Inflation and purchasing power represent inverse relationships describing how money’s value changes over time—inflation measures the rate prices increase annually, typically 2-3% in stable economies, while purchasing power describes how much goods and services money can buy, declining as inflation rises. Unlike assuming dollars maintain constant value, understanding inflation reveals that $100 today buys what $74 bought 10 years ago at 3% inflation, requiring strategic responses like investing for returns exceeding inflation, negotiating salary increases matching cost-of-living growth, and planning retirement needs accounting for decades of price increases eroding fixed savings.

This article is designed for anyone planning long-term finances, individuals on fixed incomes, or those seeking to preserve wealth over time. You do not need economics degrees, complex mathematics, or market expertise to understand inflation’s impact—simple awareness that money loses value over time through rising prices transforms financial planning from static to dynamic, from short-term to inflation-adjusted thinking spanning decades.

Understanding inflation and purchasing power matters because ignoring inflation costs retirees 30-50% of purchasing power over retirement decades, keeping savings in 1% accounts while inflation runs 3% guarantees 2% annual real loss compounding to 45% wealth erosion over 30 years, and failing to negotiate salary increases matching inflation creates effective pay cuts despite stable nominal income—yet many people make financial plans treating money as having constant value when reality proves otherwise.

Educational disclaimer: This article provides general educational information about inflation and purchasing power. Inflation rates vary by country, time period, and economic conditions. Examples use historical averages—actual rates differ. This is not financial, investment, or economic advice. Consult qualified financial professionals for personalized guidance.

Understanding Inflation

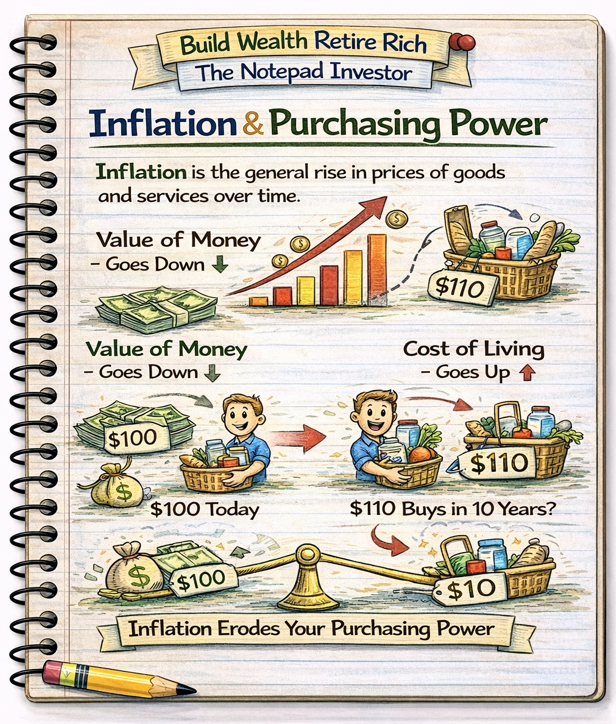

What Is Inflation?

Definition: The rate at which general price level of goods and services increases over time, eroding purchasing power

Simple explanation: Things cost more money each year—inflation measures how much more

Key characteristics:

- Expressed as annual percentage rate

- Normal feature of growing economies (2-3% typical target)

- Affects all prices though individual items vary

- Continuous process—prices generally don’t decrease

How Inflation Is Measured

Consumer Price Index (CPI):

- Most common inflation measure

- Tracks prices of basket of common consumer goods

- Includes: Housing, food, transportation, healthcare, education, etc.

- Updated monthly by Bureau of Labor Statistics

- Annual inflation = percentage change in CPI year-over-year

Core CPI (Core Inflation):

- CPI excluding volatile food and energy prices

- Provides clearer trend without temporary fluctuations

- Federal Reserve focuses on core inflation for policy

Personal Consumption Expenditures (PCE):

- Alternative inflation measure

- Broader than CPI, includes more services

- Federal Reserve’s preferred inflation metric

Historical Inflation Context

Recent U.S. inflation rates:

- 1960s-1970s: Average 4-5%, peaking at 13.5% (1980)

- 1980s-1990s: Declining from 10%+ to 2-3%

- 2000-2019: Stable 1.5-3% range

- 2020-2021: Pandemic-related volatility

- 2022-2023: 8%+ peak, returning toward 3-4%

- Long-term average (1926-2024): ~3% annually

Federal Reserve target: 2% annual inflation considered optimal for healthy economy

What Causes Inflation?

