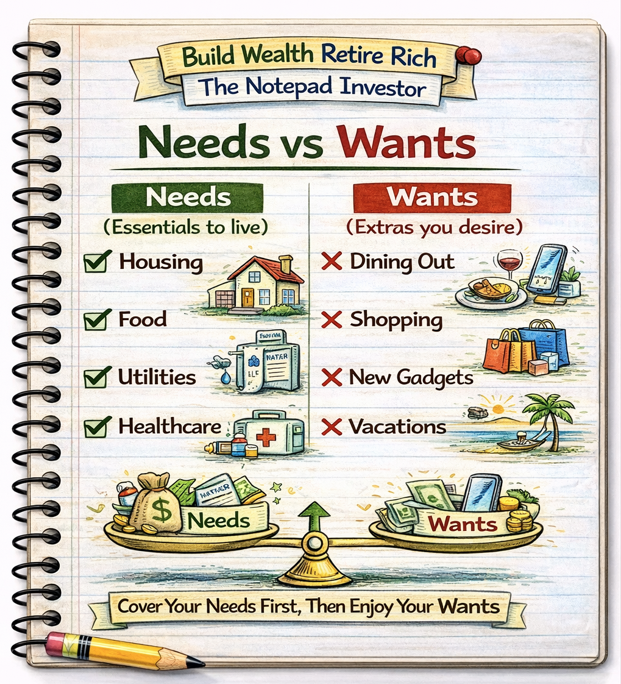

Needs vs wants represents the critical distinction between essential expenses required for basic survival and well-being versus discretionary desires enhancing comfort or lifestyle but remaining non-essential—needs include shelter, food, basic clothing, healthcare, and transportation enabling work, while wants encompass dining out, entertainment, premium versions of necessities, luxury items, and lifestyle upgrades. Unlike treating all expenses equally, distinguishing needs from wants enables strategic spending decisions, emergency budget creation, debt elimination planning, and wealth building through conscious prioritization of essential over discretionary spending.

This article is designed for anyone struggling with spending decisions, individuals living paycheck to paycheck despite adequate incomes, or those seeking to reduce expenses and increase savings. You do not need financial expertise, restrictive diets, or extreme frugality to benefit from needs versus wants clarity—understanding this fundamental distinction transforms spending from unconscious reaction to intentional choice aligned with priorities and financial goals.

Understanding needs vs wants matters because conflating wants with needs leads to overspending on non-essentials preventing wealth building, unclear priorities during financial stress force poor crisis decisions, and inability to distinguish essential from discretionary spending creates perpetual cash flow problems and debt accumulation regardless of income level, leaving people financially vulnerable despite spending on items they believed necessary.

Educational disclaimer: This article provides general educational information about distinguishing needs from wants. Individual circumstances vary—what’s essential for one person may be discretionary for another based on health, location, work requirements, and family situations. This is not financial or budgeting advice. Consult qualified financial professionals for personalized guidance.

Defining Needs

What Are Needs?

Definition: Expenses required for basic survival, health, safety, and ability to earn income

Core characteristics of needs:

- Essential for physical survival or safety

- Required to maintain employment (income generation)

- Necessary for legal or health compliance

- Cannot be eliminated without serious consequences

- Would cause harm if absent

The Hierarchy of Needs (Maslow Applied to Finance)

Level 1: Physiological needs (absolute essentials)

- Food for basic nutrition

- Water and basic utilities

- Shelter from elements

- Basic clothing for protection

- Essential medications and healthcare

Level 2: Safety and security needs

- Safe housing in secure area

- Health insurance for catastrophic protection

- Minimum liability insurance (auto if driving)

- Basic emergency fund preventing homelessness

Level 3: Income-generating needs

- Transportation to work

- Work-appropriate clothing

- Phone/internet if required for employment

- Childcare enabling work

- Tools or equipment for profession

True Needs Categories

Housing (basic shelter):

- Rent or mortgage payment

- Property taxes and essential insurance

- Basic utilities (electric, gas, water, heat)

- Essential home maintenance preventing deterioration

Food (basic nutrition):

- Groceries for home-cooked meals

- Basic nutritious foods meeting caloric needs

- Does NOT include: Restaurants, takeout, delivery, premium brands, convenience foods

Healthcare:

