanche by $10,000+ demonstrating ongoing education gap between theoretical finance and practical behavioral implementation.

Fundamental snowball principles remain timeless: quick wins within 3-6 months create motivation maintaining 24-36 month commitment, smallest-first approach prioritizes psychology over mathematics accepting modest interest premium, increasing payment amounts through rolled balances provide tangible acceleration reinforcing progress, and behavioral approach optimizing human factors produces superior completion rates versus purely mathematical methods—regardless of social media proliferation, community tool development, method debate intensity, or advisor acknowledgment evolution, understanding smallest-first psychology and accepting deliberate interest premium as execution insurance produces superior real-world outcomes through completion versus theoretical optimization abandoned halfway impossible without behavioral finance literacy recognizing human motivation factors determining success probability.

3 Things You Can Do Today

Ready to implement debt snowball method? Here are three simple steps you can take right now:

1. Create complete debt inventory ranked smallest to largest balance establishing attack order and baseline – List every debt: Credit cards, auto loans, student loans, personal loans, medical debt, everything owed. For each record: Creditor name, current balance (exact amount to penny), interest rate APR, minimum monthly payment, payment due date. Rank list: Smallest balance to largest (ignore interest rates completely in ranking). Example list: Store card $685, Credit card A $1,850, Credit card B $4,200, Auto loan $7,500, Student loan $12,400. Calculate totals: Sum all balances ($26,635 example), sum all minimum payments ($685 example). Identify attack debt: Smallest balance (store card $685 in example) becomes primary target receiving all extra payment beyond minimums. Write attack commitment: “Attack debt: [Creditor name] $[amount]. Will pay $[amount] monthly until eliminated in approximately [months] months.” Visual organization: Create spreadsheet or handwritten chart posting visibly (refrigerator, bathroom mirror) creating constant reminder and motivation. Takes 20 minutes creating foundational document driving entire elimination strategy impossible without complete organized inventory ranked by balance establishing clear systematic approach versus random ad-hoc payments lacking strategic direction.

2. Calculate total available monthly payment combining minimums plus extra from budget cuts or income creating aggressive attack amount – Sum minimum payments: Add all required minimums from inventory (example: $685 total). Analyze discretionary spending: Review last 3 months identifying cuts (dining out $200, entertainment $120, subscriptions $80, shopping $150 = $550 potential monthly cuts). Identify income opportunities: Side gig potential (DoorDash, freelance, overtime) = $400-800 monthly realistic, selling items one-time boost applied to attack debt = $500-2,000. Calculate total capacity: Required minimums + budget cuts + side income = total debt elimination firepower (example: $685 minimums + $400 cuts + $600 side gig = $1,685 total monthly). Determine extra amount: Total capacity minus minimums = extra attacking smallest debt (example: $1,685 – $685 minimums = $1,000 extra to attack debt). Calculate first victory timeline: Attack debt balance ÷ extra payment = months to first elimination (example: $685 ÷ $1,000 = 1 month = immediate victory!). Write payment commitment: “Total available: $[amount] monthly. $[minimums] to non-attack debts, $[extra] attacking [smallest debt]. First victory: [date/month].” Reality check: If extra amount insufficient creating 12+ month first victory, increase cuts or income further creating 3-6 month timeline optimal for momentum. Takes 30 minutes establishing payment capacity creating concrete monthly allocation impossible when vaguely “paying extra” without specific calculated amounts driving systematic execution.

3. Set up payment automation and tracking creating systematic execution and visible progress monitoring – Automate minimum payments: Set up automatic payments for all non-attack debts at minimum amounts preventing missed payments while focusing energy on attack debt, schedule day after payday ensuring funds available. Attack debt payment: Set calendar reminder 1st of month “Pay $[extra amount] to [attack debt]” creating manual flexibility increasing amounts when possible, alternatively automate if amount consistent. Progress tracking setup: Create simple spreadsheet with columns (Date, Debt Name, Balance, Payment, New Balance, Notes), update monthly after payments showing balance reduction, or use debt tracking app (Debt Payoff Planner, Undebt.it) automating calculations. Visual progress chart: Print thermometer or bar chart showing total debt with sections for each individual debt, color in sections as paid creating visual shrinking representation posting prominently. Celebration planning: Mark calendar with predicted first debt elimination date, plan small celebration ($25-50 dinner or activity), schedule victory photo cutting up paid card posting to accountability community or social media if comfortable. First month execution: Make all minimum payments, make attack debt extra payment, update tracking showing first month’s progress, review visible chart seeing initial reduction. Takes 1 hour establishing systematic execution infrastructure transforming vague debt elimination intention into concrete automated approach with visible progress monitoring creating accountability and motivation impossible when relying on memory and ad-hoc payments without systematic tracking and celebration planning.

