Time value of money is the financial principle stating that money available now is worth more than the same amount in the future due to its earning potential—$1,000 today can be invested to grow into $2,000+ over a decade while $1,000 received in ten years remains static, making present money more valuable. Unlike treating all dollars equally regardless of when received, time value of money recognizes that money can earn returns through investment, inflation erodes purchasing power over time, and earlier access to funds provides flexibility and opportunity unavailable with delayed receipt.

This article is designed for anyone making financial decisions involving time, individuals evaluating investment opportunities, or those planning retirement and long-term financial goals. You do not need mathematics expertise, finance degrees, or complex calculations to understand time value of money—grasping this fundamental concept transforms how you view savings, debt, investment timing, and major life decisions involving money and time trade-offs.

Understanding time value of money matters because starting retirement savings at 25 versus 35 creates hundreds of thousands in wealth difference through compound growth, paying extra on mortgages saves tens of thousands in interest through time value principles, and ignoring time value leads to poor financial decisions undervaluing future outcomes or overvaluing present consumption—yet most people make financial choices without considering how time affects money’s worth.

Educational disclaimer: This article provides general educational information about time value of money concepts. Calculations use simplified assumptions—actual investment returns vary and are not guaranteed. Individual circumstances differ significantly. This is not financial, investment, or tax advice. Consult qualified financial professionals for personalized guidance based on specific situations.

Understanding Time Value of Money

The Core Principle

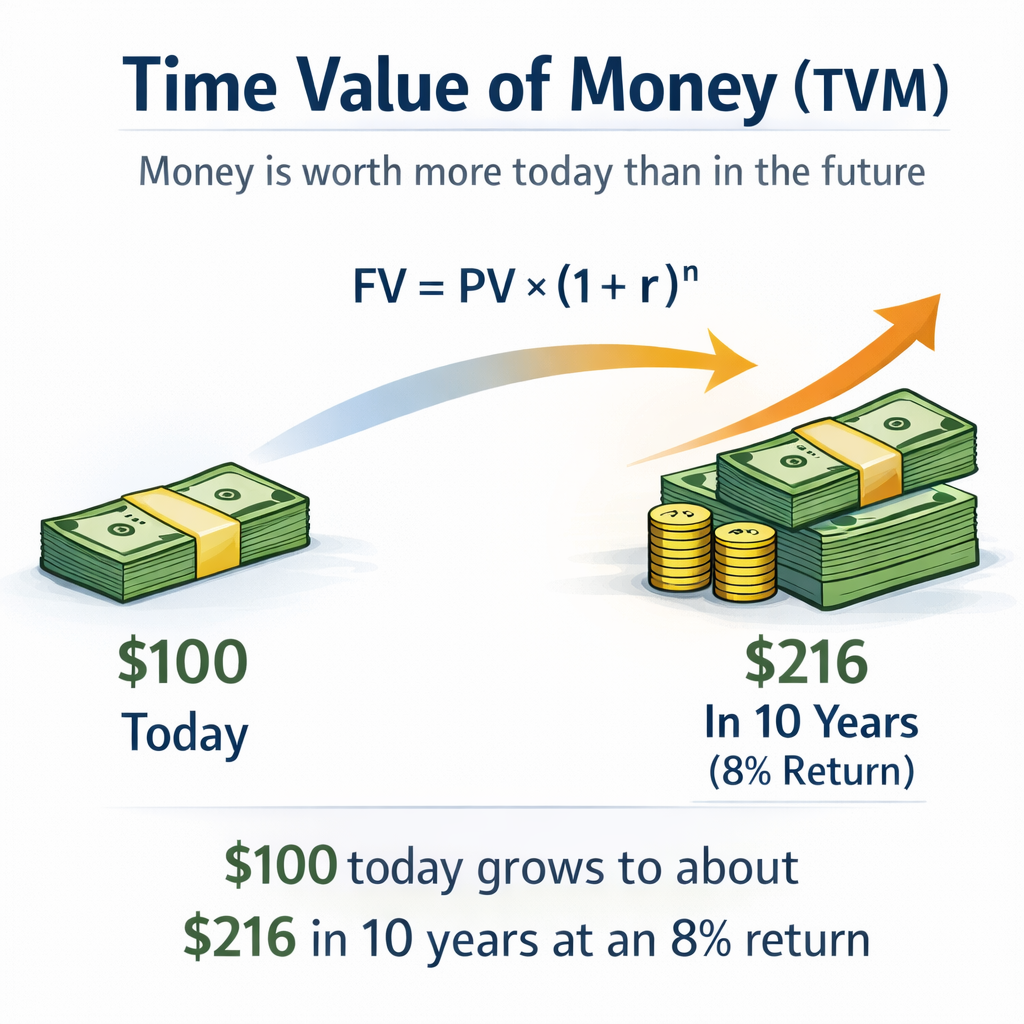

Fundamental concept: A dollar today is worth more than a dollar tomorrow

Three reasons why:

1. Earning potential (opportunity to invest):

- Money received today can be invested immediately

- Investments generate returns (interest, dividends, appreciation)

- Earlier investment means longer compounding period

- $1,000 today invested at 8% becomes $2,159 in 10 years

- $1,000 received in 10 years remains $1,000

2. Inflation (purchasing power erosion):

- Prices increase over time

- Same dollars buy less in future

- 3% annual inflation means $1,000 today buys what $744 buys in 10 years

- Future money worth less in real purchasing power

3. Risk and uncertainty:

- Future payment involves uncertainty

- Circumstances change (bankruptcy, death, default)

- Money in hand eliminates future receipt risk

- Guaranteed present value preferred over uncertain future value

Present Value vs Future Value

Present Value (PV):

- Current worth of future money

- Discounts future amounts to today’s equivalent

- Question: “How much is $1,000 in 10 years worth today?”

- Answer depends on discount rate (opportunity cost of capital)

Future Value (FV):

- Amount current money will grow to over time

- Projects today’s amounts to future equivalent

- Question: “How much will $1,000 today be worth in 10 years?”

- Answer depends on investment return rate

The relationship:

- Present and future values are reciprocals through time and interest rates

- Higher interest rates = lower present values of future money

- Longer time periods = lower present values, higher future values

Simple Example

Scenario: Win $1,000 today or $1,100 in one year?

Analysis:

- If you can invest at 8% annual return:

- $1,000 today grows to $1,080 in one year

- $1,100 in one year worth $1,019 today (discounting at 8%)

- Decision: Take $1,100 in one year (better value)

If you can invest at 12% annual return:

- $1,000 today grows to $1,120 in one year

- $1,100 in one year worth $982 today (discounting at 12%)

- Decision: Take $1,000 today (better value)

Key insight: Time value calculations depend on your opportunity cost (what you could earn on money)

Compound Interest: Time Value’s Power

What Is Compound Interest?

Definition: Earning returns on both initial investment and accumulated returns

Simple interest vs compound interest:

Simple interest (rare in practice):

- Earn only on initial principal

- $1,000 at 8% simple: Earn $80 annually forever

- 10 years: $1,000 + ($80 × 10) = $1,800

Compound interest (standard for investments):

- Earn on principal plus accumulated interest

- $1,000 at 8% compound: Earn $80 year 1, $86.40 year 2, $93.31 year 3, etc.

- 10 years: $2,159

- Difference: $359 additional through compounding

The Rule of 72

Quick estimation tool: How long to double money at given return rate

Formula: Years to double = 72 ÷ Annual return rate

Examples:

- 6% return: 72 ÷ 6 = 12 years to double

- 8% return: 72 ÷ 8 = 9 years to double

- 10% return: 72 ÷ 10 = 7.2 years to double

- 12% return: 72 ÷ 12 = 6 years to double

Application: $10,000 invested at 8% doubles every 9 years: $20K (year 9), $40K (year 18), $80K (year 27), $160K (year 36)

Compound Growth Examples

$10,000 invested at different rates over time:

At 6% annual return:

- 10 years: $17,908

- 20 years: $32,071

- 30 years: $57,435

- 40 years: $102,857

At 8% annual return:

- 10 years: $21,589

- 20 years: $46,610

- 30 years: $100,627

- 40 years: $217,245

At 10% annual return:

- 10 years: $25,937

- 20 years: $67,275

- 30 years: $174,494

- 40 years: $452,593

Key observation: Small return rate differences create enormous long-term value differences through compounding

Monthly Contributions Amplify Growth

$500 monthly investment at 8% annual return:

- 10 years: $91,473 (contributed $60,000, earned $31,473)

- 20 years: $294,510 (contributed $120,000, earned $174,510)

- 30 years: $745,180 (contributed $180,000, earned $565,180)

- 40 years: $1,745,503 (contributed $240,000, earned $1,505,503)

Insight: Contributions of $240,000 over 40 years grow to $1.7+ million through time value and compounding—more than 7x return

Starting Early: The Ultimate Time Value Advantage

Scenario: $500 monthly at 8% return

Starting at age 25, saving until 65 (40 years):

- Total contributions: $240,000

- Account value at 65: $1,745,503

Starting at age 35, saving until 65 (30 years):

- Total contributions: $180,000

- Account value at 65: $745,180

Cost of 10-year delay:

- Contributed $60,000 less

- Account value $1,000,000+ less

- 10-year delay cost: $1 million in lost wealth

Starting at age 45, saving until 65 (20 years):

- Total contributions: $120,000

- Account value at 65: $294,510

Cost of 20-year delay:

- Contributed $120,000 less

- Account value $1,450,000+ less

- 20-year delay cost: $1.45 million in lost wealth

Critical lesson: Starting early is most powerful wealth-building tool through time value of money

Practical Applications

Retirement Planning

Question: How much to save for retirement?

