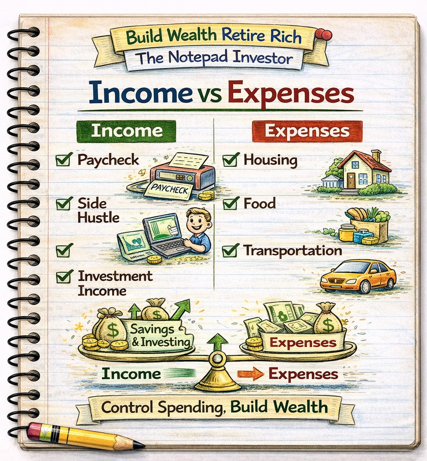

Income vs expenses represents the fundamental financial equation determining whether you’re building wealth, treading water financially, or sliding into debt—income encompasses all money flowing into your household while expenses represent all money flowing out, with the critical difference between these numbers determining financial trajectory. Unlike focusing on income alone, understanding the relationship between earnings and spending reveals true financial health, with positive cash flow (income exceeding expenses) enabling savings and wealth building while negative cash flow (expenses exceeding income) forces debt accumulation regardless of income level.

This article is designed for anyone wanting to understand their true financial position, individuals struggling financially despite decent incomes, or those seeking to improve cash flow and build wealth. You do not need accounting expertise, financial degrees, or complex spreadsheets to analyze income versus expenses—simple tracking and awareness of this fundamental relationship transforms financial outcomes more than any other single factor.

Understanding income vs expenses matters because high earners living paycheck to paycheck prove income alone doesn’t create financial security, modest earners with disciplined spending build substantial wealth demonstrating expense control matters more than income level, and unconscious spending patterns destroy financial potential forcing people to work longer than necessary or remain trapped in jobs they dislike despite adequate or even high incomes.

Educational disclaimer: This article provides general educational information about income and expense management. Individual financial situations vary significantly. This is not financial, tax, or investment advice. Consult qualified financial professionals for personalized guidance based on specific circumstances.

Understanding Income

Types of Income

Earned income (active income):

- Wages and salary from employment

- Hourly pay or commissioned earnings

- Tips and bonuses

- Self-employment income

- Freelance or gig work earnings

- Requires active work to generate

Passive income:

- Rental property income

- Dividend and interest from investments

- Royalties from creative work

- Business income with minimal involvement

- Continues with limited ongoing effort

Government benefits:

- Social Security retirement or disability

- Unemployment compensation

- Veterans benefits

- Supplemental Security Income (SSI)

- Child tax credits or stimulus payments

Other income sources:

- Alimony or child support

- Pension payments

- Annuity distributions

- Trust distributions

- Gifts or inheritance (irregular)

Gross Income vs Net Income

Gross income:

- Total earnings before any deductions

- Listed on pay stubs and tax returns

- Used for loan qualifications and rent applications

- Example: $75,000 annual salary = $75,000 gross income

Net income (take-home pay):

- Money actually received after deductions

- What deposits into bank account

- What’s available for spending and saving

- Critical number for budgeting

Common deductions from gross to net:

- Federal income tax (10-37% depending on bracket)

- State income tax (0-13% depending on state)

- FICA taxes (7.65%: Social Security 6.2% + Medicare 1.45%)

- Health insurance premiums

- Retirement contributions (401k, 403b)

- HSA or FSA contributions

- Other voluntary deductions

Example calculation:

- Gross salary: $75,000 annually ($6,250 monthly)

- Federal tax (est.): -$900 monthly

- State tax (est.): -$300 monthly

- FICA: -$478 monthly

- Health insurance: -$200 monthly

- 401k (10%): -$625 monthly

- Net income: $3,747 monthly (60% of gross)

Critical point: Budget based on net income, not gross. Many people overspend by mentally spending gross income unavailable to them.