- Health insurance premiums

- Necessary medical treatments and prescriptions

- Preventive care maintaining health

- Dental and vision care for health (not purely cosmetic)

Transportation (to work/essential activities):

- Car payment if vehicle essential for work

- Gas and basic maintenance

- Auto insurance (legally required)

- Public transportation if available alternative

Clothing (basic):

- Weather-appropriate clothing

- Work-required attire

- Basic wardrobe replacements when worn out

- Children’s clothing as they grow

Legal obligations:

- Minimum debt payments avoiding default

- Court-ordered payments (child support, alimony)

- Required insurance coverage

- Necessary taxes

Context-Dependent Needs

Some items are needs for certain people but wants for others based on circumstances:

Car ownership:

- Need: Rural area with no public transit, required for work commute

- Want: Urban area with robust public transportation, walkable neighborhood

Internet/phone service:

- Need: Required for remote work, job searching, essential communications

- Want: Entertainment only, luxury unlimited data plan

Gym membership:

- Need: Medical condition requiring supervised exercise, physical therapy

- Want: Convenience preference, social activity, aesthetic goals

Eating out:

- Need: Business meals required for work, medical condition preventing cooking

- Want: Convenience, social activity, treat, dislike cooking

Defining Wants

What Are Wants?

Definition: Discretionary expenses enhancing lifestyle, comfort, or enjoyment but not required for survival or basic functioning

Core characteristics of wants:

- Enhance quality of life but not essential

- Can be delayed or eliminated without harm

- Represent preferences and choices

- Often emotional or social motivations

- Upgrades beyond basic necessity

Common Wants Categories

Food and dining upgrades:

- Restaurants and takeout

- Food delivery services

- Premium or organic groceries beyond health necessity

- Specialty foods and gourmet items

- Alcohol and beverages beyond water/milk

- Coffee shop drinks vs home brewing

Entertainment:

- Streaming services (Netflix, Hulu, Disney+, etc.)

- Cable TV

- Movies, concerts, sporting events

- Hobbies and recreational activities

- Gaming consoles and video games

- Books, magazines, music (beyond free library options)

Upgraded versions of needs:

- Luxury car vs reliable basic transportation

- Designer clothing vs functional basics

- Large home in premium area vs adequate shelter

- Latest smartphone vs functional older model

- Organic/premium groceries vs standard nutrition

Technology and gadgets:

- Latest smartphone when current one functions

- Smart home devices

- Tablets, smartwatches, earbuds

- Gaming systems

- Upgraded electronics beyond basic needs

Personal care upgrades:

- Salon services vs home hair care

- Professional manicures/pedicures

- Premium beauty and skincare products

- Spa treatments and massages

- Cosmetic procedures

Travel and experiences:

- Vacations and trips

- Weekend getaways

- Leisure travel

- Adventure activities

Lifestyle conveniences:

- House cleaning services

- Meal delivery kits

- Premium subscriptions

- Convenience services

The “Wants Disguised as Needs” Trap

Common rationalizations:

- “I need my daily coffee” (want: habit/ritual, need: caffeine from home brewing)

- “I need a new car” (want: new model, need: reliable transportation—used works)

- “I need cable TV” (want: entertainment, need: none—free options exist)

- “I need to eat out for work” (want: convenience, need: none—meal prep possible)

- “I need this for my mental health” (sometimes valid, often rationalization)

The “deserve it” justification:

- “I work hard, I deserve this vacation”

- “I deserve to treat myself”

- “I deserve nice things”

- Deserving doesn’t make it a need—still a want requiring budgeting

The Gray Area: Needs vs Wants Spectrum

Understanding the Spectrum

Not all expenses fit neatly into “need” or “want” categories—many exist on a spectrum from absolute necessity to pure luxury.

Example: Transportation spectrum

- Pure need: Used reliable car for work commute (no transit alternative)

- Need with want elements: Newer car with safety features

- Middle ground: Reliable car with comfort features

- Want with need elements: Nice car enabling confidence at work

- Pure want: Luxury sports car for enjoyment

Example: Housing spectrum

- Pure need: Safe, basic shelter adequate for family size

- Need with want elements: Extra bedroom for home office

- Middle ground: Desirable neighborhood with good schools

- Want with need elements: Larger home for entertaining

- Pure want: Luxury home with amenities beyond family needs

The 80/20 Need-Want Analysis

Apply to each expense:

- What portion is truly necessary?