These actions create debt snowball implementation foundation within 2 hours—complete debt inventory ranked smallest to largest establishing clear attack order ($685 first, then $1,850, etc.), calculated total available payment determining aggressive attack amount ($1,000 extra monthly example creating 1-month first victory), and established payment automation plus tracking infrastructure ensuring systematic execution with visible progress monitoring—transforming debt snowball from conceptual method into concrete actionable plan with specific monthly payments and predicted victory timeline impossible without organized inventory, calculated payment capacity, and systematic execution infrastructure enabling momentum-building quick wins through smallest-first behavioral approach.

Quick FAQ

What is debt snowball method exactly?

Debt elimination strategy attacking smallest balance first regardless of interest rate creating quick psychological wins maintaining long-term commitment: Core mechanics—List all debts smallest to largest balance (ignore APRs), pay minimum on all except smallest, apply all extra payment to smallest balance, when eliminated roll entire payment to next smallest creating accelerating “snowball effect” through increasing payment amounts as debts disappear. Example: $800, $2,500, $5,000, $8,000 balances, $800 total available monthly = Attack $800 first (paid month 1-2), roll $150 freed minimum to $2,500 creating $350 monthly (paid months 3-9), roll $350 to $5,000 creating $500 monthly (paid months 10-20), roll $500 to $8,000 creating $800 monthly (paid months 21-32), debt-free in 32 months. Key principle: Prioritizes psychology over mathematics accepting modest interest premium ($500-1,000 typical on $15,000 total debt) ensuring completion through motivation maintenance versus mathematical optimization (avalanche) risking abandonment. Named “snowball” because payment amounts and momentum accelerate like snowball rolling downhill gaining mass and speed through each victory. Popularized by Dave Ramsey emphasizing behavioral approach recognizing human motivation factors more important than pure mathematics for successful debt elimination in real-world execution versus theoretical optimization.

Is snowball or avalanche better for paying off debt?

Depends on personality: Snowball better for psychology-driven individuals needing quick wins, avalanche better for disciplined number-focused personalities comfortable delayed gratification: Snowball advantages—First victory 3-6 months creating motivation surge, multiple celebrations throughout journey, accepts $500-1,000 extra interest as execution insurance, proven higher completion rates for average individuals, best when interest rates relatively similar (all 15-25% range). Avalanche advantages—Minimizes total interest mathematically (saves $500-1,000 typical), faster overall timeline (2-4 months typically), best for disciplined individuals motivated by optimization, critical when large rate gaps (24% card versus 4% loan makes avalanche clearly superior). Real-world data: Snowball users complete elimination 80%+ rate, avalanche users complete 60-70% rate due to discouragement from delayed first victory requiring 12+ months without tangible progress creating abandonment risk. Example comparison: $15,000 total debt, $800 monthly, snowball = 24 months $16,200 total paid, avalanche = 22 months $15,850 total (saves $350 and 2 months). Decision framework: Choose snowball if history of giving up on goals, need visible progress maintaining motivation, multiple small balances under $2,000 enabling rapid victories, emotionally-driven decision maker. Choose avalanche if highly disciplined, motivated by numbers and optimization, comfortable waiting 12+ months for first win, significant rate gaps justifying mathematical approach. Hybrid option: Snowball first small balance under $1,000 for immediate win, then switch to avalanche remaining debts combining psychological boost with mathematical efficiency. Key insight: EITHER method vastly superior to minimum-only perpetuation—method selection personal preference optimizing execution probability not universal superiority declaration, making primary goal aggressive payment amount and commitment not perfecting method choice.

How much extra should I pay to make snowball work?

Target 50-100% increase above minimums creating 18-36 month total elimination timeline with 3-6 month first victories: Minimum threshold—At least 20-30% above minimums creating meaningful progress (example: $500 minimums, add $100-150 extra = $600-650 total making 3-4 year timeline versus 10+ years minimums only). Optimal range—50-100% increase creating 2-3 year elimination with rapid early victories (example: $500 minimums, add $250-500 extra = $750-1,000 total making 24-36 months debt-free with first win 3-6 months). Aggressive approach—100%+ increase creating 12-24 month elimination through intense temporary sacrifice (example: $500 minimums, add $500-1,000 through spending freeze and side income = $1,000-1,500 total making 18 months debt-free). First victory consideration: Extra payment should eliminate smallest debt within 6 months maximum maintaining momentum (smallest balance $1,200, need $200+ extra monthly for 6-month victory, $400 extra for 3-month victory). Calculation: Determine total debt ÷ 36 months = target monthly payment creating 3-year timeline (example: $18,000 ÷ 36 = $500 monthly minimum target), if minimums already $400, need only $100 extra achieving goal, if minimums $200, need $300 extra. Reality: Most carrying $10,000-20,000 debt can eliminate in 24-36 months with $500-800 total monthly through combination of current minimums ($300-400) plus budget cuts ($100-200) plus side income ($200-400) making aggressive elimination achievable not requiring dramatic income increases when budget optimized and temporary side gig added. Key: Extra amount more important than method choice—$600 extra monthly on wrong method outperforms $100 extra on optimal method making payment magnitude driving success not perfected strategy selection.

What if my smallest debt is low interest and largest is high interest?