Variable vs Stable Income

Stable income characteristics:

- Predictable amounts each pay period

- Salaried positions or hourly with consistent hours

- Easy to budget with certainty

- Lower financial stress

Variable income characteristics:

- Fluctuates month to month

- Commission-based sales, freelance work, seasonal businesses

- Requires different budgeting approach

- Needs larger emergency fund for lean months

Budgeting with variable income:

- Calculate average monthly income (last 12 months)

- Budget based on lowest earning months

- Save excess from high-earning months for low months

- Maintain larger emergency fund (6-12 months vs 3-6)

- Prioritize essential expenses first

Understanding Expenses

Fixed Expenses

Definition: Costs that remain constant month to month, due on specific dates

Examples:

- Rent or mortgage payment

- Car payment or lease

- Insurance premiums (auto, health, life, renters/homeowners)

- Loan payments (student loans, personal loans)

- Subscriptions (streaming services, gym memberships, software)

- Phone and internet bills

- Childcare costs

Characteristics:

- Predictable and consistent

- Easy to budget for

- Often contractual obligations

- Difficult to change short-term

- Should total 50-60% of net income ideally

Variable Expenses

Definition: Costs that fluctuate month to month based on usage or consumption

Examples:

- Groceries and household supplies

- Utilities (electric, gas, water)

- Gasoline and transportation

- Medical expenses and prescriptions

- Clothing and personal care

- Home and auto maintenance

Characteristics:

- Change monthly based on behavior and needs

- Some control possible through conscious choices

- Require monthly budget adjustments

- Can estimate based on historical averages

Discretionary Expenses

Definition: Non-essential spending on wants rather than needs

Examples:

- Dining out and takeout

- Entertainment (movies, concerts, events)

- Hobbies and recreation

- Travel and vacations

- Shopping for non-essentials

- Premium subscriptions beyond basic needs

Characteristics:

- Completely controllable

- First area to cut when budgets tight

- Should be 20-30% of net income maximum

- Often unconscious spending category

- Significant wealth-building opportunity through reduction

Periodic/Irregular Expenses

Definition: Expenses occurring less frequently than monthly but predictably

Examples:

- Annual insurance premiums

- Property taxes (quarterly or annually)

- Vehicle registration and smog checks

- Quarterly HOA fees

- Annual membership renewals

- Holiday and birthday gifts

- Back-to-school expenses

Budgeting strategy:

- Calculate annual total for all periodic expenses

- Divide by 12 to get monthly amount

- Save monthly amount in separate account

- Pay periodic bills from accumulated savings

- Prevents financial surprises and debt accumulation

Example:

- Car insurance: $1,200 annually

- Property tax: $3,600 annually

- Gifts: $1,200 annually

- Total: $6,000 annually = $500 monthly to save

Essential vs Non-Essential Expenses

Essential (needs):

- Housing (rent/mortgage, utilities)

- Food (groceries for home cooking)

- Transportation (car payment, gas, insurance OR public transit)

- Basic clothing

- Healthcare (insurance, medications, necessary care)

- Minimum debt payments

- Basic phone/internet for work and safety

Non-essential (wants):

- Dining out and delivery

- Cable TV or premium streaming

- New clothing beyond basic needs

- Entertainment and recreation

- Upgraded phone or car beyond needs

- Vacations and travel

- Hobbies and luxury items

Gray area items (depends on circumstances):

- Car (essential in some areas, luxury in cities with transit)

- Internet/phone (essential for work, but premium plans may not be)

- Gym membership (health necessity for some, luxury for others)

- Eating out (occasional socializing vs daily convenience)

The Critical Income vs Expenses Relationship

Three Possible Scenarios

Scenario 1: Negative Cash Flow (Expenses > Income)

- Spending more than earning monthly

- Accumulating credit card debt or depleting savings

- Unsustainable long-term

- Leads to financial crisis without correction

- Common even among high earners with lifestyle inflation

Example: Net income $4,000, expenses $4,500 = -$500 monthly deficit = $6,000 annual debt accumulation

Scenario 2: Break Even (Expenses = Income)

- Spending entire paycheck monthly

- Living paycheck to paycheck

- No savings accumulation or wealth building

- Vulnerable to any financial emergency

- Majority of Americans in this situation

Example: Net income $4,000, expenses $4,000 = $0 savings = financial fragility

Scenario 3: Positive Cash Flow (Income > Expenses)

- Earning more than spending

- Surplus available for saving and investing

- Building emergency fund and wealth

- Financial security increasing over time

- Achievable at any income level through disciplined spending

Example: Net income $4,000, expenses $3,200 = $800 monthly surplus = $9,600 annual savings/investment

The Savings Rate Concept

Formula: Savings Rate = (Net Income – Expenses) ÷ Net Income × 100

Savings rate targets:

- Minimum viable: 10-15% (basic retirement funding)

- Good: 20-30% (comfortable retirement, financial flexibility)

- Excellent: 30-50% (early retirement possible, rapid wealth building)

- Extreme: 50-70%+ (early retirement in 10-15 years feasible)

Examples:

- Income $4,000, expenses $3,600, savings $400 = 10% rate

- Income $4,000, expenses $3,200, savings $800 = 20% rate

- Income $4,000, expenses $2,400, savings $1,600 = 40% rate

Critical insight: Savings rate matters more than income level for wealth building. Someone earning $50,000 saving 30% builds wealth faster than someone earning $100,000 saving 5%.