Time value analysis:

- Need $50,000 annually in retirement (today’s dollars)

- Retire at 65, life expectancy 90 (25 years retirement)

- 4% withdrawal rule suggests need $1.25 million ($50K ÷ 4%)

- Currently age 30 (35 years to retirement)

- Expected 8% annual return

Options:

- Lump sum today: $86,200 grows to $1.25M in 35 years

- Monthly contributions: $430 monthly grows to $1.25M in 35 years

- Wait 10 years, start at 40: $1,034 monthly required (2.4x more per month)

Insight: Earlier start requires dramatically less monthly contribution due to time value

Debt Payoff Decisions

Scenario: $10,000 windfall—invest or pay extra on mortgage?

Option A: Pay extra on 4% mortgage

- Saves 4% interest guaranteed

- $10,000 payment reduces interest by ~$6,500 over 15 remaining years

- Equivalent to 4% guaranteed return

Option B: Invest in stock market (expected 8% return)

- $10,000 grows to $31,722 in 15 years at 8%

- Gain after mortgage savings: $31,722 – $16,500 = $15,222 advantage to investing

Decision framework:

- Debt interest rate < expected investment return: Invest instead of extra payments

- Debt interest rate > expected investment return: Pay debt instead

- Consider risk tolerance and guaranteed vs uncertain returns

Large Purchase Timing

Scenario: Buy $30,000 car now or wait 3 years?

Option A: Buy now with loan

- $30,000 at 6% for 5 years

- Monthly payment: $580

- Total paid: $34,800

- Interest cost: $4,800

Option B: Save and buy in 3 years

- Invest $500 monthly for 36 months at 8% return

- Accumulate: $20,097

- Need additional $9,903 to buy $30,000 car

- If car depreciates to $24,000 by year 3, only need $3,903 additional

Time value insight: Delaying purchase while saving produces better outcome through investment returns and depreciation

Education Funding

Child born today, college in 18 years

- Current college cost: $100,000 total

- Projected cost in 18 years (5% annual increase): $241,000

Saving strategies:

Start immediately:

- $445 monthly at 8% return = $241,000 in 18 years

Wait 10 years:

- $1,473 monthly at 8% return = $241,000 in 8 years

- 3.3x more per month required

Time value advantage: Early start reduces monthly burden dramatically

Salary Negotiation and Career Decisions

Scenario: Job A offers $70,000, Job B offers $75,000

Simple view: $5,000 annual difference

Time value view (30-year career):

- $5,000 difference annually

- Assume 3% annual raises on base salary

- Total additional earnings over 30 years: $238,000+

- If investing 10% of difference: $23,800 invested

- $23,800 growing at 8% over 30 years: $239,000

Insight: $5,000 salary difference compounds to ~$500,000 additional lifetime value through time value of money

Common Time Value Mistakes

Delaying Retirement Savings

Mistake: “I’ll start saving seriously in my 40s when I earn more”

Cost: Missing decades of compound growth—10-year delay costs $1+ million in lost wealth

Solution: Start immediately even with small amounts. $100 monthly starting at 25 beats $500 monthly starting at 45

Ignoring Inflation in Long-Term Planning

Mistake: Planning to retire on $50,000 annually without adjusting for inflation

Cost: $50,000 in 30 years buys what ~$21,000 buys today at 3% inflation

Solution: Plan retirement needs in today’s dollars but project future costs with inflation

Paying Only Minimum on High-Interest Debt

Mistake: Minimum payments on 20% APR credit card while money sits in 1% savings

Cost: Losing 19% annually (20% debt cost minus 1% savings return)

Solution: Accelerate high-interest debt payoff—guaranteed 20% “return” beats uncertain investment returns

Keeping Emergency Fund Too Large

Mistake: $50,000 emergency fund earning 1% when only need $15,000

Cost: $35,000 not invested at 8% = $75,000 in 10 years, $240,000 in 20 years

Solution: Right-size emergency fund (3-6 months expenses), invest excess

Lifestyle Inflation Preventing Investment

Mistake: Spending every raise instead of increasing savings

Cost: $5,000 annual raise spent vs invested at 8% = $575,000 over 30 years

Solution: Direct 50-100% of raises to savings and investment before lifestyle adjusts

Analysis Paralysis Delaying Investment

Mistake: Waiting for “perfect” market timing or investment selection

Cost: Every year delayed waiting costs 8%+ growth plus compounds over remaining years

Solution: Start immediately with simple index funds. Imperfect action beats perfect planning.