Demand-pull inflation:

- Too much money chasing too few goods

- High consumer demand exceeds supply capacity

- Example: Pandemic stimulus + supply chain disruptions

Cost-push inflation:

- Rising production costs (labor, materials, energy)

- Businesses pass costs to consumers through higher prices

- Example: Oil price shocks increasing transportation costs

Monetary inflation:

- Central bank increases money supply

- More currency in circulation reduces each dollar’s value

- Example: Quantitative easing programs

Built-in inflation (wage-price spiral):

- Workers demand higher wages to maintain purchasing power

- Higher wages increase production costs

- Businesses raise prices to cover costs

- Creates self-reinforcing cycle

Understanding Purchasing Power

What Is Purchasing Power?

Definition: The quantity of goods and services money can buy

Relationship to inflation: Purchasing power and inflation move inversely—as inflation rises, purchasing power falls

Formula: Real purchasing power = Nominal dollars ÷ (1 + inflation rate)^years

Purchasing Power Erosion Examples

$100 purchasing power at 3% annual inflation:

- Today: Buys $100 worth of goods

- 5 years: Buys $86 worth of goods (14% loss)

- 10 years: Buys $74 worth of goods (26% loss)

- 20 years: Buys $55 worth of goods (45% loss)

- 30 years: Buys $41 worth of goods (59% loss)

$50,000 annual income at 3% inflation:

- Without raises maintaining purchasing power:

- Year 10: Buying power equivalent to $37,000 today

- Year 20: Buying power equivalent to $27,500 today

- Year 30: Buying power equivalent to $20,500 today

Required income to maintain $50,000 purchasing power:

- Year 10: $67,196 needed

- Year 20: $90,306 needed

- Year 30: $121,363 needed

Real vs Nominal Values

Nominal value:

- Dollar amount not adjusted for inflation

- Face value or stated amount

- Example: $50,000 salary

Real value:

- Purchasing power adjusted for inflation

- Value in constant dollars (often using base year)

- Example: $50,000 salary in 2025 = $37,000 purchasing power in 2035 at 3% inflation

Critical insight: Focus on real values for long-term planning—nominal amounts mislead without inflation adjustment

Inflation’s Uneven Impact

Not all prices rise equally:

Above-average inflation sectors:

- Healthcare: 4-6% annually (exceeds general inflation)

- College tuition: 5-8% annually historically

- Housing in high-demand areas: 4-7%

Below-average inflation sectors:

- Technology products: Often deflation (better/cheaper over time)

- Clothing: Modest increases or stable

- Household goods: Generally lower than CPI

Implication: Personal inflation rate depends on spending composition—retirees with high healthcare costs experience higher personal inflation than young professionals with low healthcare needs

Inflation’s Impact on Financial Planning

Retirement Planning

Challenge: Retirement may span 20-30+ years—inflation dramatically affects needed savings

Example: Planning for $50,000 annual retirement income

Ignoring inflation (wrong approach):

- Assume need $50,000 annually for 30 years

- At 4% withdrawal rule: Need $1.25 million saved

Accounting for 3% inflation (correct approach):

- Year 1: $50,000

- Year 10: $65,227 needed for same purchasing power

- Year 20: $85,195 needed

- Year 30: $111,272 needed

- Average need over 30 years: ~$75,000 annually

- Actually need $1.875 million saved ($750,000 more than nominal calculation)

Critical lesson: Ignoring inflation in retirement planning creates 50%+ shortfalls

Savings and Cash Holdings

Scenario: $100,000 in savings account earning 1% annually with 3% inflation

10-year outcome:

- Nominal value: $110,462 (grew 10.5%)

- Real purchasing power: $82,035 in today’s dollars (lost 18%)

- Net result: Lost purchasing power despite nominal growth

Required return to maintain purchasing power:

- Must earn at minimum the inflation rate

- 3% inflation requires 3%+ investment returns

- Returns below inflation = guaranteed real losses

Implication: Cash and low-return savings accounts lose value over time—appropriate for emergency funds and short-term needs only, not long-term wealth building

Fixed Income and Pensions

Challenge: Fixed payments maintain nominal value but lose real value

Example: $3,000 monthly pension without cost-of-living adjustment (COLA)

Real purchasing power at 3% inflation:

- Year 1: $3,000 ($36,000 annually)

- Year 10: $2,228 real value ($26,736 annually)

- Year 20: $1,654 real value ($19,848 annually)

- Year 30: $1,228 real value ($14,736 annually)

30-year result: Nominal income stayed $36,000 but purchasing power declined to $14,736—59% loss

Solution: Seek pensions with COLA increases or supplement with inflation-protected investments