Income Level vs Financial Health

High income doesn’t guarantee financial health:

- Earning $150,000 but spending $160,000 = financial distress

- Lifestyle inflation consuming raises

- Expensive housing, cars, lifestyle commitments

- High earners can be broke

Modest income can build substantial wealth:

- Earning $50,000 but spending $35,000 = $15,000 annual savings

- 30% savings rate building wealth rapidly

- Modest lifestyle enabling financial freedom

- Discipline matters more than income

Real-world example comparison:

Person A:

- Income: $150,000 gross ($100,000 net)

- Expenses: $95,000 annually

- Savings: $5,000 annually (5% rate)

- After 20 years: ~$200,000 saved

Person B:

- Income: $60,000 gross ($45,000 net)

- Expenses: $33,000 annually

- Savings: $12,000 annually (27% rate)

- After 20 years: ~$480,000 saved

Conclusion: Person B earning less than half Person A’s income accumulates more than double the wealth through disciplined expense control and higher savings rate.

Improving Your Income vs Expenses Ratio

Strategy 1: Increase Income

Career advancement:

- Pursue promotions and raises (average 3% annual, negotiate for 10-20%)

- Develop high-value skills increasing marketability

- Professional certifications or additional education

- Change employers strategically (often 10-20% income increase)

Side income:

- Freelance work in existing skills ($500-$2,000+ monthly possible)

- Part-time job or gig work (delivery, tutoring, etc.)

- Sell items or start small business

- Rent spare room or parking space

Passive income development:

- Investment dividends and interest

- Rental property income

- Create and sell digital products

- Build assets generating ongoing revenue

Reality check: Income increases often trigger lifestyle inflation, negating benefits unless spending discipline maintained.

Strategy 2: Decrease Expenses (Often Faster and More Controllable)

Fixed expense reduction:

- Refinance mortgage or negotiate rent (save $100-$500+ monthly)

- Shop insurance annually (save $50-$200+ monthly)

- Eliminate or downgrade subscriptions (save $50-$200+ monthly)

- Refinance high-interest debt to lower rates

- Downsize housing or vehicles if significantly oversized

Variable expense reduction:

- Meal planning and cooking vs eating out (save $200-$600+ monthly)

- Reduce utility usage through conservation (save $20-$100+ monthly)

- Generic vs name brand products (save $50-$150+ monthly)

- DIY vs hiring for some services

Discretionary expense reduction:

- Entertainment at home vs expensive outings (save $100-$400+ monthly)

- Free or low-cost hobbies and activities

- Strategic shopping vs impulse purchases

- Delay or eliminate non-essential purchases

Expense reduction example (moderate cuts):

- Meal planning vs takeout: -$300 monthly

- Insurance shopping: -$100 monthly

- Subscription audit: -$75 monthly

- Entertainment choices: -$150 monthly

- Total reduction: -$625 monthly = $7,500 annual savings increase

Strategy 3: Optimize Both Simultaneously

Most effective approach:

- Increase income through career development and side hustles

- Simultaneously reduce or maintain expenses despite income increases

- Direct all income increases to savings and investment

- Avoid lifestyle inflation consuming raises

- Maximize savings rate through dual approach

Example:

- Year 1: Income $50,000, expenses $42,000, savings $8,000 (16% rate)

- Year 3: Income $65,000 (promotion + side hustle), expenses $42,000 (maintained), savings $23,000 (35% rate)

- Income increased 30%, expenses stayed flat, savings increased 188%

Tracking Income vs Expenses

Why Tracking Matters

- Reveals actual spending vs perceived spending (often shockingly different)

- Identifies unconscious money leaks

- Enables informed budget adjustments

- Provides accountability for financial goals

- Increases financial awareness changing behaviors

Tracking Methods

Manual tracking (spreadsheet or notebook):