- What portion is discretionary upgrade?

Example: $150 grocery bill

- $100 = basic nutritious food (need)

- $30 = convenience and premium items (want)

- $20 = treats and snacks (want)

- 67% need, 33% want

Example: $800 rent

- $600 = basic safe shelter (need)

- $200 = upgraded location/amenities (want)

- 75% need, 25% want

Quality of Life Needs

Some “wants” become needs for long-term sustainability:

- Mental health: Occasional leisure preventing burnout

- Social connection: Some social spending maintaining relationships

- Work effectiveness: Tools or environment enabling productivity

- Family harmony: Activities preventing constant conflict

Balance required: Recognize these as important but budget for them consciously as “quality of life” category rather than justifying all discretionary spending as necessity.

Practical Application: Using Needs vs Wants

Creating a Needs-Only Budget

Purpose: Understand bare minimum living costs for emergency situations or debt payoff

Process:

- List all current expenses

- Mark each as “need” or “want”

- For mixed items, separate need portion from want portion

- Total all true needs

- Result = Survival budget baseline

Example needs-only budget:

- Rent: $1,000 (need)

- Utilities: $150 (need)

- Groceries: $300 (need portion of $400 total)

- Car payment: $250 (need if required for work)

- Car insurance: $100 (need – legally required)

- Gas: $150 (need for work commute)

- Health insurance: $200 (need)

- Phone: $40 (need – basic plan only)

- Minimum debt payments: $200 (need – legal obligation)

- Total needs: $2,390

Wants that could be eliminated temporarily:

- Streaming services: $40

- Dining out: $200

- Premium groceries: $100

- Gym: $50

- Shopping/clothes: $100

- Entertainment: $75

- Total wants: $565

Insight: If income $3,500 and total spending $2,955 ($2,390 needs + $565 wants), survival possible on $2,390 freeing $1,110 monthly for emergency debt payoff or wealth building.

The 50/30/20 Budget Framework

Rule:

- 50% of net income = Needs

- 30% of net income = Wants

- 20% of net income = Savings and debt payoff

Example with $4,000 monthly net income:

- Needs budget: $2,000 (50%)

- Wants budget: $1,200 (30%)

- Savings/debt: $800 (20%)

Flexibility:

- High cost-of-living areas: May need 60/20/20

- Aggressive savers: 50/10/40 or better

- Debt payoff mode: 50/0/50 temporarily

Decision Framework for Purchases

Before any purchase, ask:

- Is this a need or want? Be honest, no rationalization

- If a need, what’s the minimum viable version? Avoid upgrading needs unnecessarily

- If a want, does it fit in my wants budget? Check remaining discretionary funds

- What am I trading for this want? Every dollar spent on wants delays financial goals

- Will I remember/value this in 6 months? Avoid regret purchases

The 24-hour rule for wants:

- Wait 24 hours before purchasing any non-essential item over $50

- If still want it after waiting, evaluate against wants budget

- Prevents impulse purchases disguised as needs

- Reduces regret and wasted money

Common Needs vs Wants Mistakes

Lifestyle Creep (Needs Inflation)

Pattern: Yesterday’s wants become today’s “needs” as income increases

- First apartment: $600 studio = need

- After raise: $1,200 one-bedroom = “need bigger space”

- After promotion: $1,800 two-bedroom = “need home office”

- Income doubled but housing more than tripled

Solution: Revisit needs definition regularly. Challenge upgrades as wants, budget accordingly.

Comparison-Driven “Needs”

Pattern: Defining needs based on peers rather than actual requirements

- “Everyone has Netflix/Hulu/Disney+ so I need them”

- “My coworkers drive nice cars so I need one too”

- “My friends take vacations so I need to travel”

Solution: Define needs based on YOUR life requirements, not others’ choices. Their wants aren’t your needs.

Emergency Justification

Pattern: Claiming wants as needs during specific situations

- “I need this vacation—I’m so stressed” (want: relief, need: stress management has free options)

- “I need new clothes for this event” (want: new outfit, need: wear existing clothing)

- “I need to order food, too tired to cook” (want: convenience, need: nutrition has home options)

Solution: Acknowledge wants honestly. Budget for them if possible, but don’t pretend they’re needs.