Debt Management

Inflation benefits borrowers with fixed-rate debt:

Example: $200,000 mortgage at 4% fixed, 30-year term

- Monthly payment: $955 (fixed nominally)

- Real cost of payment declines over time

- Year 1: $955 payment = $955 real cost

- Year 15 (at 3% inflation): $955 payment = $611 real cost

- Year 30: $955 payment = $392 real cost

Implication: Fixed-rate debt payments become easier over time as inflation erodes real cost—one reason mortgages are valuable

However: High inflation with low wages growth still makes payments difficult—inflation helps only if income keeps pace

Salary Negotiations

Maintaining purchasing power requires inflation-matching raises:

$60,000 salary with no raises, 3% annual inflation:

- Year 5: $51,674 real purchasing power (14% pay cut)

- Year 10: $44,523 real purchasing power (26% pay cut)

- Year 15: $38,357 real purchasing power (36% pay cut)

Required raises to maintain purchasing power:

- Annual 3% minimum just to stay even

- Real raises require exceeding inflation rate

- 5% raise with 3% inflation = 2% real increase

Protecting Against Inflation

Investment Strategies

1. Stocks (Historically best inflation hedge)

- Average 8-10% annual returns exceed typical 2-3% inflation

- Companies can raise prices maintaining profitability

- Long-term stock ownership preserves purchasing power

- Short-term volatility but long-term growth

2. Real Estate

- Property values generally rise with inflation

- Rental income increases with inflation

- Fixed-rate mortgages benefit from inflation

- Tangible asset with inherent value

3. Treasury Inflation-Protected Securities (TIPS)

- Principal adjusts with CPI inflation

- Interest payments rise as principal increases

- Guaranteed inflation protection

- Lower returns but explicit inflation hedge

4. I Bonds (Series I Savings Bonds)

- Interest rate adjusts every 6 months with inflation

- Safe, government-backed

- Tax advantages (defer federal tax, exempt from state/local)

- Purchase limits: $10,000 electronic + $5,000 paper annually

5. Commodities and Precious Metals

- Gold, silver, oil often rise with inflation

- Diversification benefit

- High volatility, no income generation

- Better as small portfolio allocation (5-10%)

Income Strategies

Negotiate regular raises:

- Minimum: Inflation-matching increases

- Goal: Inflation + merit raises (5-7% annually)

- Track personal performance justifying above-inflation increases

Develop inflation-resistant income sources:

- Skills and expertise that appreciate over time

- Business ownership with pricing power

- Royalties and passive income adjustable with inflation

Diversify income streams:

- Multiple sources reduce single-income risk

- Investment income supplements wage income

- Side businesses provide flexibility raising prices

Spending Strategies

Lock in long-term fixed costs when possible:

- Fixed-rate mortgages protect against housing inflation

- Long-term service contracts at fixed rates

- Prepay future expenses at current prices when advantageous

Prioritize inflation-sensitive expense reduction:

- Healthcare, housing, education have above-average inflation

- Reducing exposure protects against personal inflation rate

- Location choices significantly affect housing inflation exposure

Social Security Considerations

Automatic inflation protection:

- Social Security includes annual COLA (cost-of-living adjustment)

- Benefits increase with CPI inflation

- Maintains purchasing power automatically

- One reason Social Security valuable in retirement planning

Common Inflation Mistakes

Keeping Too Much Cash Long-Term

Mistake: Large emergency fund or savings sitting in low-yield accounts for years

Cost: 2% annual real loss (3% inflation minus 1% return) compounds to 45% purchasing power loss over 30 years

Solution: Right-size emergency fund (3-6 months), invest excess in inflation-beating assets

Ignoring Inflation in Retirement Planning

Mistake: Calculating retirement needs in today’s dollars without adjusting for future costs

Cost: 50%+ retirement savings shortfall

Solution: Plan retirement income needs increasing 3% annually, adjust savings targets accordingly

Accepting Nominal Salary Stability

Mistake: Staying at same salary year after year thinking you’re maintaining position

Cost: 3% annual real pay cut compounding to 26% loss over 10 years

Solution: Negotiate annual raises minimum matching inflation, change jobs if necessary

Fixed Annuities Without Inflation Protection

Mistake: Purchasing annuity with fixed payments thinking it provides lifetime security

Cost: Payments lose 40-60% purchasing power over 20-30 year retirement

Solution: Choose annuities with inflation riders or supplement with inflation-protected investments

Overweighting Bonds in Long Time Horizons

Mistake: Conservative bond-heavy portfolio decades before retirement

Cost: 3-4% bond returns barely exceed inflation, missing stock market’s 8-10% long-term returns

Solution: Match asset allocation to time horizon—stocks for 10+ year goals, bonds for near-term needs

Why Understanding Inflation and Purchasing Power Matters

Without understanding inflation, people plan retirements based on today’s costs discovering decades later their savings insufficient, keep emergency funds too large in low-return accounts losing purchasing power systematically, and accept stagnant salaries unaware they’re experiencing real pay cuts—while those accounting for inflation invest strategically, negotiate raises protecting purchasing power, and plan dynamically for inflation-adjusted futures.