Time Value Formulas (Simplified)

Future Value of Lump Sum

Formula: FV = PV × (1 + r)^n

- FV = Future Value

- PV = Present Value (amount today)

- r = Annual interest rate (as decimal)

- n = Number of years

Example: $10,000 at 8% for 10 years

- FV = $10,000 × (1.08)^10

- FV = $10,000 × 2.159

- FV = $21,590

Present Value of Future Sum

Formula: PV = FV ÷ (1 + r)^n

Example: $50,000 in 20 years, discounted at 8%

- PV = $50,000 ÷ (1.08)^20

- PV = $50,000 ÷ 4.661

- PV = $10,727

Interpretation: $50,000 in 20 years equals $10,727 today at 8% discount rate

Note on Calculations

While formulas provide precision, understanding concepts matters more than calculations. Online calculators and financial tools handle complex math. Focus on principles: time multiplies money through compound growth, earlier investment beats later investment, and small rate differences create enormous long-term value differences.

Why Time Value of Money Matters

Without understanding time value of money, people delay retirement savings costing hundreds of thousands in lost compound growth, ignore investment opportunities while keeping cash in low-return accounts, and make poor financial decisions treating present and future money as equivalent when time dramatically affects value—while those understanding time value strategically position investments maximizing compounding periods and returns.

Understanding time value of money enables individuals to:

- Start investing early maximizing compound growth benefits

- Make informed decisions comparing present and future values

- Evaluate debt payoff versus investment alternatives rationally

- Plan retirement and long-term goals with realistic projections

- Negotiate salaries understanding lifetime value implications

- Allocate resources strategically to highest time-adjusted returns

Time value awareness transforms financial decision-making from short-term focus to long-term wealth optimization through strategic timing and compounding.

Common Misunderstandings

Many people assume time value of money only matters for large sums or wealthy individuals. In reality, time value affects all financial decisions regardless of amount—$50 monthly invested over 40 years creates more wealth than $500 monthly invested over 10 years through time value principles, proving timing matters more than amount for building wealth.

Another common misconception is that waiting to invest until you “have enough money” is prudent. In practice, delaying investment while accumulating lump sum costs more through lost compound growth than starting immediately with small regular contributions—time in market beats timing market, and earlier small investments compound into larger values than later large investments.

Some believe time value calculations are too complex for practical use. However, understanding basic principles—money grows over time, earlier investment beats later investment, compound growth accelerates with time—enables better financial decisions without mathematical expertise. Simple awareness of time value transforms decision quality dramatically without requiring precise calculations.

How Time Value Fits Into Financial Success

Time value of money provides mathematical foundation explaining why starting retirement savings early matters more than contribution amounts, why carrying high-interest debt destroys wealth systematically, and why delaying financial decisions costs exponentially more than immediate action—creating framework for evaluating all financial choices involving time dimensions.

For example, two people commit to saving $100,000 for retirement. Person A starts at 25 investing $200 monthly at 8% return, reaching $100,000 by age 44 (19 years). Continues until 65 accumulating $351,428 total. Person B waits until 35, needs $380 monthly to reach $100,000 by age 54 (19 years, same timeframe). Continues until 65 accumulating only $265,180 total. Both “saved” for 19 years but Person A started 10 years earlier, resulting in $86,248 additional wealth ($351,428 vs $265,180) despite identical saving periods. Time value advantage from earlier start created $86,000+ difference through compound growth—decade of time worth nearly as much as two decades of contributions through time value principles.

Time value understanding transforms “I’ll start later” into “I must start now” enabling wealth accumulation impossible through procrastination.

Recent Updates and Trends

In recent years, inflation has increased highlighting time value importance—money losing purchasing power at 3-8% annually makes time value considerations more critical for maintaining real wealth versus nominal values.

Compound interest calculators and visualization tools have made time value concepts more accessible—interactive tools showing growth curves and comparing scenarios make abstract principles concrete and emotionally resonant.

Low interest rates on savings (1-2%) versus historical market returns (8-10%) have widened opportunity cost of holding excess cash, making time value optimization through proper investment more valuable.