Kids’ Wants Become Parents’ “Needs”

Pattern: Children’s desires reframed as necessities

- “They need the latest phone for school” (want: status, need: basic communication)

- “They need brand-name shoes” (want: peer acceptance, need: functional footwear)

- “They need this experience/activity” (want: enrichment, need: free alternatives exist)

Solution: Distinguish actual needs (education, safety, health) from wants (status items, premium experiences). Budget for some wants but be honest about categorization.

Confusion Between Habits and Needs

Pattern: Long-standing habits mistaken for requirements

- “I need my morning Starbucks” (habit, not need—home coffee works)

- “I need to eat out for lunch” (habit, not need—packing lunch possible)

- “I need cable TV” (habit, not need—streaming or antenna alternatives)

Solution: Examine regular expenses. Habits feel like needs but remain wants if alternatives exist.

Why Needs vs Wants Understanding Matters

Without distinguishing needs from wants, people overspend on discretionary items believing them essential preventing savings accumulation, financial emergencies become catastrophic because basic survival costs unclear, and debt accumulation occurs through unconscious want spending rationalized as necessary rather than discretionary choices enabling financial fragility regardless of income level.

Understanding needs vs wants enables individuals to:

- Create realistic budgets distinguishing essential from discretionary

- Survive financial emergencies by cutting to needs-only spending

- Accelerate debt payoff through temporary want elimination

- Make conscious spending choices aligned with priorities

- Reduce financial stress through clarity about true requirements

- Build wealth faster by controlling want spending strategically

Needs versus wants clarity transforms spending from emotional reaction to intentional choice supporting financial goals and security.

Common Misunderstandings

Many people assume needs versus wants distinction requires extreme deprivation or elimination of all enjoyment. In reality, understanding the difference enables strategic allocation of discretionary spending to highest-value wants rather than unconscious spending on low-value items—knowing what’s truly needed creates freedom to spend on wants deliberately and guilt-free within budget constraints.

Another common misconception is that wants are bad or wasteful. In practice, wants enhance life quality and happiness when budgeted appropriately—problem arises when wants consume resources needed for financial security or when wants are rationalized as needs preventing honest budget management and conscious choice-making.

Some believe their personal needs are objectively higher than average requiring more spending. However, most people’s true survival needs are similar—differences lie in quality preferences, location choices, and lifestyle standards representing wants added to basic needs, not genuinely higher baseline requirements for survival and functioning.

How Needs vs Wants Fits Into Financial Health

Needs versus wants distinction provides framework for all financial decisions—emergency budgets cut to needs only, debt payoff prioritizes needs funding wants elimination, and wealth building requires conscious want control directing surplus toward savings and investment rather than lifestyle inflation consuming income increases.

For example, person earning $4,000 monthly treats all spending as needs—$3,900 total expenses seem necessary, leaving only $100 monthly for savings. Financial emergency occurs requiring budget cuts but person believes they “can’t cut anything because everything is a need.” Result: Credit card debt accumulation at 20% interest. Contrast: Similar person honestly categorizes $2,200 as true needs, $1,700 as wants. Emergency occurs—immediately cuts wants to zero, maintains $2,200 needs, uses $1,800 monthly surplus to handle emergency without debt. After emergency passes, gradually adds back highest-value wants while maintaining $800+ monthly savings. Needs versus wants clarity enabled emergency navigation without debt spiral plus sustainable wealth building.

Needs versus wants distinction creates financial flexibility and resilience impossible when all spending treated as equally necessary.

Recent Updates and Trends

In recent years, subscription creep has blurred needs-wants lines—multiple streaming services, apps, memberships accumulating creating perception of necessity when all are wants requiring conscious evaluation and elimination.

Minimalism movement has popularized needs-wants distinction—deliberate living emphasizing need satisfaction while questioning want accumulation, though some interpretations become extreme rather than balanced.

Influencer culture has intensified wants-as-needs confusion—social media showcasing lifestyles creating artificial needs through comparison and FOMO (fear of missing out) driving discretionary spending rationalized as necessary.

Economic uncertainty has renewed interest in needs-only budgeting—more people creating survival budgets understanding bare minimum costs as financial fragility protection.