Understanding inflation and purchasing power enables individuals to:

- Plan retirement needs accounting for decades of price increases

- Invest strategically for returns exceeding inflation preserving wealth

- Negotiate compensation maintaining and growing real purchasing power

- Make informed financial decisions in real rather than nominal terms

- Protect against systematic wealth erosion from holding cash long-term

- Structure debt and financial commitments advantageously relative to inflation

Inflation awareness transforms financial planning from static nominal thinking to dynamic purchasing power preservation spanning decades.

Common Misunderstandings

Many people assume inflation only affects prices but doesn’t impact their personal finances if income stays stable. In reality, stable nominal income with 3% annual inflation creates automatic 26% real pay cut over decade—inflation silently erodes purchasing power requiring active responses through raises, investments, or career advancement maintaining real living standards.

Another common misconception is that low inflation periods mean inflation doesn’t matter. In practice, even 2% annual inflation compounds to 49% purchasing power loss over 30 years—seemingly modest inflation rates create substantial long-term impacts requiring strategic responses regardless of whether inflation feels immediate or urgent.

Some believe investing is unnecessary because keeping money “safe” in savings accounts preserves value. However, 1-2% savings returns versus 3% inflation guarantees 1-2% annual real losses compounding to 26-45% wealth erosion over 20-30 years—safety from market volatility trades for guaranteed purchasing power destruction through inflation exceeding returns.

How Inflation Understanding Fits Into Financial Success

Inflation awareness provides framework distinguishing nominal changes from real changes, enabling proper evaluation of investments (returns must exceed inflation), compensation (raises must match or exceed inflation), and long-term planning (future needs grow with inflation)—separating those preserving wealth from those experiencing systematic purchasing power erosion despite appearing financially stable.

For example, two people earn $60,000 annually. Person A never considers inflation—keeps $50,000 emergency fund in savings earning 1%, never negotiates raises maintaining $60,000 salary for 15 years, plans retirement needing $40,000 annually in today’s dollars. Person B accounts for inflation—invests excess emergency fund beyond $20,000 earning 8%, negotiates 4-5% annual raises growing salary to $110,000 over 15 years, plans retirement needing $62,000 annually adjusted for inflation. After 15 years: Person A has $60,000 salary worth $39,000 in purchasing power (35% real decline), emergency fund worth $33,000 purchasing power (lost 34% real value), severely under-saved for retirement. Person B has $110,000 salary exceeding inflation maintaining purchasing power growth, investments growing ahead of inflation, realistic retirement planning. Same starting salary, different inflation awareness, dramatically different financial outcomes. Understanding purchasing power erosion enabled strategic responses preserving and growing real wealth.

Inflation understanding separates those building lasting wealth from those experiencing silent systematic value destruction despite nominal stability.

Recent Updates and Trends

In recent years, post-pandemic inflation spike reached 8%+ (2022) highlighting inflation’s impact—many people experienced inflation’s wealth erosion directly for first time in decades, increasing awareness and concern about purchasing power protection.

Remote work has changed geographic inflation impact—ability to work remotely from lower-cost areas enables escaping high-inflation housing markets, reducing personal inflation rates through location arbitrage.

Inflation-protected securities have gained popularity—TIPS and I Bonds seeing increased demand as investors seek explicit inflation hedges amid elevated inflation concerns.

Federal Reserve policy more transparent—regular communications about 2% inflation target and policy adjustments help individuals plan around expected inflation ranges.

Fundamental inflation principles remain timeless: prices generally rise over time eroding money’s purchasing power, returns must exceed inflation preserving real wealth, long-term planning requires inflation adjustment transforming nominal projections to purchasing power reality, and proactive strategies (investing, negotiating, diversifying) protect against systematic wealth erosion—regardless of whether current inflation runs 2% or 8%, understanding purchasing power dynamics enables appropriate strategic responses.