- Complete control and customization

- Free

- Requires discipline to maintain

- Good for understanding financial details

Budgeting apps (Mint, YNAB, EveryDollar):

- Automatic transaction categorization

- Real-time spending tracking

- Budget alerts and reports

- Free or $10-$15 monthly

- Easiest long-term maintenance

Bank/credit card tracking features:

- Built into many banking apps

- Automatic categorization

- Spending insights and trends

- Free but limited features

What to Track

- All income sources and amounts with dates

- Every expense categorized by type

- Payment methods (cash, debit, credit)

- Monthly totals by category

- Net cash flow (income – expenses)

- Savings and investment contributions

Tracking Frequency

- Record transactions: Daily or weekly (before forgetting)

- Review spending: Weekly (adjust behavior in real-time)

- Analyze patterns: Monthly (identify trends and adjust budget)

- Comprehensive review: Quarterly or annually (big-picture assessment)

Why Income vs Expenses Understanding Matters

Without understanding income versus expenses relationship, people focus solely on earning more while spending proportionally, earning $100,000 yet living paycheck to paycheck proving income alone doesn’t create wealth, and remain perpetually financially stressed despite adequate incomes because unconscious spending patterns consume all earnings preventing savings accumulation and wealth building.

Understanding income vs expenses enables individuals to:

- Identify true financial position beyond income level

- Build wealth through spending discipline regardless of earnings

- Eliminate paycheck-to-paycheck living through positive cash flow

- Make informed decisions about lifestyle affordability

- Achieve financial goals through systematic surplus management

- Reduce financial stress through expense awareness and control

Income versus expenses awareness transforms financial outcomes through behavior change more than income increases alone.

Common Misunderstandings

Many people assume wealth comes primarily from high income. In reality, wealth accumulation depends more on savings rate (income minus expenses gap) than absolute income level—disciplined moderate earners often accumulate more wealth than high earners with proportionally high spending through superior expense management.

Another common misconception is that cutting expenses means deprivation and miserable living. In practice, strategic expense reduction focuses on eliminating unconscious waste and low-value spending while maintaining or improving life satisfaction—most people find happiness unchanged or improved when cutting expenses they barely noticed or valued.

Some believe tracking every expense is obsessive or unnecessary micromanagement. However, initial tracking phase (3-6 months) reveals spending patterns enabling informed decisions, after which many people maintain financial health with periodic reviews rather than detailed daily tracking—temporary detailed awareness creates lasting beneficial behavior changes.

How Income vs Expenses Fits Into Financial Success

Income versus expenses relationship determines financial trajectory—positive cash flow enables emergency funds, debt elimination, investment, and wealth accumulation while negative cash flow forces debt accumulation, financial stress, and perpetual paycheck-to-paycheck living regardless of income level achieved.

For example, two households both earn $75,000 annually. Household A focuses exclusively on income—works overtime, pursues raises, adds side hustles increasing income to $90,000 over three years but simultaneously lifestyle inflates, now spending $88,000 annually with minimal savings despite higher income. Household B earns steady $75,000 but focuses on expense optimization—reduces spending from $70,000 to $55,000 through strategic cuts, maintains modest lifestyle, saves $20,000 annually. After 10 years: Household A has minimal savings despite higher income, still financially stressed. Household B has $250,000+ saved and invested, financial security, and work optionality. Same starting income, different expense discipline, dramatically different financial outcomes.

Income vs expenses relationship determines financial destiny more than income level alone.

Recent Updates and Trends

In recent years, FIRE movement (Financial Independence Retire Early) has popularized extreme savings rates—followers save 50-70% of income through aggressive expense optimization enabling retirement in 10-15 years rather than traditional 40-year careers.

Budgeting apps have democratized expense tracking—automatic transaction categorization, real-time alerts, and spending insights make tracking effortless versus traditional manual methods, increasing adoption and awareness.

Lifestyle inflation awareness has increased—more people consciously combat tendency to increase spending with income, directing raises to savings rather than upgraded lifestyles.

Side hustle culture has normalized multiple income streams—gig economy enables easier income supplementation, though expense discipline remains critical to prevent additional income funding additional spending.

Fundamental income vs expenses principles remain timeless: positive cash flow (spending less than earning) is foundation of wealth building, savings rate matters more than income level, expense awareness and control create financial security, and disciplined spending enables financial freedom regardless of income achieved.