Fundamental needs versus wants principles remain timeless: distinguish essential survival requirements from discretionary enhancements, budget for both honestly rather than rationalizing wants as needs, maintain ability to cut to needs-only during emergencies, and consciously allocate discretionary spending to highest-value wants rather than unconscious accumulation of low-satisfaction purchases.

3 Things You Can Do Today

Ready to clarify needs vs wants? Here are three simple steps you can take right now:

1. Categorize last month’s expenses as needs vs wants – Pull last month’s bank and credit card statements. List every expense. Mark each honestly as “need” or “want” (no rationalization allowed). For mixed items, separate need portion from want portion. Total each category. Calculate percentages. This reveals actual spending patterns versus assumptions. Most people discover 40-60% of spending is wants they believed were needs.

2. Create your needs-only survival budget – List minimum expenses for basic survival if emergency required drastic cuts: shelter, basic utilities, minimum groceries, essential transportation, legally required insurance and payments, critical healthcare. Total these. This number = emergency baseline. Knowing this amount reduces financial anxiety—you know exact minimum required for survival. Typical needs-only budget: 50-60% of current spending.

3. Implement the 24-hour want delay rule – Starting today: Before purchasing any non-essential item over $50, wait 24 hours. Write down the item and date. If still want it tomorrow, evaluate against monthly wants budget. If fits budget and still desired, purchase. This single rule prevents impulse want purchases saving $100-$500+ monthly for most people—those savings compound to $50,000-$250,000+ over 20 years invested.

These actions create needs versus wants clarity enabling conscious spending choices rather than unconscious rationalization and impulse purchases.

Quick FAQ

How do I know if something is really a need?

Ask: “What happens if I don’t have this?” If answer includes: physical harm, homelessness, inability to work, legal consequences, health deterioration—it’s likely a need. If answer is: disappointment, inconvenience, missing out, looking less successful—it’s a want. Most honest self-assessment reveals 70%+ of “needs” are actually wants we strongly prefer.

Are any wants actually okay to have?

Absolutely! Wants are not evil or wasteful—they enhance life quality and happiness. Problem arises when: (1) wants consume resources needed for financial security, (2) wants are rationalized as needs preventing honest budgeting, (3) want spending is unconscious rather than intentional. Budget consciously for wants within your discretionary income after covering needs and savings goals.

What percentage of my budget should be needs vs wants?

General guideline: 50% needs, 30% wants, 20% savings (50/30/20 rule). High cost-of-living areas might be 60/20/20. Aggressive savers: 50/10/40. During debt payoff: 50/0/50 temporarily. Adapt to your situation but maintain clear separation and honest categorization. Most people claim 80-90% needs when actually 50-60%.

Is a car a need or want?

Depends entirely on circumstances. Need: Rural area, no public transit, required for work commute with no alternatives. Want: Urban area with robust public transportation, walkable neighborhood, or remote work. Even when car is need, luxury model vs. reliable used vehicle represents want portion. Context matters—examine your specific situation honestly.

How can I afford wants on a tight budget?

After covering needs and minimum savings (even $50-100 monthly), allocate specific wants budget from remaining income. Choose highest-value wants that bring most joy per dollar. Example: $100 monthly wants budget might go to one streaming service ($15), one nice dinner ($40), hobby supplies ($30), social activity ($15). Strategic want spending beats unconscious want accumulation exceeding budget.

What if my needs exceed my income?

Two options: (1) Reduce needs through major changes (cheaper housing, eliminate car via public transit, roommates, move to lower-cost area), (2) Increase income urgently (second job, higher-paying work, government assistance if eligible). Unsustainable long-term—requires immediate action. Examine “needs” critically—often contain want elements that can be reduced (cheaper housing location, basic food vs premium groceries, etc.).

Explore More in Money Basics

Disclosure

This article is provided for educational purposes only and does not constitute financial or budgeting advice. What constitutes a “need” versus “want” varies by individual circumstances including health conditions, location, work requirements, family situations, and personal values. Information presented represents general frameworks—specific categorizations depend on individual contexts. Examples are illustrative—actual spending patterns and appropriate needs-wants balances vary significantly. No judgment intended for any spending choices—article aims to provide clarity for informed decision-making, not prescribe specific lifestyles. Consult qualified financial professionals for personalized guidance. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.

Interactive Quiz: Needs vs Wants

Choose an answer for each question and click Check Answer to learn why it is right or wrong.