3 Things You Can Do Today

Ready to protect against inflation? Here are three simple steps you can take right now:

1. Calculate your real salary change over past 5-10 years – Find salary from 5 and 10 years ago. Use inflation calculator (search “inflation calculator”) to convert past salaries to today’s dollars. Compare to current salary. Example: $50,000 ten years ago = $67,196 today at 3% inflation. If current salary under $67,196, you’ve taken real pay cut. This reveals whether you’re maintaining, gaining, or losing purchasing power—awareness enables strategic career decisions.

2. Audit savings and cash holdings against inflation – Total all cash in savings accounts, checking, CDs earning under 3%. If over 6 months expenses, excess is losing purchasing power. Compare account interest rates to current inflation rate. Any accounts earning less than inflation are guaranteed losers. Action: Move excess beyond emergency fund to investments earning inflation-beating returns (stock index funds averaging 8-10% long-term). This protects purchasing power while maintaining adequate emergency reserves.

3. Recalculate one long-term financial goal with inflation – Choose major goal: retirement, home down payment, education fund. Calculate using today’s costs. Then recalculate using inflation-adjusted future costs: multiply by (1.03)^years for 3% inflation. Example: $50,000 needed in 20 years = $90,306 actual need. This reveals true target versus nominal planning—many people discover they’re saving for goals requiring 50-100% more than originally thought when properly accounting for inflation.

These actions create inflation awareness transforming nominal financial planning into purchasing power reality enabling strategic adjustments protecting and building real wealth.

Quick FAQ

What’s a “good” inflation rate?

Federal Reserve targets 2% annual inflation as optimal—high enough encouraging economic activity (people spend rather than hoarding cash) but low enough preserving purchasing power and preventing economic distortion. Under 2% risks deflation (prices falling, economically problematic). Over 4% creates uncertainty and rapid purchasing power erosion. 2-3% range considered healthy balance.

How much should my investments return to beat inflation?

Minimum: Match inflation rate (3%) preserving purchasing power. Better: Exceed inflation by 3-5% (6-8% total return) building real wealth. Stock market historical average ~8-10% provides ~5-7% real return above 3% inflation. Bonds ~3-5% barely beat inflation. Savings accounts ~1-2% lose to inflation. Target investments averaging 6-8%+ long-term.

Should I pay off my mortgage or invest during high inflation?

High inflation makes fixed-rate mortgages more attractive—payment’s real cost declines over time. If mortgage rate 4% and inflation 3%, real cost only 1%. Meanwhile, investments potentially return 8%+ nominal (5%+ real). Generally better to invest rather than accelerate low-rate mortgage payoff during inflation. Exception: Approaching retirement or uncomfortable with debt regardless of economics.

How does inflation affect Social Security?

Social Security includes automatic COLA (cost-of-living adjustment) increasing benefits annually with CPI inflation. This maintains purchasing power unlike fixed pensions or annuities. Makes Social Security particularly valuable in retirement—rare inflation-protected income source. However, COLA sometimes lags actual inflation or uses different calculation than CPI, creating modest erosion some years.

What if we experience deflation instead of inflation?

Deflation (falling prices) is economically problematic—people delay purchases expecting lower prices, reducing economic activity, causing recession. Also increases real burden of debt. Rarely occurs in modern economies—Japan 1990s-2000s and Great Depression are examples. Central banks actively prevent deflation through monetary policy. Focus planning on inflation since far more common and likely than sustained deflation.

How do I protect my retirement from inflation?

Multiple strategies: (1) Continue stock market exposure in retirement (60/40 or 50/50 stocks/bonds vs traditional conservative allocation), (2) TIPS or I Bonds for portion of portfolio, (3) Real estate or REITs providing inflation-linked income, (4) Social Security delay maximizing COLA-protected benefit, (5) Flexible withdrawal strategy adjusting spending during high inflation years. Diversification across inflation-protected income sources provides best protection.

Explore More in Money Basics

Disclosure

This article is provided for educational purposes only and does not constitute financial, investment, or economic advice. Inflation rates vary by country, region, time period, and individual spending patterns. Historical inflation data does not guarantee future rates. Investment returns mentioned are historical averages—actual returns vary significantly and are not guaranteed. Individual circumstances differ based on spending composition, income sources, investment horizons, and risk tolerance. Examples use simplified assumptions and hypothetical scenarios—actual results vary. Inflation-protected investments like TIPS and I Bonds have specific terms, restrictions, and tax implications requiring research. Consult qualified financial professionals, tax advisors, and investment advisors for personalized guidance. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.

Interactive Quiz: Inflation and Purchasing Power

Choose an answer and click Check Answer to learn why it is right or wrong.