3 Things You Can Do Today

Ready to optimize income vs expenses? Here are three simple steps you can take right now:

1. Calculate your exact monthly cash flow – List all income sources this month (net amounts deposited). List all expenses this month across all accounts and payment methods. Subtract expenses from income. Result shows if you have positive (surplus), zero (break even), or negative (deficit) cash flow. Then calculate savings rate: (Income – Expenses) ÷ Income × 100. This reveals true financial position in 30 minutes.

2. Track all spending for next 30 days – Download budgeting app (Mint, YNAB, EveryDollar) or create simple spreadsheet. Record every expense for one month—coffee, groceries, bills, everything. Categorize by type (housing, food, transportation, discretionary, etc.). This reveals actual spending patterns versus assumptions. Most people discover $200-$500+ monthly unconscious spending in first tracking month.

3. Identify three expense reduction opportunities – Review last month’s spending. Find three cuts requiring minimal lifestyle impact: unused subscriptions ($10-$50+ monthly), excessive dining out (reduce 25% = $100-$200+ monthly), insurance shopping ($50-$100+ monthly), generic products ($20-$50+ monthly). Make changes today. Small cuts compound—$200 monthly reduction = $2,400 annually = $24,000+ over 10 years invested.

These actions transform vague financial awareness into concrete data enabling informed decisions improving income versus expenses relationship.

Quick FAQ

What’s a good income to expenses ratio?

Aim for 80/20 rule: Expenses maximum 80% of net income, savings minimum 20%. Better: 70/30 (expenses 70%, savings 30%). Excellent: 60/40 or better. Minimum viable: 85/15 (expenses 85%, savings 15% for basic retirement funding). Key: Consistent positive cash flow with meaningful savings rate regardless of specific ratio.

Is it better to increase income or decrease expenses?

Both matter, but expense reduction often faster and more controllable. Can cut expenses $500 monthly in weeks; increasing income $500 monthly may take months or years. Best approach: Optimize both simultaneously—reduce expenses while pursuing income increases, direct all raises to savings avoiding lifestyle inflation. This maximizes savings rate improvement.

How do I stop living paycheck to paycheck?

Four steps: (1) Track all spending for one month identifying waste, (2) Cut expenses 10-20% through strategic reductions, (3) Save surplus in separate account, (4) Build $1,000 starter emergency fund preventing debt during minor emergencies. Then continue building 3-6 month emergency fund. Positive cash flow plus emergency cushion breaks paycheck-to-paycheck cycle.

What if my expenses exceed my income?

Immediate action required—unsustainable long-term. Options: (1) Reduce expenses drastically (needs-only budget temporarily), (2) Increase income urgently (second job, side hustle, sell possessions), (3) Combination approach. Prioritize: Stop accumulating new debt, make minimum debt payments, reduce all discretionary spending to zero temporarily. Get to break-even minimum, then build surplus.

Should I budget on gross or net income?

Always budget based on net (take-home) income—what actually deposits in your account after taxes and deductions. Budgeting on gross income leads to overspending since 20-40% of gross never reaches you. Exception: When calculating savings rate including 401k contributions, use gross income since retirement savings count toward rate even though pre-tax.

How much should I spend on different expense categories?

General guideline (50/30/20 rule): 50% needs (housing, food, transportation, insurance, minimum debt payments), 30% wants (entertainment, dining out, hobbies, non-essentials), 20% savings and extra debt payments. Adjust based on circumstances: High cost-of-living areas may need 60% needs, 20% wants, 20% savings. Aggressive savers: 50% needs, 10% wants, 40% savings.

Explore More in Money Basics

Disclosure

This article is provided for educational purposes only and does not constitute financial, tax, or investment advice. Individual financial situations vary significantly based on income levels, living costs, family circumstances, and personal priorities. Expense reduction strategies and savings rate targets are generalizations—specific appropriate levels depend on individual circumstances. Examples are illustrative—actual results vary based on income, expenses, investment returns, and time horizons. Information current as of publication but personal finance best practices and available tools evolve. Consult qualified financial professionals for personalized guidance. Advertisements or sponsored content may appear within or alongside this content. All information is presented independently.

Interactive Quiz: Income vs Expenses

Choose an answer for each question and click Check Answer to learn why it is right or wrong.