Stay committed to snowball smallest-first or switch to avalanche if rate gap extreme (over 15% difference), accepting trade-off explicitly: Snowball commitment argument—Quick win from small debt creates motivation maintaining 2-3 year journey, interest difference usually modest ($300-800 on typical scenario not $5,000), behavioral benefit outweighs mathematical cost, method consistency more important than mid-stream optimization. Example scenario: $1,000 at 6% (auto) versus $5,000 at 21% (credit card), snowball attacks $1,000 first despite low rate. Cost analysis: Paying $1,000 at 6% while carrying $5,000 at 21% for additional 3 months versus attacking $5,000 first = approximately $200 extra interest (modest premium for quick psychological win). Avalanche switch consideration: If rate gap extreme AND smallest balance requires 12+ months elimination creating delayed victory anyway, switch to avalanche makes sense (example: $8,000 smallest at 4% requiring 16 months versus $6,000 at 26% attacked in 10 months = avalanche clearly superior both mathematically and psychologically). Hybrid solution: Attack smallest regardless of rate if eliminates within 6 months (quick win valuable), then evaluate remaining debts switching to avalanche if rate gaps significant. Decision framework: Stay snowball if smallest debt eliminated within 3-6 months (quick win worth interest premium), switch to avalanche if smallest requires 12+ months anyway (losing psychological benefit making mathematical optimization preferable). Key principle: Snowball’s value comes from quick victories within 3-6 months creating momentum—if first victory delayed 12+ months anyway due to balance size, psychological benefit lost making avalanche superior, but if smallest balance small enough for rapid elimination regardless of rate, quick win maintains method value despite interest premium.

Should I save emergency fund before starting debt snowball?

Yes—build $1,000 starter emergency fund BEFORE aggressive debt attack preventing new debt from unexpected expenses: Starter fund priority—Pause aggressive debt elimination, save $1,000 as quickly as possible ($200-400 monthly reaches $1,000 in 3-5 months), store in separate savings account accessible but not daily checking, provides buffer for car repairs, minor medical, appliance replacement, prevents reactive credit card usage restarting debt cycle. Why starter fund essential: $1,000 prevents 80%+ of emergency credit card usage, unexpected $800 car repair with fund = use savings and replenish over 2-3 months versus on credit card at 20% APR costing $900+ over 12 months, minor setbacks don’t derail debt elimination maintaining momentum, psychological security reducing stress about “what if” scenarios. Snowball sequence: (1) Stop ALL debt payments except minimums, (2) save $1,000 starter fund as fast as possible, (3) once $1,000 saved resume aggressive debt snowball, (4) after debt-free expand fund to 3-6 months expenses. Common mistake: Skipping starter fund attacking debt immediately creating vulnerability forcing new credit card debt when emergencies arise negating progress. Alternative opinion: Some advocate zero savings attacking debt with “gazelle intensity” arguing debt emergency bigger than potential unexpected expense, but practical experience shows emergencies DO occur during 24-36 month elimination making $1,000 buffer worthwhile preventing setbacks. Full emergency fund timing: Do NOT save full 3-6 months expenses before debt elimination (would delay debt attack years), $1,000 sufficient during elimination phase, expand to full reserve after debt-free when can redirect entire debt payment amount to savings building full fund in 6-12 months. Exception: If already have $1,000+ saved, maintain it and start snowball immediately, if have $5,000 saved use $4,000 attacking debt keeping $1,000 buffer creating head start on elimination.

Explore More in Money Basics

Disclosure

This article provides general educational information about debt snowball method and debt elimination strategies. Individual debt situations, appropriate methods, payoff timelines, and interest costs vary significantly based on circumstances including total debt, income, expenses, interest rates, and individual psychology. This is not financial advice or recommendation that debt snowball method optimal for all situations. “Debt snowball” and associated strategies represent one approach among multiple valid debt elimination methods. Interest cost comparisons between snowball and avalanche methods represent typical scenarios—actual differences vary based on specific debt compositions and interest rates. Completion rate statistics represent general observations not scientific controlled studies. Behavioral finance principles supporting snowball method based on psychological research but individual motivation factors vary widely. Some individuals may achieve better outcomes with debt avalanche, hybrid approaches, or other strategies depending on personality and circumstances. Timeline projections assume consistent payments without interruption—actual elimination periods vary based on income stability, emergency disruptions, and commitment maintenance. Side income and spending reduction estimates represent potential ranges not guarantees—actual results depend on individual effort, skills, and market conditions. Emergency fund recommendations represent general guidelines—appropriate amounts vary by individual risk factors and circumstances. Celebration and reward suggestions should be scaled appropriately to individual budgets avoiding excessive spending. Method switching or hybrid approaches require careful evaluation—consistency generally preferable to frequent strategy changes. Consult qualified financial professionals, credit counselors, or debt advisors for personalized guidance matching individual situations and psychological profiles. Focus on sustainable long-term behavior changes alongside debt elimination preventing future cycles. Advertisements or sponsored content may appear within or alongside this content. All information presented independently for educational purposes only.