Retirement age uncertainty and longevity increases have lengthened required investment timeframes—30-40 year horizons make time value of early investment even more dramatic through extended compound periods.

Fundamental time value principles remain timeless: money can earn returns making present money more valuable than future money, compound growth accelerates over time making early investment disproportionately powerful, and inflation erodes purchasing power making future money worth less in real terms—understanding time value enables strategic positioning maximizing wealth accumulation regardless of market conditions or economic environment.

3 Things You Can Do Today

Ready to apply time value of money? Here are three simple steps you can take right now:

1. Calculate your retirement savings trajectory – Use free compound interest calculator (search “compound interest calculator”). Input: current savings, monthly contribution, years until retirement, expected 8% return. Compare result to retirement needs. If insufficient, calculate what monthly contribution reaches goal. This visualization makes time value concrete—seeing $500 monthly grow to $1+ million over 35 years transforms abstract concept into motivating reality.

2. Start or increase retirement contribution today—even $50 monthly – If not contributing to retirement account, start with minimum amount today (even $50-100 monthly). If already contributing, increase by $50-100 monthly. $50 monthly at 8% over 30 years = $75,000. Small amounts matter through time value—starting today is more valuable than waiting to contribute larger amounts later. Time in market beats timing market.

3. Calculate time value cost of one current expense – Choose one regular expense: $150 monthly subscription, $200 dining out, $100 shopping. Calculate 30-year future value at 8% if invested instead (use calculator from step 1). Example: $150 monthly = $224,000 in 30 years. Seeing this single expense’s opportunity cost makes time value personal and actionable. May or may not change spending choice, but creates awareness enabling conscious decisions.

These actions transform abstract time value concepts into personal financial decisions improving wealth accumulation through compound awareness and strategic timing.

Quick FAQ

What’s more important: how much I save or when I start?

When you start matters more initially. $200 monthly from 25-65 (40 years) at 8% = $622,000. $400 monthly from 45-65 (20 years) at 8% = $246,000. Half the monthly amount for double the time creates 2.5x more wealth through time value. However, both timing AND amount matter—ideal: start early AND save aggressively.

Should I pay off low-interest debt or invest?

Compare debt interest rate to expected investment return. Debt under 5%: Generally invest instead (expected 8%+ market return). Debt 5-7%: Personal preference balancing guaranteed return (debt payoff) versus potential return (investment). Debt over 8%: Pay off before investing—guaranteed return exceeds uncertain investment returns. Consider risk tolerance and behavior—some prefer debt-free peace of mind.

How do I account for inflation in time value calculations?

Use “real return” instead of nominal return. Real return = nominal return – inflation rate. Example: 8% investment return minus 3% inflation = 5% real return. Plan retirement needs in today’s dollars for mental clarity, then calculate using real returns. Alternatively, project future costs with inflation then calculate needed savings with nominal returns.

Is it ever too late to start investing?

Never too late—time value still works over any period. Starting at 50 with 15 years to 65: $1,000 monthly at 8% = $348,000. Not millions but substantial. Also, retirement may last 20-30 years providing additional time for growth. Best time to start was 20 years ago; second best time is today. Every year delayed reduces final wealth—start immediately regardless of age.

What return rate should I use in time value calculations?

Conservative planning: 6-7% (below historical 8-10% stock market average). Moderate: 8% (historical long-term stock average). Aggressive: 9-10% (optimistic). Bonds: 3-5%. Savings accounts: 1-4%. Use conservative estimates for critical goals like retirement. Actual returns vary—estimates provide planning framework, not guarantees. Adjust plans as actual results differ from projections.

How does time value of money relate to opportunity cost?

Time value is specific type of opportunity cost—money spent today costs not just the amount but also the investment returns forgone. Spending $1,000 costs $1,000 plus $9,000 it could have grown to in 30 years at 8% = $10,000 total opportunity cost. Time value quantifies opportunity cost of consumption versus investment through compound growth calculations.

Explore More in Money Basics

Disclosure

This article is provided for educational purposes only and does not constitute financial, investment, or tax advice. Time value calculations use simplified assumptions and hypothetical examples—actual investment returns vary significantly and are not guaranteed. Historical returns do not guarantee future performance. Individual circumstances differ based on age, risk tolerance, financial situation, and goals. Examples use assumed rates of return for illustration—actual returns may be higher or lower affecting outcomes substantially. Inflation rates vary and are unpredictable. Consult qualified financial professionals for personalized guidance considering specific situations, investment horizons, and risk tolerances. Information current as of publication but financial products, market conditions, and tax laws change. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.